How a salary cut or reduced income could affect your retirement fund

Many South Africans have lost their jobs in 2020 and more still fortunate enough to be employed, face salary cuts or reduced hours of work, as companies and organisations try to survive a profoundly challenging economic year.

However, a reduced retirement fund contribution is better than none at all.

Less really is better than none

A reduction in your salary probably means that you will reduce your monthly contributions to your retirement fund. This is not the end of the world, says Dinash. Continuing to make any contribution will only help to strengthen your financial position when you retire. It’s also helpful to remember that the reduction may not be permanent, so when your salary increases again, your contribution can increase.

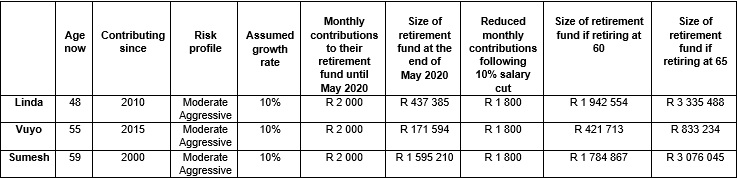

We know that the financial knock-on effect of a salary cut is far-reaching in the medium term, but what of the long term? Your retirement fund is meant to be an income during your retirement, so what happens when you reduce your contributions?

Let’s look closely at three employees – Linda, Vuyo and Sumesh – and how reduced contributions would impact their employee retirement savings.

• We’re all in the same storm but in different boats – while we may be facing the same crisis, every person is unique with their own set of financial circumstances.

• In each of the scenarios, staying invested, even with a reduced monthly contribution, has significant positive financial outcomes in the medium and long term.

• Any adjustment to your retirement savings – negative or positive – has an impact on your financial future.

What to do if you’re facing a salary cut

1. Get help from a financial adviser

This truly is the best time to talk to your financial adviser. There are some big, important financial decisions to be made, and your qualified financial adviser can help you make them with confidence. This could include revisiting your budget, your debt repayments and your retirement plan in light of your reduced income.

2. Cut your household budget

Bills will continue to reach you, while your income will have reduced in size. Now is the time to go through your monthly household budget with a fine-tooth comb. You need to be strict and clinical about the expenses that are unavoidable (e.g. your bond repayment or kids’ school fees) and those that are luxuries and can be eliminated – at least for a while.

3. Contribute to your retirement fund for as long as possible

Your retirement savings is your money, but not for today. Early retirement may be tempting, especially if you’re nearing retirement age. However, if you are able to continue to work – and contribute to your retirement fund, even with a reduced salary – that would be first prize.

4. Speak up

Don’t be embarrassed to ask for better interest rates, reduced instalments on your accounts or even payment holidays if you are feeling the pinch of a reduced income. Whatever you do, don’t ignore your debt obligations. If you are struggling to keep up your debt payments, a conversation with the credit manager at your bank or a debt counsellor will go a long way in preventing judgements and blacklisting.

5. Early retirement

While it’s wise to work for as many years as you can and, in so doing, contribute to your retirement fund for as long as possible, the reality is that many employers are offering early retirement to their employees. If you have decided to take up this option, there are a few decisions you would need to make regarding the funds that you have worked so hard to accumulate over the years. Don’t make these decisions alone – a financial adviser can help. Together, you can decide how the money will be invested to ensure that you have the best financial outcome during your retirement.

Glacier Financial Solutions (Pty) Ltd and Sanlam Life Insurance Ltd are licensed financial services providers.