Living annuitants at risk of destitution

Deane Moore, CEO of Just Retirement South Africa.

Carlene Vollenhoven, Sales Executive, Just Retirement South Africa.

“South African retirees are hurtling towards destitution in their old age by blindly following the misguided ‘collective wisdom’ of the herd”, says Deane Moore, CEO of Just Retirement South Africa.

“We need to debunk the myths of the herd,” he says. These include:

• Investing 100% of your retirement benefits in a living annuity is a good option provided you don’t draw more than 6% initially. This is not true, as retirees are likely to hit their drawdown cap of 17,5% before they die.

• Death benefits are too costly in retirement, so investing 100% of your retirement benefits in a living annuity is better. This is also not true. In a living annuity retirees self-insure their death benefits in the early years of retirement at the cost of the income they will need to survive on in later years.

• Advisors can earn greater remuneration by recommending clients to invest 100% of their retirement benefits in a living annuity. Not true. In fact, both client outcomes and total advisor remuneration can be simultaneously improved by combining a living annuity and an enhanced with profit annuity to meet the specific, and different, needs for which each was designed.

Using enhanced with profit annuities and living annuities for their intended purpose

In retirement you require income to meet your basic needs: food, accommodation, water, electricity and communication. It is reckless to gamble your life savings on a living annuity being able to meet these needs over your lifetime, given that it provides no guaranteed future income. An enhanced with profit annuity has been specifically designed for that purpose. It guarantees a monthly income that never decreases, no matter how long you and your spouse survive or what happens in investment markets. Your income increases each year by an amount linked to the performance of an investment portfolio managed by best-of-breed asset managers, which is targeted to be in line with inflation. And you may qualify for an enhanced income if you live with certain medical conditions.

Living annuities have been designed for the surplus assets not required to meet basic living expenses. Here you can afford to invest a substantial portion in growth assets to maximise the long term investment return, and not worry about short term volatility. These assets are available to draw on if unexpected expenses materialize, and any assets not used during your lifetime are available to your beneficiaries. It was never designed to be a one-size-fits-all solution for every retiree in every circumstance.

A practical example

Carlene Vollenhoven, Sales Executive of Just Retirement South Africa, illustrates how investing 50% of retirement fund benefits in an enhanced with profit annuity and the remaining 50% in a living annuity can provide better client outcomes than investing 100% of the benefits in a living annuity:

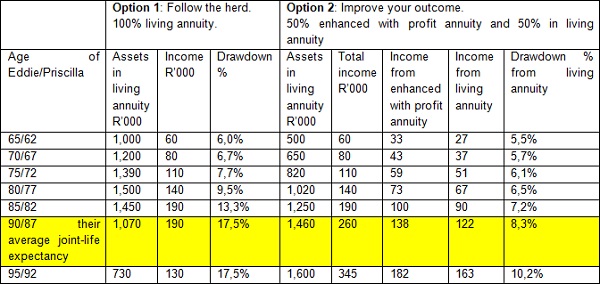

Steady Eddie retires at 65 with R1m in his retirement fund. His spouse, Practical Priscilla, is 62. They are both in good health and should expect at least one of them to be alive for 25 years or more. They need R5,000 per month (R60,000 pa) to cover their essential expenses, and this does not change if one dies. Their advisor shows them two options to compare:

Option 1: Follow the herd to destitution

Invest the full R1m in a living annuity and draw R60,000 pa and increase this each year with inflation.

To balance the need for short term income with long term growth, the advisor suggests a moderate risk investment portfolio.

The advisor takes a fee of 0.5% pa and no upfront fee.

Option 2: Improve your outcome by matching needs to products

Invest R500,000 in an enhanced with profit annuity that pays R32,500 pa and targets annual increases in line with inflation; and R500,000 in a living annuity, from which they draw R27,500 pa (to make up the R60,000 pa they require at the outset, increasing annually with inflation).

The guarantees provided by the enhanced with profit annuity allow them to invest their living annuity in a portfolio more strongly focused on long term growth that targets an additional 1% pa in investment return. (Typically asset managers suggest that 10% higher equity content is expected to generate an additional 1% pa return in the long term).

The advisor takes a fee of 1.5% upfront on the R500,000 invested in the with profit annuity and 0,7% pa on the amount in the living annuity. Because the living annuity is focused on long term growth, there will be more active advice each year.

This is how the income and assets available in the living annuity escalate over time under the two options:

By the time Steady Eddie and Practical Priscilla reach their life expectancy, option 2 is generating 35% higher income (R260,000 compared to R190,000) and has 40% more assets available for a rainy day or beneficiaries (R1,46m compared to R1,07m). Furthermore, under option 1, they would face a future of destitution, capped at a 17,5% drawdown rate on dwindling assets. Meanwhile, the advisor earns approximately the same remuneration up to that date under option 1 and 2.

The reasons why option 2 performs better are:

• The additional 1% pa investment return generated by the higher proportion invested in growth assets helps the living annuity in option 2 to grow significantly faster.

• The income from the enhanced with profit annuity is guaranteed no matter how long they survive and what happens to investment markets. This allows a lower drawdown rate from the living annuity in option 2, and a sustainable income should they survive beyond their life expectancy.

Option 2 is also lower risk. In the event of a market crash, the enhanced with profit annuity smoothes this over a six-year period. However, under option 1, they are required to increase their drawdown rate to receive the same amount of required income for the year. This means there are less assets available to benefit from any subsequent recovery in the investment markets.

This realistic example reflects the circumstances of the majority of retirees who purchase living annuities. The same methodology can be used to show that even retirees with a drawdown rate of 5% who could shift 5% of their portfolio towards growth assets would benefit by combining an enhanced with profit annuity and living annuity.

If the client is one of the 40% of the population who qualifies for enhanced income due to ill health and lifestyle factors, they could achieve an even better outcome.

The living annuity accident waiting to happen

Living annuities became popular in South Africa in the 1990s. Many who bought living annuities are now in the age range 75 to 85. The above illustration demonstrates clearly how South African retirees are hurtling unsuspectingly towards destitution. Most would feel comfortable having a drawdown rate as low as 8% to 10% at that age, but the example shows how quickly this drawdown rate escalates once the income they need to draw exceeds the investment earnings after all fees and charges, and assets start to decrease each year.

In most cases, retirees do not realise the urgency of considering the relative merits of an enhanced with profit annuity compared to a living annuity. The former provides a guaranteed income for life, and the potential for enhanced income for those who are ill. To qualify, an individual must take up or convert to an enhanced with profit annuity before age 85.

Just Retirement is extremely concerned about this vulnerable portion of the retired population who may be denied the opportunity of additional comfort in their advanced years. Retirees invested in living annuities who are between age 75 and 85 can potentially avoid the risk in the above illustration by taking the first step and requesting a quote for an enhanced with profit annuity.