Attitudes towards retirement fund risk not affected by income or age

Craig Aitchison, General Manager of Corporate Customer Solutions at Old Mutual Corporate.

While conventional wisdom would suggest that people of varying ages and incomes would have significantly varying attitudes towards retirement fund risks, a new study by Old Mutual Corporate has found that there is in fact very little difference across these demographics.

The Old Mutual Smoothed Bonus Customer Monitor surveyed more than 1 000 South Africans older than 18 who are currently contributing to a pension, provident or preservation fund to understand members’ risk attitudes and retirement income return preferences, as well as the underlying reasons for these preferences.

Craig Aitchison, General Manager of Corporate Customer Solutions at Old Mutual Corporate, says that there was no significant bias towards risk aversion by age and income levels in the group of fund members surveyed. There was a similar level of concern among members, across all age groups and income levels, about a loss in asset values.

The report revealed that most members are highly loss-averse, with 80% of respondents indicating that they would become very concerned if they experienced even a small loss of 5% of their retirement savings in a year.

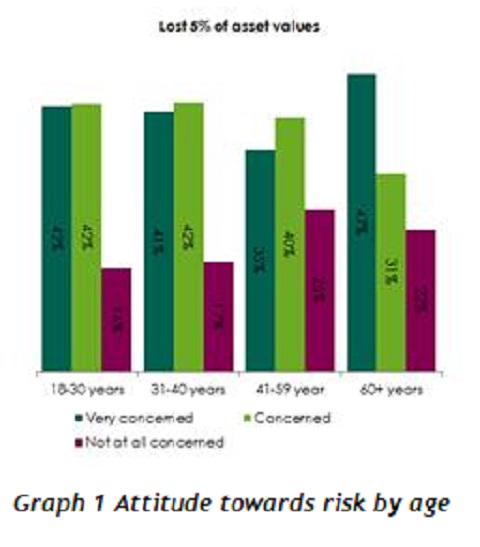

In terms of the attitude towards risk by age group, more than 80% of people in the age group 18-30 years and the age group 31-40 years expressed a concern for a 5% loss, while 75% of the age group 41-59 years and 78% of the age group 60+ expressed concern. The only drastic difference in response was in the age group 60+ with nearly half (47%) very concerned about a 5% loss of asset values.

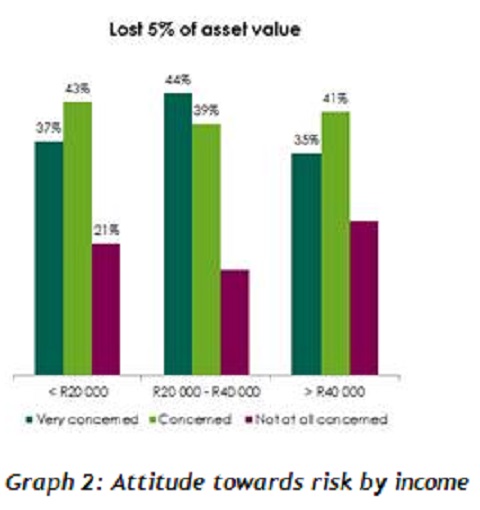

The attitude towards risk, by income groups, was also surprisingly evenly split. 80% of respondents earning less than R20 000 per month are either concerned or very concerned about a 5% loss in asset value, while 83% of respondents earning between R20 000 and R40 000, and 76% earning more than R40 000, express the same sentiment.

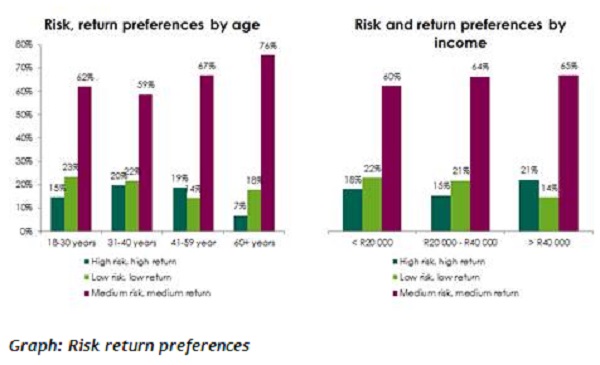

However, despite the majority of members being very risk-averse, the findings reveal that they are still attracted to returns above the low-risk and safe option. “There is a significant overlap between downside aversion and a need for growth exposure. 63% of respondents stated they wanted a medium level of investment risk and medium investment return as their risk/return preference, and 17% wanted a high-risk/high-return preference.”

Aitchison adds that once again a medium-risk/medium-return preference was mirrored across all age and income groups.

Aitchison says that respondents’ preference for a medium risk and return retirement investment strategy matches the value proposition of a smoothed bonus fund, or an absolute return portfolio.

“A smoothed bonus fund seeks to provide access to growth asset classes, while reducing investment return volatility. These products trim the extremes from the peaks and troughs of the market, and give the investor who is risk averse some level of comfort in investing in assets that can give them higher real returns in the long run.”

Respondents were asked about their attitudes towards smoothed bonus, and 56% of members understood the basic concept of smoothing of returns after being presented with an example. If offered the opportunity to invest in another retirement fund, 50% of members were likely to invest in smoothed bonus. “The reasons attributed to this decision were: the fund seems to have high growth potential (27%), it is a safe fund option (20%), and it suits my needs and is a good product (13%).

“While the members in the report have a strong stance on the returns they seek and the risk they are prepared to take to obtain this, the majority of members (80%) surveyed acknowledged not being very knowledgeable about their retirement fund savings. Their attitudes to smoothed bonus therefore suggest that with some level of financial education, members can have a high level of appreciation of how these funds work, and how they can impact their retirement savings,” concludes Aitchison.