The impact fees have on your living annuity returns

Tracy Jensen, Product Architect at 10X Investments.

For most people, cost is a primary consideration in almost every purchase decision. Except, it seems, when it comes to critical financial decisions, such as buying a savings or investment product. Many South African retirement investors therefore also overlook the fees on their living annuity, or rather, the impact these fees will have on the longevity of their savings.

A living annuity is an investment product that provides you with an income from your retirement savings. Unlike a guaranteed annuity, it gives you the flexibility to choose your income each year (subject to regulatory limits) and how your money is invested. The downside is that you bear the risk of outliving your savings, or that your annual income does not keep pace with inflation. Your annual draw-down rate – the percentage of your investment value that you draw as income – plays a big part in how long your money will last.

“All investors who buy a living annuity run the risk of outliving their savings. In this context, one of the three most critical elements they must consider is the fees they will be paying,” says Tracy Jensen, Product Architect at 10X Investments.

Few investors appreciate that their capital is reduced both by their draw-down and by the fees they pay. “To assess the full impact on their capital, investors must add their fee rate and their draw-down rate - both expressed as a percentage of capital. The higher the fees, the sooner the money will run out. Or alternatively, the higher the fees, the lower your draw-down rate will need to be, to sustain a given level of income,” says Jensen.

The average fee on a living annuity is high, at around 2.85% per annum (including VAT) of the investment balance. This comprises an investment management fee of approximately 1.5%, an administration or platform fee of around 0.25%, advice at 0.75% and VAT of 0.35%.

The cost is high because most living annuity providers follow an expensive active management approach, they offer unnecessary ‘bells and whistles’ that add to administration costs, and require the involvement of an advisor.

Fortunately for investors however, far more cost effective options have become available in recent times. “For example, 10X’s maximum fee on living annuities is 0.86% per annum, which decreases further above R5m. Our fees are low because we use index rather than active investing, and we offer a simple solution, with the use of an advisor optional. ”

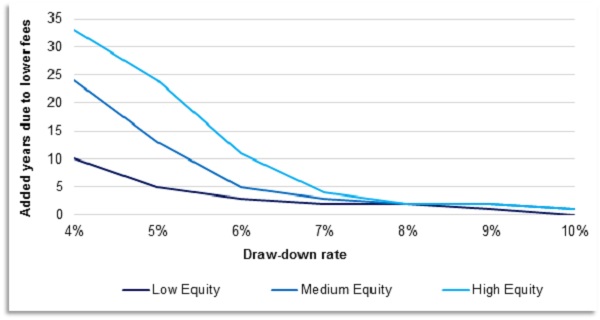

The huge impact that fees have on the longevity of your savings can be seen in the example below. It shows the added years of income that you stand to receive, assuming you pay the low 10X fee of 0.86% versus the industry average fee of 2.85%. The impact depends on the type of portfolio you choose (i.e. either high, medium or low equity).

“A high draw-down rates (above 8%), the fee impact is quite muted, as your savings deplete so quickly; however, if you intend to make your savings last, and draw down conservatively (between 4% - 6% pa), the fee impact is highly significant. For example, drawing down at 5% from a high equity portfolio can sustain your income 25 more years, if you pay the lower fees; and even for a low equity portfolio, you stand to gain an added five years of income,” says Jensen.

Investors may have little bargaining power to negotiate the fees charged on their living annuity product, but they do have the choice to select a low cost provider, says Jensen. “When selecting a provider, make sure you know all the applicable fees before making your selection. Many companies are masters at obscuring their fee structure. But don’t just consider fees. Also assess the provider in terms of the investment portfolios available and the services provided. For example, how easy is it to access information, how strong are the planning tools, how transparent is the reporting, how responsive is the provider?”

“Always take into account the fees you pay. Research from Morningstar demonstrates that low fund fees are better at predicting winning funds than start ratings.. If you invest in a living annuity with high fees you will most probably not get the optimal pay-back on your retirement savings.” concludes Jensen.

Comments

My contact number is 0835646641.

Kind Regards

Dave Renke Report Abuse