Eating a R1 million dinner

Yanga Nozibele, Investment Associate at Cannon Asset Managers

If you received a R1 million bill with your restaurant dinner, your jaw would likely hit the floor. But what if you knew that your weekly takeout meals could be worth an extra million rand in your retirement pot?

This is because of the potent combination of compound interest and time, which can transform even small amounts into significant wealth. Compound interest is the process whereby your savings, and the interest earned on your savings, earn additional interest to become a powerful multiplying machine.

As a simple example of just how powerful compound interest can be, imagine that someone offered you the choice between winning R30,000 today or a magical cent that doubled in value every day for 30 days. At face value, the first option seems far more appealing. However, if you instead chose the magical cent that doubles every day, your winnings would gradually pick up momentum as the month went by, growing from just a few rand at the end of the first week to over R5.3 million by the end of the 30 days.

Table: The magical doubling cent

|

Day |

Value |

|

Day 1 |

1 cent |

|

Day 2 |

2 cents |

|

Day 3 |

4 cents |

|

Day 4 |

8 cents |

|

Day 5 |

16 cents |

|

Day 10 |

R5.12 |

|

Day 15 |

R163.84 |

|

Day 20 |

R5,242.88 |

|

Day 25 |

R167,772.16 |

|

Day 30 |

R5,368,709.12 |

Source: Cannon Asset Managers (2020)

Of course, there is no such thing as a magical doubling cent, and in reality, the process of earning compound interest on savings and investments works much more slowly, growing savings steadily over years and decades rather than all within the space of a month. But what the example shows is the power of what investors know as the principle of “compounding”.

How small savings on a takeout meal can transform into R1 million

Returning to our original example, consider if, at the age of 25 years old, you take a hard look at your budget, and make the decision that instead of spending R125.00 on takeout meals each week, or R500 a month, you will opt for home-cooked meals instead.

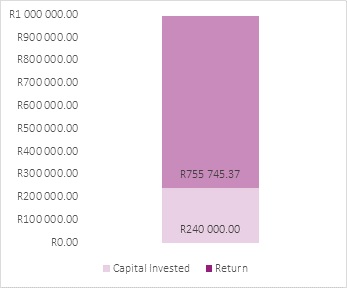

Crucially, you then make the conscious decision to invest these monthly savings instead. If you invested this money into an equity portfolio for the next 40 years, you would end up having saved a total of R240,000 towards your nest egg. But, if this portfolio then achieved average annual returns of 12% and inflation remained at 6%, by the time you retire at the age of 65 years, your investment would be worth a whopping R996,000 in real terms.

In other words, your weekly takeout alone could mean almost R1 million extra in your savings pot through the same potent combination of compound interest and time.

Graph: R500 invested monthly for 40 years

Source: Cannon Asset Managers (2020)

This example shows that even small amounts of money have the potential for exponential growth if invested correctly and given enough time. This is not to say that you shouldn’t treat yourself, but rather to encourage you to think twice before spending your hard-earned money. After all, manicures, expensive hairstyles, designer clothing and restaurants suddenly become far less appealing when you work out their multimillion-rand price tag in retirement.

The dark side of compounding

When it comes to compound interest, it is important to realise that while it can act as a force of good when put to work for savings and investments, it can also destroy your wealth if put to work against you through expensive debt.

If, for example, you have a credit card with a balance of R10,000 and your bank charges you 15% per annum in interest, you would owe R11,617 at the end of the year if you leave the balance unpaid. In other words, compound interest would mean that your debt would grow instead, preventing you from saving towards your financial goals.

Likewise, the idea of opening clothing accounts and being able to buy clothes whenever you want (rather than waiting for payday) is tempting. But, in reality, interest charges and service fees mean that a simple R100 T-shirt could end up costing you twice as much.

Ultimately, one of the most important financial lessons you will ever learn is that you don’t need huge amounts of money to build wealth – even small amounts can translate into significant savings if you begin investing wisely and as early as possible. Put compound interest to work for you by investing rather than have it work against you by spending on credit. And then give your wealth the time it needs to grow.