RA or TFSA? - Maximising after-tax returns

Francis Marais, Research & Investment Analyst at Glacier by Sanlam

The end of the 2016 tax season is fast approaching and financial services companies are very active in promoting their respective tax-free savings accounts. This is of course a good thing as we should all be saving more and investing through a tax-free savings account is a very tax efficient way of ensuring maximum after-tax returns for your clients’ hard earned rands.

The goal of financial intermediaries and wealth managers should ultimately be to maximise after-tax returns, and merely focusing on pre-tax investment returns is simply not sufficient. This is particularly important for affluent individuals.

The question then ultimately becomes: how can we maximise our clients’ after-tax investment returns? Fortunately, in South Africa, we have a few tools to help with achieving maximum tax efficiency. Some are explicit tax savings vehicles while some are less explicit, but worth keeping in mind.

In this article I will focus on two of these tools, namely a Retirement Annuity (RA) and a Tax-Free Savings Account (TFSA). I will also attempt to show that for those investors with a current high marginal tax rate it is beneficial to start off with maximising your RA contributions before you start to maximise your TFSA contributions.

Before we start, it is important to make a clear distinction between tax avoidance and tax evasion. Tax evasion is of course illegal, and in no way acceptable. We should all be responsible citizens and contribute appropriately, this goes without saying. From an investment perspective, tax avoidance is to avoid paying unnecessary taxes due to sub-standard investment planning. All citizens have a right to reduce their tax burdens within the ambit of the law. Naturally this article aims to assist intermediaries with minimising tax burdens, not evading tax.

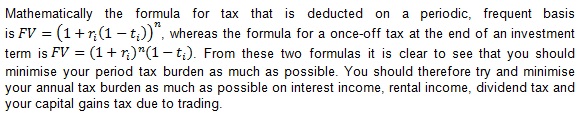

So let’s start and review some simple aspects regarding the effect of tax on your investment returns. Firstly, tax can either be deducted periodically (yearly) or at the end of an investment term (once-off). If it is deducted annually, you have a compounding effect, so the value of your investment will be less, versus a once-off tax deduction at the end of your investment term. Annual deductions from an investment would include tax on interest, dividends and also capital gains tax - should you have sold any investments during the year and realised a capital gain. A once-off tax at the end of an investment period would include capital gains tax on a buy and hold strategy, but also other types of tax such as estate duty.

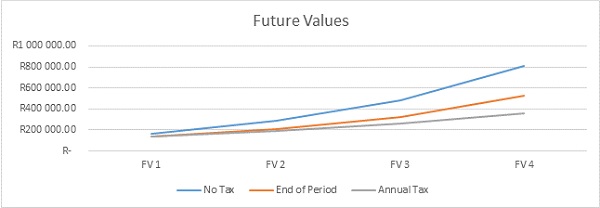

Graphically the difference between the two can be shown as follows:

For the example above, I have taken an initial investment of R100 000 over four different terms. The first term is five years, the second term is 10 years, term three is 15 years and term four is 20 years. Using an expected return of 11% per annum, one can clearly see the effect of no tax, the effect of only having to pay tax at the end of an investment term and the effect of tax being deducted annually and therefore being compounded. A further insight is that the longer the investment horizon the bigger these differences become.

It is clear to see that you would be making a mistake. If you only focus on pre-tax returns as can be seen in the table below that plots the differences between the various strategies for the 20-year investment horizon.

Investing in either a Tax-Free Savings Account (TFSA) or a Retirement Annuity (RA) effectively mitigates your risk of an excessive tax burden and is therefore a tax-efficient way of saving. Choosing either one of these products is therefore a “no-brainer”, but how would we go about deciding which one to choose?

We have already established that the effect of minimal or no taxes becomes much more apparent the longer the investment time horizon, so in the first instance one should make sure that your client’s investment time horizon for the two products is relatively long, in order to gain maximum benefit. With regards to an RA, this longer time horizon is relatively certain as this is mandated by law; however, this is not so with a TFSA where you can withdraw your money relatively easily. Therefore the full benefits of a TFSA will require some discipline. If your intention is to save for retirement using any one of these two products, make sure you can make the necessary commitment, and if not, then the RA is your best option.

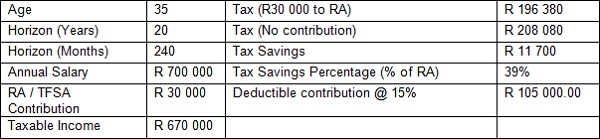

A major difference between an RA and TFSA is the fact that your contributions to an RA are tax deductible (up to certain limits), but when you eventually start drawing an income from your annuity, the entire amount will be subject to your personal effective income tax rate at that specific point in time. So for instance, let’s assume a hypothetical client, age 35, who earns an annual salary of R700 000. As per the 2015 (28/02/2015) tax tables he will be taxed at a marginal tax rate of 39%, but at an effective tax rate of around 29% (if he or she does not contribute to any retirement savings products that are tax deductible). For comparison’s sake, let’s assume this client now wants to start contributing an annual amount of R30 000 to either a TFSA or an RA. Below is a table summarising the hypothetical client detail. Which one should he choose?

If the client has no savings plan and is only able to save R30 000 per year, which one should he choose?

In this example, the client should choose to invest his annual R30 000 into his RA, as he gets a comparative tax advantage by investing through his RA versus a TFSA.

Why the big difference? It stems from the fact that a R2 500 contribution to the TFSA is equivalent to a R4 098.36 contribution to your RA, i.e. R2 500 / (1-0.39). Naturally when withdrawing from the annuity in the future you will pay income tax. If the tax rate paid while saving exceeds that of the tax rate paid when you withdraw, you have a comparative tax advantage. Note that the drop-off at the end of the period in the RA value represents the tax payable on income withdrawals. (For ease of reference this was done as a once-off deduction. In reality, two-thirds will be invested in a living annuity where tax will be deducted on a monthly basis, further extending the tax benefit.)

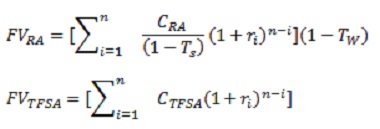

Mathematically, it can be presented through the following equations:

Where CRA is the contribution to the RA; Ts is the tax rate applicable while saving; TW is the tax rate applicable at withdrawal; CTFSA is the contribution to Tax Free Savings Account.

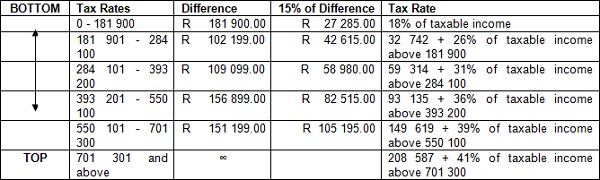

The tax rate at withdrawal will be different due to the fact that, while saving, you save at your marginal tax rate (or very close to this), but once you start withdrawing from your annuity you will pay tax at your average effective tax rate, while also benefitting from tax-free withdrawals (currently the first R500 000 can be withdrawn tax free). Another way of looking at this is that your RA contributions first start working from a top-down perspective, by first reducing your most “expensive” income, while at retirement your tax liability is calculated from the bottom-up, starting with your least “expensive” income.

From the table above it is clear that the current total contribution of 15% is not sufficient to decrease your weighted marginal tax rate by any significant margin. Should the 15% change to 27.5%, it will have an impact, but even then the same concept applies that while saving through an RA your most expensive income will be reduced first, and at withdrawal the opposite is true. A caveat associated with this is that when you currently face low marginal tax rates, but expect this to materially change in future you should ideally try and maximise your contributions to a TFSA and as your marginal tax rates increase, you should increase your contributions to your RA.

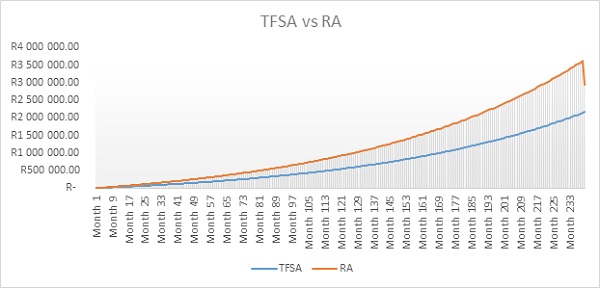

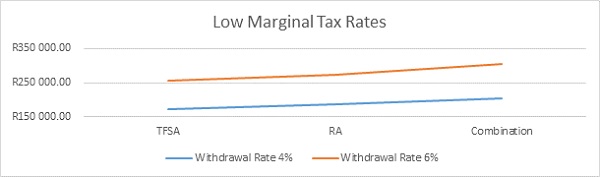

Below I show that an investor who starts off at the lowest marginal tax rate (18%) and earns a 6% annual salary increase, will be better off by first maximising his contribution to his TFSA and then save what is left of his savings budget (27.5% - % contribution to TFSA) in his RA. As the graph also shows, when used in isolation the RA still outperforms, but the combination where the contribution to the TFSA is maximised first, will deliver a superior outcome.

It is true that there are a myriad of other considerations when choosing between a TFSA and an RA. For instance, investments in an RA need to be Regulation 28 compliant. This is a constraint that might detract from investment returns, while investments in a TFSA are free from these type of constraints. Furthermore your annual contribution to a TFSA is limited to R30 000, so depending on your level of income this might be insufficient. Additionally, for some very affluent individuals the majority of their retirement savings may be in large concentrated positions, outside a formal retirement product, such as company stock options, private businesses and private property. This could result in large annual income withdrawals in future, increasing the individual’s effective tax rate and thereby undermining the potential tax benefits of an RA. Lastly, from an estate planning perspective it is important to note that your investment in an RA is safe from creditors’ claims while an investment in a TFSA is not.

The point of this investigation is that there are certain tax benefits when investing in an RA versus a TFSA, especially for affluent individuals with high marginal tax rates, and this needs to be acknowledged. Ideally one should not have to make a decision between the exclusive use of either one or the other. As mentioned previously in this article, your annual tax liability should be reduced as much as possible and in order to achieve this goal, both an RA and TFSA can be used as tools or strategies in conjunction with one another. Ultimately, when saving for retirement, clients should try and maximise their contributions to an RA first, and when faced with either the 15% limit (27.5% as from 1 March 2016) or the maximum annual contribution of R350 000 as from 1 March 2016, try and maximise their contributions to a TFSA.

What type of investments should you include in your RA or TFSA? Preferably those types of investments with high annual tax liabilities, such as high interest investments or bonds (taxed at personal tax rates), property (taxed at personal tax rates), high dividend-yielding stocks (taxed at 15% dividend withholdings tax) and actively traded share portfolios (available through an RA on our platform but not through a TFSA).

Property is a particularly interesting choice, especially when investing through REITs, as qualifying REITs deduct their distributions from gross income, before tax. Therefore any qualifying REIT income received in your TFSA or RA is essentially 100% tax-free, as no tax would have been paid on either the REIT level or investor level.

In summary, for those with high marginal tax rates it is advantageous to utilise the maximum allowable contributions to your RA first, and then start maximising your TFSA contributions. For those clients with lower marginal tax rates the opposite is true as there is a large probability that their future marginal tax rates will be higher, increasing their future effective tax rates. I have also indicated that using the two in combination can deliver superior results and that it should not necessarily be an either/or choice. Lastly I briefly touched on some differentiating aspects that one should also keep in mind when deciding between the two.