Close to retirement but haven’t saved enough? Here are some steps you can take to secure your retirement

You’ve reached retirement and, according to the Net Replacement Ratio (NRR), you haven’t saved enough. What now? Hildegard Wilson, Product Solutions Actuary at Momentum Investment shares some advice.

A few years ago, the National Treasury stated that only 6% of South Africans can replace their full income after retirement. This sentiment was re-iterated in the National Treasury’s release in December 2021 on the suggested two-pot retirement savings paper. Despite the current interventions such as financial education, tax savings vehicles and retirement reform, South Africa’s retirement saving situation has not changed meaningfully. With such a bleak picture, some may think it is too late to change their future if they are close to retirement age, but there are always steps that can be taken.

Step 1: Consider your ‘Hierarchy of Financial Needs’

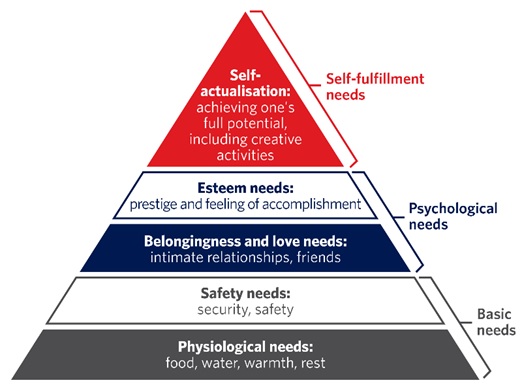

In the 1940s, psychologist Abraham Maslow gave us a glimpse into the human psyche, explaining his theory of human motivation. He defined a hierarchy of needs as follows:

Source: Maslow's Hierarchy of Needs (www.simplypsychology.org)

As Maslow explained, people should first fill their basic needs (psychological needs such as food, water, warmth, rest and security needs, such as security and safety) before they fill their ‘need’ for luxury items or experiences, such as an expensive outfit, an evening out or a dream holiday. This hierarchy of needs can help us not only understand ourselves, but also how people save. Financial savings, for example, only become a ‘need’ after your more basic needs such as food, security and clothing have been covered.

When planning for your retirement, it’s important to first budget for your ‘basic’ needs before moving further up the hierarchy triangle. In this way, if you are short of money in your retirement, you can prioritise the money you do have, to ensure that your essential needs are met. However, in South Africa the prices of many basic goods have increased disproportionately when compared to salaries.

Step 2: Keep your budget up to date with your personal inflation as opposed to consumer price index (CPI) inflation

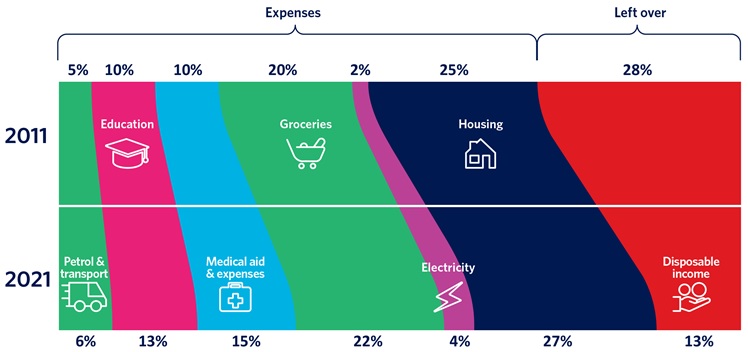

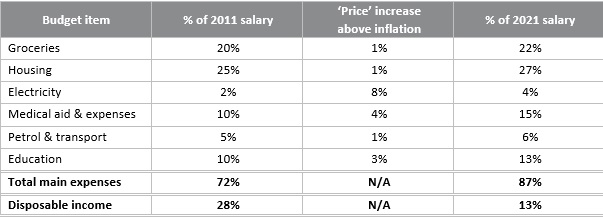

Let’s look at a case study. In this case study, we assume salaries have kept up with inflation. If a person’s expenses grew by more than inflation, a higher proportion of salary will have to be allocated to expenses. For example, if you spent 2% on electricity in 2011 and your salary increased by inflation, by 2021 the electricity bill will make up 4% of your total salary. The reason is electricity prices increased by 8% more than inflation each year over the last 10 years. This will clearly have an impact on how much ‘free’ cash you have available for the rest of the needs in your hierarchy.

The graph below took a list of possible basic expenses and allocated a % of salary that might have been spent on each item in 2011. We allocated a rate at which each item increases based on industry averages. In reality this rate will differ from person to person, for example a family shopping at high-end shops will have experienced different price increases when compared to that of a budget shopper.

Below is an example of the impact could look like:

Source: Momentum Investments

Looking at the above scenario, we see that disposable income has more than halved in the past 10 years. With less disposable income to put towards non-urgent needs, this has put significant pressure on people trying to save for retirement. Retirement savings should be even more deliberate and planned. The pressure of saving for retirement can be alleviated by keeping an up to date budget to make sure there’s enough money left to contribute towards retirement.

Step 3: Take control of your retirement NOW – no matter your age!

Given the pressures making life difficult and more expensive for consumers, there are still a few options available for those who haven’t managed to save enough to retire comfortably by the time their retirement age comes around:

• Additional contributions: Although making additional contributions to your retirement savings is not always possible, there is another option. When retiring, many people opt to take as much of their hard-earned retirement savings in cash as possible. However, the truth is, you’re more likely to burn through cash if you have free access to it. If you have another source of income in your early retirement years (e.g. a part-time job, consulting, rental income or a stipend from your family), it would be wise to invest a portion (or all, preferably) of your saved retirement funds, so that you can continue to grow your retirement savings during your retirement, and only access the savings when you no longer have this additional source of income. Compound interest can create significant wealth. For example, if a modest investment return of 8% per year can be achieved and interest is re-invested, your investment will double in just nine years. If invested at 12% per year with interest re-invested, your investment will double in just over six years.

• Delay retirement or partial retirement: The current retirement age of 65 was set in the late 1800s and aligned closely to the average life expectancy of people in that era. More than 100 years later, is this age still appropriate, given that many people seem to live longer than previous generations? Each person’s retirement date should be as personal as any other financial decision. Consider whether it is possible to start a second career, or to consult on a part-time basis? If retirement can be postponed from age 65 to 70, more than a 10% increase in income can be achieved from a life annuity.

• Lowering income levels over time: Most people can’t absorb an immediate drop in income after retirement, and understandably so. However, with coaching, most people are able to lower their standard of living over time, in much the same way people tend to increase their standard of living when they get salary increases. To do this, people would need to gradually reduce their drawdown level to a sustainable level by slowly cutting back over time. This is a risky option as the future retiree will be exposed to risk such as sequencing risk. This is where a large income amount is withdrawn while markets and the retirement investment are low. In this scenario, a proportionately higher percentage is drawn from the retirement fund during market downturn compared to when investment markets are high.

With a little innovative thinking, there is hope for those facing these financial challenges.