Ideal for Living Annuities: The Glacier Invest Real Income Solutions

In this article we discuss how the construction of the Glacier Invest Real Income Solutions for Living Annuities make them ideal for post-retirement clients who draw an income from their investments.

We’ll show you where these solutions fit into our holistic discretionary fund management (DFM) offering – a comprehensive offering that covers the needs of a wide range of clients across a variety of life stages and risk profiles, providing you with the means to meet the needs of a diverse client base.

Where do the Glacier Invest Real Income solutions fit into the bigger picture?

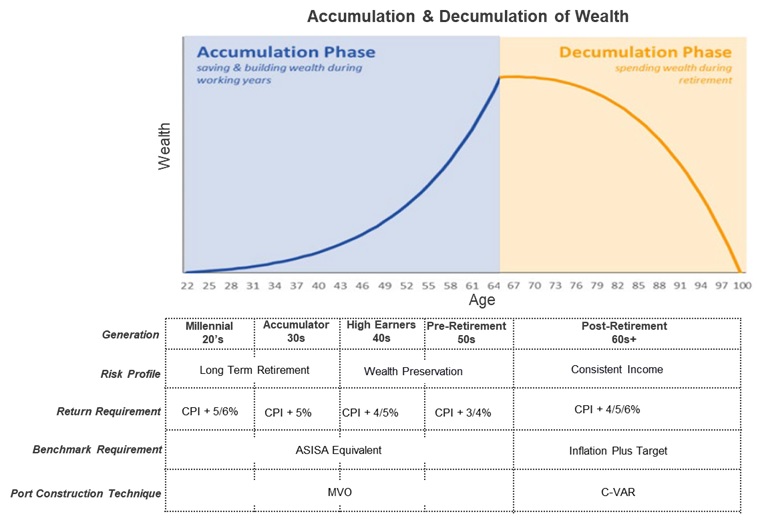

The Glacier Invest Real Income Solutions are specifically created for clients with living annuities and are therefore specialist retirement income portfolios. Below is a graphical depiction of clients’ investment life stages and the corresponding return requirements and portfolio construction techniques.

It is important to note a few key points:

First, take note of the suggestion that clients in their 20s, 30s and 40s should invest in fairly aggressive and high growth investment portfolios, assuming they have the risk tolerance for that. As clients start moving into their fifties, it may be prudent to move them into more moderate or medium growth and medium risk portfolios, to start focusing more on preserving wealth for their retirement. These life stages are covered by the range of portfolios we manage in collaboration with financial intermediaries through our investment consulting services and the regular investment committee meetings we have with financial intermediaries.

We suggest that retired clients should move into specialist retirement income portfolios, designed to be specifically for this part of a client’s investment lifecycle: The Glacier Invest Real Income Solutions.

The bottom row of the table above is labelled “Portfolio construction technique”. You will note that we use a construction technique called Mean Variance Optimisation (MVO), for pre-retirement portfolios, but the technique changes to the Conditional Value at Risk Optimisation Approach (CVaR) after retirement. This is the technique used for the Glacier Invest Real Income Solutions.

The link between asset allocation and portfolio optimisation

Why a change in the portfolio construction approach is so important when designing and managing retirement income portfolios

Asset allocation is of course the process of dividing investments among different kinds of asset classes such as equities, bonds, property, cash, etc. The aim is to achieve the best combination of asset classes that will lead to risk and reward outcomes consistent with an investor's specific situation and goals.

And portfolio construction is the process of assigning a weighting to each chosen asset class and choosing the appropriate investment funds within each asset class to underlie the portfolio, so investors get the best possible return for a given level of risk.

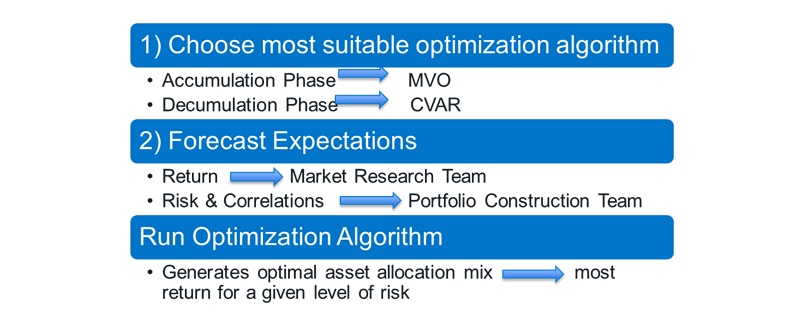

The portfolio construction process consists of three general steps:

• In the first step we choose the type of optimisation algorithm to use, depending on what we are trying to achieve. For example, if we’re designing a portfolio for the accumulation phase of a client’s investment lifecycle, we use MVO, as mentioned. And if we’re designing a portfolio for the decumulation phase, during which a living annuity client will be drawing income from their investment, we use the CVaR approach.

• In the second step we model the forward-looking assumptions for each asset class in terms of projected return and risk, as well as co-movements or correlations among the asset classes.

• In the third step we run the chosen optimisation algorithm which generates percentage allocations to the different asset classes, to create the most efficient asset allocation.

Why use different portfolio construction approaches during different phases?

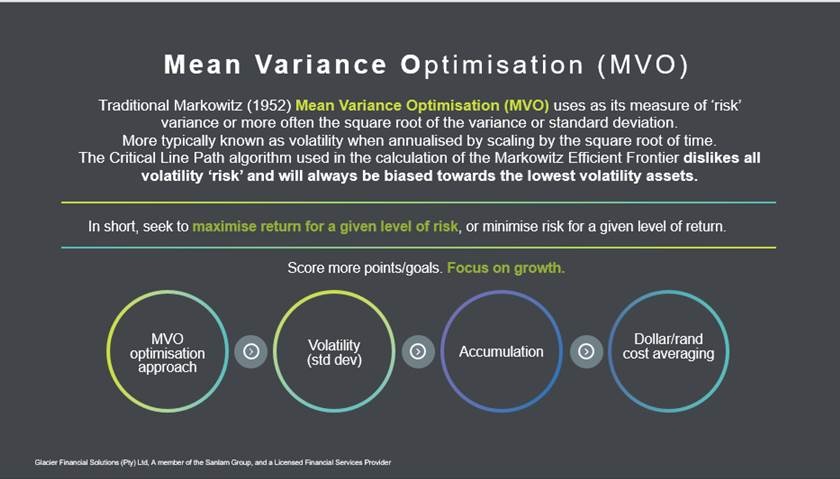

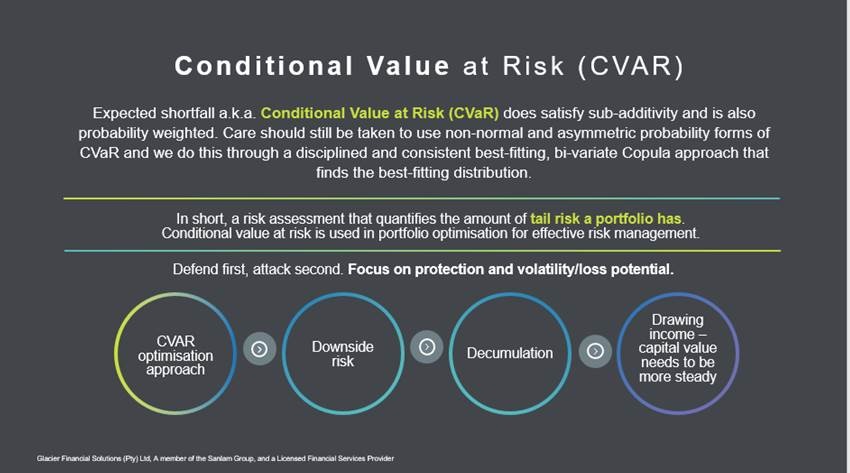

The difference between the two optimisation approaches is that MVO focuses on reducing overall volatility, in other words the standard deviation of the portfolio, whereas CVaR focuses on managing downside risk.

Portfolio volatility has a much greater negative impact on a post-retirement portfolio from which a client is drawing income, than on a portfolio in which a client is accumulating assets pre-retirement. To demonstrate, let’s refer to the diagrams below.

A basic rule of investing is that a long-term dollar or rand cost averaging strategy is self-correcting. As long as the investor keeps investing a steady amount of money month after month and year after year, the average return should be solid. So, when accumulating assets, volatility can actually be an investor’s friend. This is because when you are slowly adding money to your portfolio each month, it allows you to also buy investment assets that have had a big drawdown and are therefore cheaper. Take the example of the impact of the COVID outbreak on the markets last year: People who were contributing money to their retirement savings portfolios from April to October last year, were buying assets at bargain prices. And although the drawdown temporarily impacted the rest of their investment assets, these then recovered along with the newly bought assets.

After retirement, an investor doesn’t contribute money to their investment anymore, but instead withdraws money on a regular basis. If the market happens to be bullish, their withdrawals will be offset - at least in part - by new gains, depending on their income drawdown rate. However, in a bear market, each withdrawal takes a bite out of the investment and is not offset by new deposits. The client is essentially then taking an amount of cash each month out of an account that is steadily shrinking in size. Therefore, we need to be much more focused on protecting the downside in living annuity portfolios where clients are drawing an income, and that is what the CVaR approach to portfolio construction allows us to do.

Conditional Value-at-Risk

What this optimisation approach achieves for us when we construct retirement income portfolios

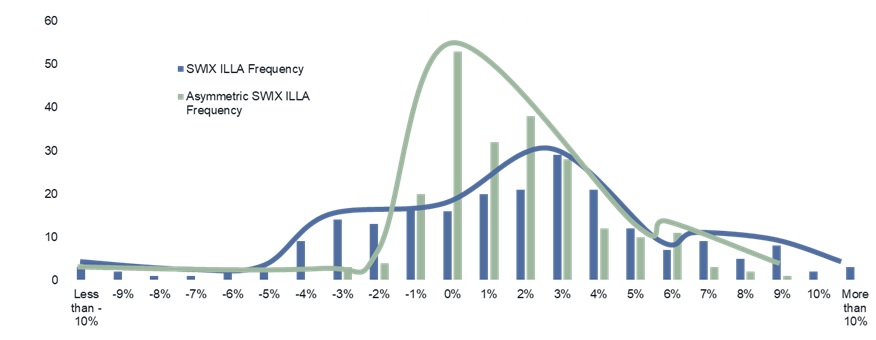

Looking at the dark blue vertical bars in the diagram above: The X axis represents monthly returns, ranging from less than -10% to 10% plus. The Y axis represents the percentage of months in the past that a particular return was achieved. For example, the tallest dark blue column indicates that roughly 30% of the time, the return of the JSE SWIX index is about 3% per month. Note that in the negative tail of the distribution, there are many months where the portfolio has significant negative returns of 8%, 9%, 10% or more, and those are the ones we want to avoid for retirement income portfolios, for reasons already discussed.

The CVaR optimisation approach enables us to construct portfolios that have a distribution of monthly returns that looks more like the distribution represented by the green bars on the chart. You will note that this distribution cuts the returns below -3% for the most part.

Inclusion of non-traditional assets for diversification

It is not only the optimisation method used that helps us protect downside risk. We also need to generate enough return in these specialist retirement income portfolios to protect a client’s portfolio from inflation and fund an income of 4%, 5% or 6% per year. Within a living annuity life wrapper, we can include asset classes that are uncorrelated with more traditional asset classes like equities, bonds, property, etc. Many of these alternative assets – such as private equity, private debt, and unlisted property - also enhance the returns of the portfolio better than their more traditional counterparts.

Within these portfolios, we also include asset classes that act as great diversifiers and downside protectors, such as hedge funds, infrastructure and smooth bonus funds.

Bringing it all together

We combine these three aspects: the return enhancers, the diversifiers, and the CVaR optimisation approach to create the Glacier Invest Real Income Solutions. These three aspects make for portfolios that have much lower downside risk than more traditional ASISA category average type portfolios, without leading to lower returns.

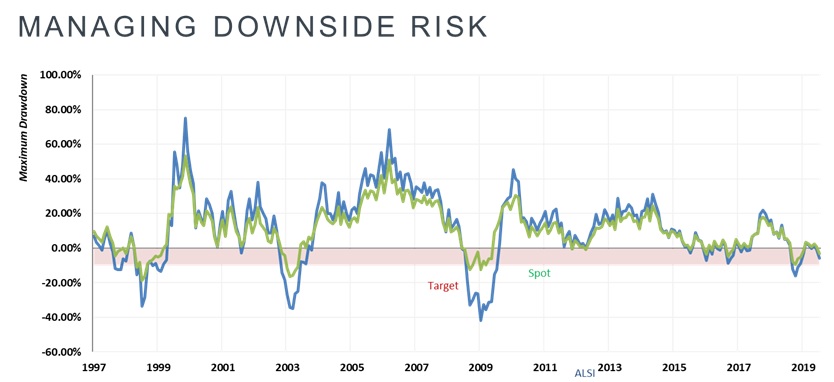

The rolling one-year return series of these portfolios therefore look more like the light green line in the chart below, than the blue line depicting the return of a more traditional portfolio.

We hope this article has provided sufficient insight into the portfolio construction methodology used in the Glacier Invest Real Income Solutions. Please get in touch with your Glacier Invest representative should you require any further information in this regard.

Glacier Financial Solutions (Pty) Ltd is a licensed discretionary financial services provider, trading as Glacier Invest FSP 770

Sanlam Multi Manager International (Pty) Ltd FSP 845 is a licensed discretionary financial services provider, acting as Juristic Representative under Glacier Financial Solutions (Pty) Ltd

Glacier Invest is the discretionary fund management offering of Glacier Financial Solutions (Pty) Ltd (“Glacier’’). Glacier has partnered with Sanlam Multi Manager International (Pty) Ltd, part of the Sanlam Investments Group, to optimise the investment management responsibilities