Asymmetric returns yield greater upside

Andrew Rumbelow, Institutional Segment Head at Sanlam Investments.

In volatile markets, capture most of the upside, less of the downside.

Retirement fund trustees have to meet challenging goals— above all, achieve the highest possible rate of return for their members while limiting downside risk and volatility of returns. Yet in the current climate of increased volatility and lowered return expectations, reaching that objective has become increasingly difficult, says Andrew Rumbelow, Institutional Segment Head at Sanlam Investments.

So how can institutional investors meet the return objectives of their members without exposing them to substantial risk of short-term capital losses?

Many trustees have now begun to accept that they must be willing to fundamentally re-examine their investment strategies and investigate more tactical ways to achieve their investment goals. We anticipate that a key trend going forward will be a focus on investment strategies that generate a more asymmetric return payoff profile, i.e., strategies that maximise upside potential while capping downside risks in volatile markets. The key to these and to achieving sustainable positive returns over time is a dynamic risk-management process that limits the probability of large investment portfolio losses.

This article helps explain how trustees can leverage these strategies to provide members with a smoother journey toward achieving their goals.

What are asymmetric returns?

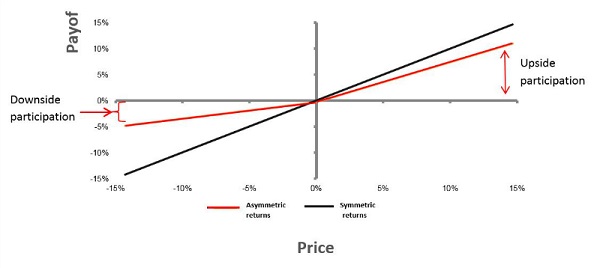

An asymmetric return profile is, at its most simplistic level, higher and more positive returns, lower and fewer negative returns – achieved through active risk management. An asymmetric return is a return profile that is actively managed to meet the end investors’ risk preferences more efficiently. Besides reducing volatility in returns, asymmetric returns are designed to preserve capital and offer downside protection, illustrated below:

A typical asymmetric return profile illustrates that participation in the upside is far greater (roughly ?) than participation in the downside (only ?):

Source: Sanlam Investments, 2016

Asymmetric returns are also extremely useful from a behavioural finance point of view. They limit the likelihood of irrational investor behaviour by creating a smoother return experience. Here we make the assumption that investors prefer asymmetric returns over symmetric returns, drawing on behavioural theorists Kahneman and Tvesky (1979), who describe the relative psychological experience of gains versus losses, called ‘loss aversion’. Accordingly, investors feel the pain of loss twice as much as the joy of gains, triggering emotional reactions (like fear) which may lead to poor investor decisions. Absolute return strategies are key in that they limit the likelihood of these behaviours.

Defining risk in absolute (rather than relative) terms

“The essence of investment management is the management of risks, not the management of returns.” Benjamin Graham"

Risk management in an absolute return context is driven by profit and loss, rather than market benchmarks. This means that risk is defined against an absolute yardstick, like capital depreciation, as the return objective is to generate a positive compounding of capital while the risk-neutral position is cash (Alexander Ineichen, 2006). However, in a relative return context (like benchmarking and indexing), risk is defined, perceived and managed as ‘tracking risk’. In this context, the investor is exposed to both upward and downward swings in the asset class.

It seems likely that the future of active asset management will rely more on designing investment strategies where the risk/reward relationship is asymmetric and less about beating a benchmark. It is not surprising, therefore, that internationally hedge funds have started to seriously compete with traditional asset managers in recent years —especially for institutional assets.

How absolute return strategies yield asymmetric return profiles

Absolute return strategies are designed to provide investors with an asymmetric return profile. The essence of the absolute return investment strategy is to achieve inflation-beating returns at reduced levels of volatility. Tactical and dynamic asset allocation is combined with explicit downside protection, using derivatives and other risk protection strategies to achieve the required real return target. A high priority is given to minimising capital losses, in sync with an asymmetric investment strategy.

How we manage downside risk through absolute returns

At Sanlam Investments, we look at relative valuations across all asset classes to support our dynamic asset allocation decisions. Our bottom-up driven equity valuations in particular are key to determining the magnitude and timing of the protective structures we put in place. To ensure maximum certainty in outcomes, we use these fundamental equity valuations in combination with derivative overlays to put explicit downside protection in place. This combination of derivatives with a fundamental valuation underpin acts as a protective structure (or hedge) against equity market falls, aiming to achieve the highest possible rate of return (per unit of risk taken), while minimising the risk of capital losses.

We operate dynamically across all asset classes, both local and offshore, including equities, nominal bonds, inflation-linked bonds, cash, listed property and derivatives, to adapt to relative market valuations.