Don’t outlive your savings – choose the right annuity

04 June 2014 | Retirement | General | Warren Matthysen, Momentum Employee Benefits

There are many pitfalls to not saving effectively for retirement. Far too many retirees run out of money while others face a year-on-year decline in their standard of living as inflation and poor investment returns erode their income.

Warren Matthysen, Marketing Actuary at Momentum Employee Benefits, says: "The right annuity provides peace of mind for retirees who want to secure their current lifestyle post-retirement.”

Annuity options include living annuities and guaranteed annuities.

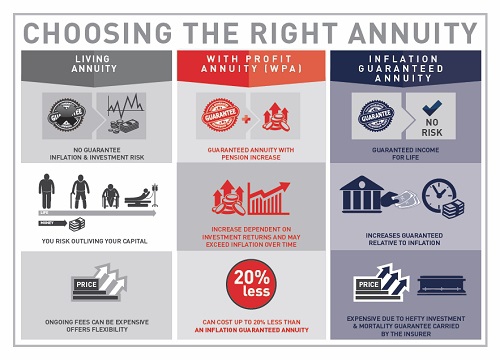

Matthysen explains: "Living annuity retirees carry inflation and investment risk as they make all the underlying investment decisions. As living annuities offer no protection against longevity, retirees also risk outliving their capital.”

"Retirees with funding shortfalls often choose living annuities as they hope to make up the deficit in the equity markets. They often draw down a high income initially, gambling on strong future investment returns to negate the risk of running out of money.”

Living annuities attract additional costs of the administration platform and ongoing financial advice, which can make them expensive.

Matthysen explains: "Living annuities typically suit retirees who have excess capital to finance their post-retirement income.”

Most retirees don’t have enough capital, so it’s surprising that living annuities account for 85% of inflows into retirement annuities. Even though a guaranteed annuity may be better suited to meet the income needs of the average retiree, it is not as well understood as an living annuity.

With guaranteed annuities, an insurance company guarantees to pay retirees an income for life. The cheapest option is a level annuity guarantee that offers retirees the same monthly income for life, with no increases.

"Retirees whose main source of post-retirement income is an annuity should consider an escalating guaranteed annuity. You can choose for your income to increase by a predetermined amount annually, or link increases to inflation to maintain a consistent standard of living”, explains Matthysen.

"These guaranteed annuities are expensive due to the cost of providing onerous investment and mortality guarantees. As retirees do not shoulder any longevity, inflation or investment risk, they are a better option than a living annuity for those expecting to live longer.”

"With profit annuities (wpas) are a guaranteed annuity, where pension increases depend on investment returns, similar to a living annuity. They differ from a living annuity in that the initial pension amount and all increases are locked in for life as the insurer provides a minimum investment guarantee equal to the retiree’s pre-selected annual interest rate. They provide an attractive option for retirees who are comfortable to link increases to investment returns, but want to enjoy the income guarantee from an insurance company.”

Although wpas do not guarantee inflation-linked increases, they have exceeded inflation over time. A wpa can cost up to 20% less than an inflation guaranteed annuity, so retirees can initially enjoy up to 20% more income.

"Retirement funding decisions are complex and often irreversible. Poorly understood options can leave many retirees with the wrong annuity product and increasingly vulnerable to poverty. If you’re not sure about the different options, an experienced and trusted financial adviser can assist”, concludes Matthysen.