Get Rewired for retirement™ with Assupol

Life after retirement requires adjustment – both psychologically and financially.

Assupol’s Ultimate Retirement Income 4Life (URI 4Life) offers retirement-income solutions to help clients match their expected post-retirement spending. The URI 4Life product provides a guaranteed monthly income and includes features like:

• An increase percentage can be selected to make sure that the guaranteed level of monthly income increases every year to better keep up with inflation.

• A guarantee term ensures that the client’s spouse and dependents will continue to receive an income if the client dies before the end of the guarantee term.

• A spouse income option ensures that a percentage of the guaranteed monthly income continues for the surviving spouse after the client’s death.

• Capital protection - the full or a percentage of the initial investment amount can be protected so that on the client’s death, beneficiaries receive a percentage of the initial investment amount. This is useful if leaving a legacy is important.

But, for the many people with insufficient retirement savings, they will have to adjust their spending during retirement. Assupol has a solution that may assist with this.

Assupol’s Rewirement feature provides clients who may have under-saved for retirement with a mechanism that allows them time to adjust their spending to better match their retirement-income. This may be a valuable tool to help clients make the necessary adjustments in their spending habits, instead of opting for sub-optimal long-term choices like a level life annuity or living annuity:

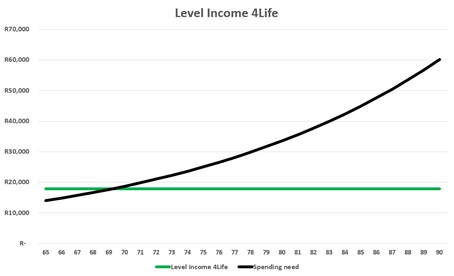

• The level life annuity provides a higher income initially, but it does not increase yearly to keep up with inflation.

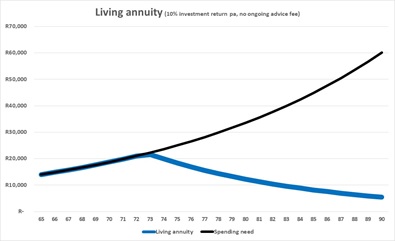

• While with a living annuity, if adjustments in spending are not made, the drawdowns taken may deplete retirement savings and not leave much for later in life.

Let’s consider an example:

- Mr. Malatji is 65 years old and he has R2m in retirement savings.

- He earned a gross salary of R224,000 per annum when he retired (R18,667 per month).

- He estimates that he needs around 75% of his pre-retirement income per month (R14,000 gross per month) to address his spending need, that is expected to increase by 6% per year.

- His retirement savings as a multiple of his annual salary at retirement is just below 9 times – which is probably on the low side.

He considers the following products to provide him with a retirement income:

1. A life annuity providing a level guaranteed income.

2. A life annuity providing an increasing guaranteed income (by 6% per year).

3. A living annuity where he chooses drawdowns in line with his spending needs.

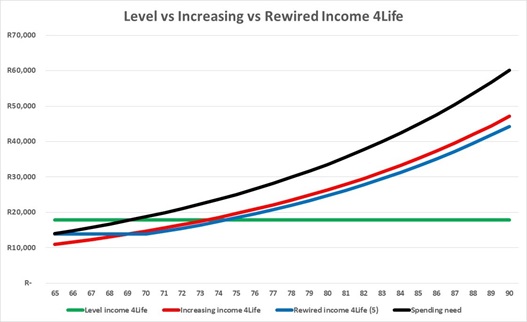

Option one, the level life annuity, will initially provide an income above his spending needs, but after a few years, his spending will have increased along with inflation and he may face problems if he doesn’t have other sources of income or support.

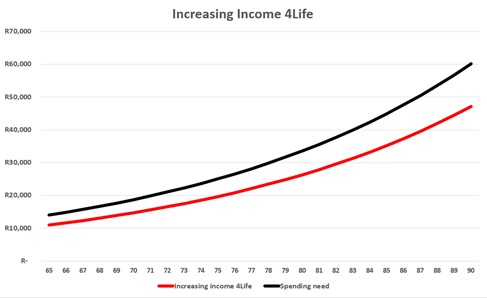

Option two, the increasing life annuity, will require an immediate adjustment in spending, because the guaranteed monthly income will start lower than his estimated spending need. One positive is that his income will increase every year and at least keep up with inflation – so this may be a better long-term solution.

Option 3, the living annuity, allows him to withdraw what he needs. If he is not disciplined and simply withdraws what he needs, then, because he under-saved for retirement, there is a risk of him depleting the capital in his living annuity and his income decreasing later in life.

So, options one and three may be sub-optimal over the longer term.

Option two may be a better long-term solution, but a lot of pain must be taken initially (immediately in the month after retirement spending must cut by 20%-25%). For many, this is too much, and sub-optimal choices are made.

Rewired for retirement™ is a new concept from Assupol.

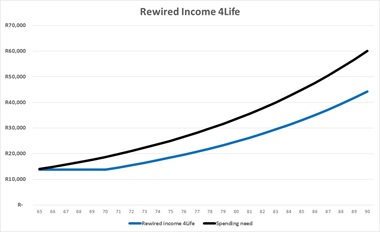

Assupol’s Rewirement feature combines a level and an increasing life annuity. Any Rewirement factor up to 10 can be chosen. The bigger the Rewirement factor chosen, the higher the retirement income will start at. But, the trade-off is that the retirement income will remain level for an initial period and a number of yearly increases in the retirement income will be skipped. The number of increases that will be skipped is equal to the Rewirement factor chosen.

So, Mr. Malatji also has another option – he could choose a guaranteed monthly income with a rewirement factor of 5. His income will start at the level he needs (around R14,000 per month), but because he will skip 5 yearly increases, he will have to start to make adjustments in his spending. Only after 5 yearly increases have been skipped will his guaranteed monthly income again start to increase by 6% per year.

By then, we believe his spending would have been “rewired” to this level that his guaranteed monthly income can afford.

Also, very important is that none of the investment risk, or the risk of outliving his retirement savings (longevity risk), will be with Mr. Malatji.

Save enough for retirement

If Mr. Malatji had a healthier level of retirement savings of around R4m (this is around 18 times his annual salary at retirement), he would have been able to opt for an increasing life annuity without using the Rewirement feature (Rewirement factor = 0). So, his income would have immediately started to increase every year after retirement, and less adjustment in spending would have been required.

This shows that the Rewirement factor of between 0 and 10 is a tool that can be used by all people to set their initial retirement income at a more comfortable level, and from there adjustments in spending can be made over time. Using the Rewirement factor, the initial monthly income can be set to any level between those offered by the traditional level and increasing life annuities. The URI 4Life offers all these combinations.