Combining a tax-free savings account with your RA can extend your earnings by an additional 12 years in retirement

Combining your retirement fund contributions in, for example, your retirement annuity (RA) with a tax-free investment (TFI) could extend the period over which you will receive an income at retirement by as much as 12 years.

“Given the increasing longevity, ensuring that you receive an income up to the age of 89, rather than just 77, can make the difference between a comfortable old age and one fraught with worry and suffering,” says Tiaan Herselman, Head of Advice at Old Mutual Wealth.

Since interest, dividends and capital gains are not taxed while you remain invested in an RA, the product remains a great mechanism for investors to save for retirement. Furthermore, since 2016, investors are now also allowed to claim a tax refund of up to 27.5% of total annual income (capped at R350 000) if this is invested in a retirement fund.

Examples of retirement funds include pension and provident funds and retirement annuities. This significant tax deduction is an incentive for South Africans to top up their annual RA contributions.

While most South Africans end up spending this tax refund on some immediate need, Herselman believes that “we are missing a big opportunity in the tax-free investment (TFI) introduced in 2015.”

Investing R 36 000 per annum and up to R500 000 over a lifetime* in a TFI vehicle ensures tax-free interest on growth and dividends with no capital gains tax as well. Importantly too, since TFI vehicles are not, like retirement funds, subject to Regulation 28, “TFIs can invest in higher earning high risk high return local and international equities and property funds with no legislative limits,” says Herselman.

The advantages of leveraging RA tax benefits in combination with the other tax benefits offered by TFI vehicles are illustrated in the following three scenarios.

Saving for retirement by combining a TFI with an RA VS using an RA alone

Let’s assume a 28-year-old investor is saving R 5000 a month for retirement, aiming to retire at 60. Let’s also assume his contributions increase 5% each year with inflation. At retirement the investor’s aim is to receive an after-tax income equivalent to R 20 000 a month in today’s value of money.

Scenario 1: The investor contributes R5000 a month in an RA only (with contributions adjusted annually for inflation) until age 60 when he retires.

Scenario 2: The investor contributes R5000 a month but split across an RA and a TFI, with R3000 going into a TFI, until it reaches the lifetime limit of R500 000, wherein those contributions will be redirected into an RA. Furthermore, the TFI contributions will be invested an offshore unit trust in order to gain exposure in the high-risk high return offshore market.

The balance of R2000 is then invested in an RA (with contributions adjusted annually for inflation) until age 60 when he retires.

The scenarios also assume that that:

• The investor receives a return of inflation plus 4-5% (9.5% per year) after all costs on the RA and inflation plus 5-7% (11% per year)

• The investor does not re-invest his SARS tax deduction since, in practice, most people spend this money although they should re-invest it to grow their retirement nest egg even more,

• The investor converts his savings into a Living Annuity at retirement, with the initial 2.5% withdrawn and the balance funded from the TFI.

• Where there is no TFI the 2.5% is automatically increased until the 17.5% legislative limit is reached on the proposed Living Annuity investment.

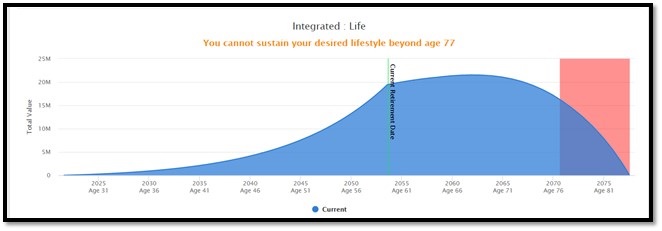

The outcome of Scenario 1 (investing through an RA only)

In this scenario the investor can sustain his desired R20 000 a month income after-tax in today’s money until he is 77 years old when he reaches the 17.5% legislative income limit on her retirement funds.

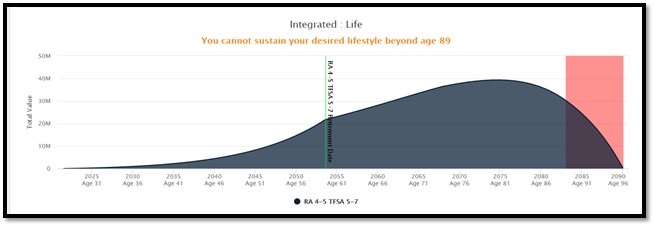

The outcome of Scenario 2 (combining an RA with a TIF)

In this scenario, the investor can sustain his desired income of R20 000 a month after-tax in today’s money until he is 89 years old when his TFI is depleted, and he reaches the 17.5% legislative threshold on retirement funds.

“Combining an RA with a TFI vehicle allows the investor to increase the lifetime of his desired income by an additional 12 years compared to when he uses an RA only,” says Herselman.

These results don’t only illustrate the potential benefits of the TFI when used in tandem with an RA, “but also show how investors can earn a higher return over the long-term as a result of unlimited exposure to the riskier local and offshore asset classes such as equities and property,” adds Herselman.

The tax refund of up to 27.5% of total annual income capped at R350 000 invested in an RA and the TFI provide South Africans with a genuine shot at improving the poor savings culture in the country, with the combination of the two providing “a realistic chance of achieving a sustainable retirement over the course of a normal working life at affordable levels,” concludes Herselman.

* Exceeding these limits will lead to a 40% tax penalty applied on excess contributions.