Retire Right

Arno Olckers, Business Development Manager at Morningstar Investment Management SA

The impact of income drawdowns and volatility

Globally markets are in the red and inflation is on the rise which translates to rising interest rates. Higher prices and spikes in market volatility have added to the already increasing list of investor worries – especially those that are dependent on their investments for an income. Living annuity investors are left wondering – will my income last? Should I be drawing more income? What about the effect of market volatility on my capital? Should I cash in my investment and rather wait it out?

In our previous Retire Right article, we focused on costs and how this affects your portfolio. In this article, we focus on two other important aspects – namely the amount you withdraw from your living annuity, as well as the importance of having the right investment strategy.

How much income can an investor withdraw safely to ensure they don’t run out of money?

The number of years you can withdraw a sustainable income from your living annuity depends on a few factors namely:

- The investment amount you have accumulated over time (the amount you have saved up to retirement, will be the initial investment in your living annuity).

- Your total amount of expenses per month[1].

- Your investment holdings and level of investment risk (in other words, what funds/asset classes are included in your portfolio and whether these allocations will give you a sufficient real return on your investment over time).

- The fees you pay in your portfolio.

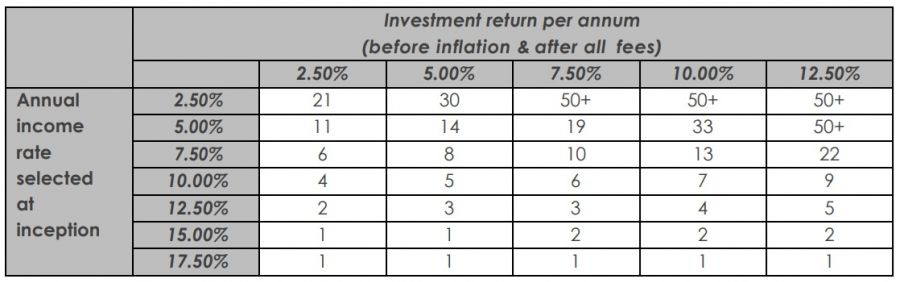

As can be seen in the table below produced by the Association for Savings and Investment South Africa (ASISA) - an investor will be able to maintain their level of income for 33 years, if they maintain a 5% drawdown rate, increasing by 6% inflation (every year) with a portfolio generating a 10% annualised return; thereafter their income will start to decrease rapidly.

Source: Association for Savings and Investment South Africa (ASISA)’ “Living Annuity Standard” report. Last updated 17 September 2021. For illustrative purposes only. Note: The table above assumes that you will adjust your percentage income selected over time to maintain the same amount of real income (i.e. allowing for inflation of 6% per annum). Once the number of years in the table above has been reached, your income will diminish rapidly in the subsequent years.

What is also apparent in this table is that if an investor requires a bigger drawdown of 7.5%, with the same assumptions his/her income will already start decreasing after 13 years. For such a small increase in drawdown, the impact is significant on the investor’s portfolio.

Are there tried and tested withdrawal rates that should be considered?

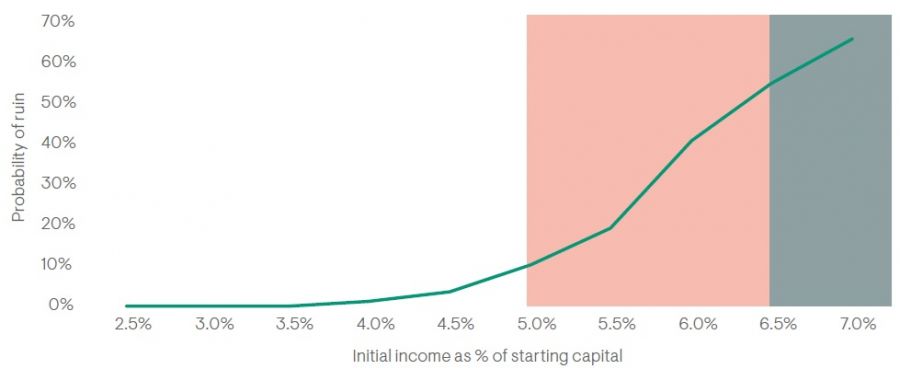

Ninety One conducted a study on income strategy failure rates given different drawdown rates. In this study they used a baseline strategy, meaning a client at retirement chooses a starting income and increases their income with the exact inflation percentage every year (also called inflation-adjusted method).

From the below graph, the study found:

- Clients withdrawing 4% resulted in no failures over a 118-year simulated model.

- When clients increased their income to 5% the failure rate approached 10%.

- When clients increased their income drawdown to 7%, the failure rate jumped more than 60%.

Taking into consideration that the average drawdown rate in South Africa is over 8%, more than 70% of investors will fail in retirement and completely deplete their living annuity.

Income strategy failure rates

Source: Ninety One SA (Pty) Ltd., “A sensible income strategy is critical for living annuity investors”. Data as at 28 June 2018. For illustrative purposes only.

What should I be investing in to ensure that my portfolio delivers a sufficient real return?

As the saying goes “it takes two to tango” and in a living annuity these two factors are the amount of risk an investor takes on (to ensure investment growth) whilst also maintaining low volatility.

A living annuity portfolio needs to generate a real return for investors, which is a return after inflation. This is only possible with a healthy exposure to growth assets (50% minimum).

At the same time, an investor should also experience lower volatility in retirement because there is an income drawdown involved. For this reason, a foreign exposure between 30% - 50% is optimal.

A very important point to remember, is that global exposure reduces volatility only to a certain point. Never underestimate the impact of the rand strengthening, as we experienced in June 2021, September 2021 and more recently March 2022.

In closing

The best thing an investor can do when contemplating change is to reflect on their goals.

Ask yourself this: "Given where I am now, what actions move me closer to my long-term goals?" "Would an investment change align with the original investment plan for reaching well-defined goals?" These are different questions than, "What do I wish I had done last month"? No doubt losses are painful. But reactivity to losses can induce a person to act rashly and make things worse in the long run.

So, the key question to ask is whether anything has fundamentally changed since setting the original strategy or whether it’s just that you are disappointed with your progress toward your goals.

We believe that “staying the course” is the right approach, patiently allocating to assets that will help you achieve your goal. So, if you catch yourself getting down about the state of the market or trying to predict what is next, keep in mind these concepts and always remember why you are investing in the first place.