Emerging markets and pension funds: Do they mix?

William Ball, Senior Equity Analyst at Sanlam Private Wealth.

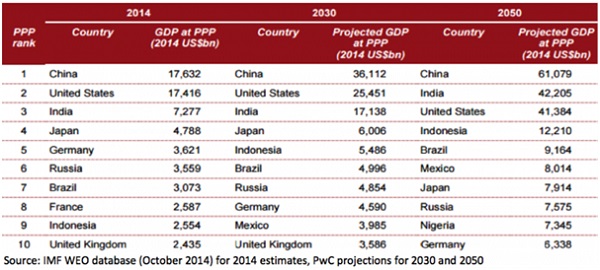

Over the past 25 years, the rise of emerging markets has transformed the global economy and the way investors allocate capital. Emerging markets have become increasingly synchronised, reflecting their enhanced integration into global trade and capital flows, with China at the epicentre of this shift. As measured by purchasing power parity (PPP), China has risen from less than 3% of total global economic output in the early 1980’s to around 16% in 2014!

Many of these countries are forecast to grow significantly over the decades to come. According to the International Monetary Fund (IMF) and PricewaterhouseCoopers (PwC), developing economies are set to incrementally increase their share of global GDP on a PPP basis.

Capital has flowed into emerging markets over the past two decades, as institutional and retail investors bought into the ‘growth story’ and increasing relevance of these economies within a global context. Nonetheless, there are ominous signs that the spectacular rise of the developing world is starting to unravel, with emerging markets suffering a net outflow of capital in 2015 for the first time since the 1980s. Part of this is down to the US Federal Reserve raising interest rates, the significant moves in the US dollar and the effects of quantitative easing on risk assets over the past 18 months.

So where does this leave emerging markets in terms of its allocation within portfolios?

From our perspective the most important point is not where a stock is listed but the breakdown of where it generates its revenue. Our style bias towards owning high quality businesses with high free cash flow conversion ratios, attractive operating margins and high returns on capital at reasonable valuations has led us away from direct emerging market exposure. Even though we have minimal direct emerging market exposure, on a revenue look-through basis we have almost 20% exposure through the multinational companies we hold in our global equity portfolio.

Furthermore, an important consideration is that there is not necessarily a discernible link between economic growth and investment returns. That said, as can been seen from the capital flows into emerging market equities and debt since the turn of the millennium, investors have allocated significant capital into these economies in search of investment returns and yield.

It is unsurprising that the end of quantitative easing in the US and subsequent strength of the US dollar along with the US Fed raising interest rates has led to the flight of capital out of emerging markets. This perhaps confirms the premise that investing in emerging markets is inherently more risky than the developed world. As a consequence–it was to be expected that many retail and institutional investors would reduce their direct exposure to emerging markets.

All of this has brought allocations to emerging market risk assets down to multi-year lows and no doubt many investors’ preference is to gain exposure through developed market companies. Over the long-term this dynamic will likely change as emerging economies and their capital markets develop.