Retire Right

Arno Olckers, Business Development Manager at Morningstar Investment Management SA

Roné Swanepoel, Business Development Manager at Morningstar Investment Management SA

The impact of fees on living annuities

The year has been off to a busy start, keeping investors at the edge of their seats. One can’t help but feel like everything is ‘increasing’ or being hiked – whether it be interest rates, the price of diesel and petrol, rates, taxes and/or geopolitical tensions, the trend seems to be upward.

During times like these – when everything thing else is increasing in cost - clients drawing an income are often impacted the hardest, as these rising costs eat away at their hard-earned savings.

Managing funds and investments require time, money and expertise. As with any service provider, you are expected to pay a reasonable charge for the use of a company’s services. The same rule applies in the world of investments and fund management. It is therefore important that an investor knows how much they are paying and decide if it is good value for the service and investment performance they are getting and/or expecting in return.

At Morningstar Investment Management South Africa, minimising costs is something that we focus on extensively. Price is one of the five pillars that we consider when evaluating a fund during the research process. If a fund manager charges higher fees, they will need to demonstrate that their process can produce meaningful outperformance relative to their peers.

Impact of fees on living annuities

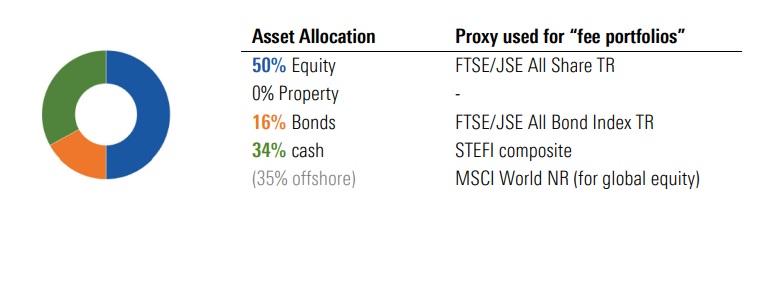

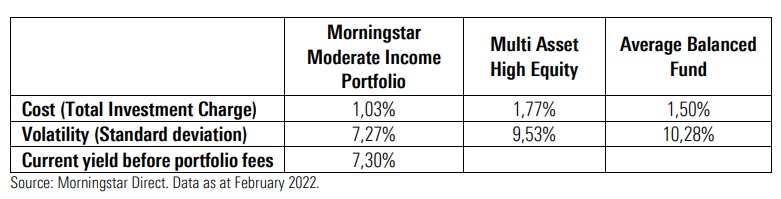

To put the cost of investment fees and the impact it has on a client’s portfolio over time into perspective, we compared the Morningstar Moderate Income Portfolio’s fee to that of the ASISA MA High Equity category average as well as the average fee of the top 10 balanced funds.

To achieve an equal comparison, we simulated three portfolios using the below target asset allocation of the Morningstar Moderate Income portfolio:

The following fees were used:

- We used a fee of 1,03% for Portfolio 1 (this is the fee of the Morningstar Moderate Income Portfolio)

- We used a fee of 1.50% for Portfolio 2 (this is the average fee of the top 10 local Balanced

funds)

- We used a fee of 1.77% for Portfolio 3 (this is the average fee of the ASISA MA High

Equity category)

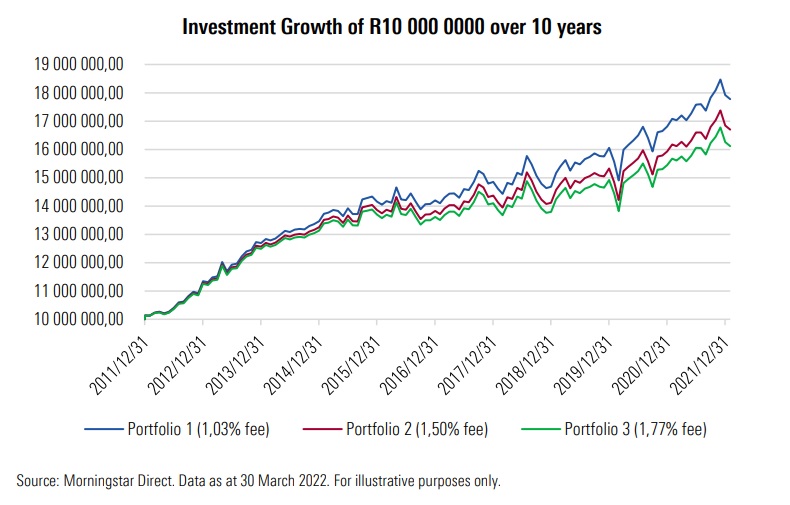

The following assumptions were used in the three simulated investment portfolios:

- The investor retired with R10,000,000 at age 60

- The investment term is 10 years

- 5% annual income drawn monthly; increased by 6% inflation annually

- Income is withdrawn proportionately from all the underlying holdings

- Monthly rebalancing of the portfolios

The results:

Some noteworthy results:

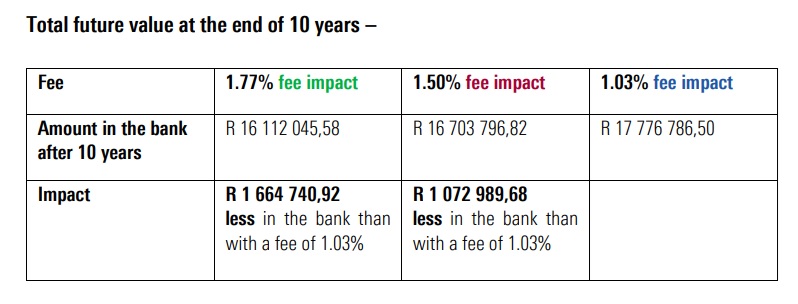

If we look at the results it becomes clear that the investor in the Morningstar Moderate Income portfolio (with a total TIC of 1,03%) has a higher chance of success during retirement given the lower fees they are paying when compared to the average balanced fund or sector. The impact of the difference in fees is immaterial over the short term but as the investment term increases the impact becomes more pronounced.

• When comparing the Morningstar Moderate Income portfolio’s fee impact to that of the fee of the ASISA MA High Equity category average, it enables the investor to earn R1 664 740,92 more over 10 years.

• When comparing Morningstar Moderate Income portfolio’s fee impact to that of the fee of the top 10 average balanced funds, it enables the investor to earn R1 072 989,68 more over 10 years.

As mentioned above, at Morningstar we are committed to minimizing costs. One of the ways in which we achieve this is by negotiating preferred fee classes from the asset managers we work with as well as by using selective passive funds, where appropriate.

Morningstar’s Moderate Income Portfolio

At Morningstar, we believe it is important to build a robust portfolio with a diverse range of return drivers. The Morningstar Moderate Income, created specifically with living annuity clients in mind, produces a high yield while keeping volatility and costs low. Each of the underlying funds in the portfolio has been handpicked to fulfil a very specific purpose - whether it is to produce yield, reduce volatility or bring down the overall cost of the portfolio.

The portfolio offers protection against rising inflation with exposure to value sectors, commodities, and high-quality companies with pricing power. To protect against interest rate hikes, we have exposure to financials. Our portfolios have sufficient exposure to SA Government Bonds to benefit from the high yields on offer. In the offshore allocation of the portfolio, we are underweight the US market and allocated to cheaper parts of the market like the UK, EM and China. There is exposure to offshore markets in the portfolio which will help to offset Rand weakness and act as diversifier to the local holdings within the portfolio, helping protect against market downturns.

Let’s compare some of the other details of this portfolio

A few important characteristics to highlight about the portfolio is that it is not a Regulation 28 portfolio, returns are not guaranteed, and the target income withdrawal is 4% - 5%.

Since its inception, the Morningstar Moderate Income portfolio has generated a 10.4% annualized return for clients.

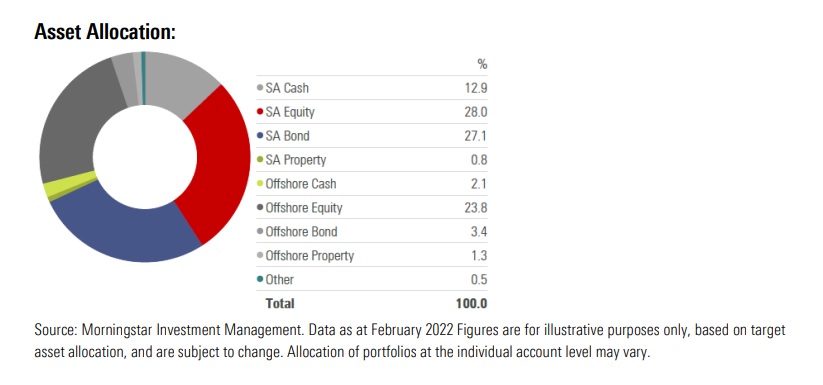

Asset Allocation and underlying fund managers for the Morningstar Moderate Income Portfolio:

Underlying fund managers

• Aylett Equity Prescient

• Ninety One Diversified Income

• Fairtree Equity Prescient

• Nedgroup Inv Core Bond

• Methodical Equity Preserver

• Ninety One Global Franchise FF

• Coreshares S&P SA Top 50

• Nedgroup Inv Core Global FF

• Coronation Strategic Income

In Closing

As we move through this latest period of market volatility, make sure you know how much you are paying and decide if it is good value for the investment performance you are getting and/or expecting in return.

When it comes to retirement planning, we encourage investors to speak to their financial adviser, who will be best suited to help them get the most out of their hard-earned savings and investments.

At Morningstar, extensive research has been done over the years to show that good financial advice can add around 2% per annum in additional returns to investors. Morningstar termed this value added by good financial advice as “gamma”. Please see our research report “Alpha, Beta and now...Gamma” for more detail.