Risk assessments: throw out generic assumptions

01 November 2013 | Magazine Archives FAnews & FAnuus | Short Term | Marcel Wood, Etana Insurance

Providing adequate risk reductions in developing and mature economies, ideally needs protection linked to a risk based approach – rather than generic assumptions – measured against solid criteria of best practises and tweaked to local conditions.

Are we there in South Africa? That is the topic of this discussion. For the risk management process to be adequate and fair, data used for risk assessment needs to be based on reliable criteria which can be substantiated.

All insurance companies carry out risk assessments on insured parties to establish the level of their exposure to risk. This involves some form of quantification of the pure risk loss scenarios, where only losses can occur, and not the business risks, where gains as well as losses may be the outcome.

There are generally three methods of achieving this:

1. qualitative risk assessment,

2. quantified risk assessment (QRA), and

3. semi-quantitative risk assessment.

Qualitative risk assessment: this process has very little, if any, solid criteria against which to base, substantiate or justify a conclusion that a particular risk is in fact low, medium or high.

Quantified risk assessment (QRA): this is really reserved for use where there is a definite and expected loss of life foreseen. It involves complex calculations and is a protracted process.

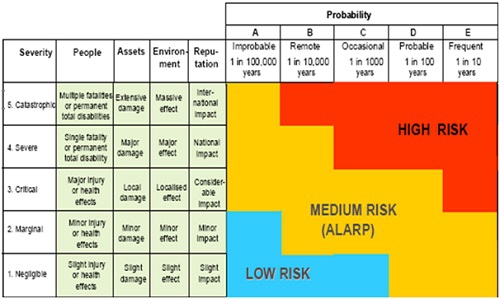

Semi-quantitative method: this is the most suitable method of assessing pure risk and is clearly laid out in the graphic below. The data used includes all, or some of, either empirical, historical or scientific data which can be substantiated. Another advantage is it is not a complex process and provides a base against which risk can be easily and accurately assessed. (See graph below)

Semi-quantitative method revealed

Mistakes insurers make

One of the mistakes we, as insurers, make is allowing people outside our company to judge what is a low, medium or high risk. For example: a client says they have been in business for an impressive number of years and have never experienced a loss. This is considered ‘evidence’ of low or no risk.

This assumption is perpetuated by a client’s excellent claims history, implying that claims histories qualify as reliable proof of low risk levels. The reliance on approved rational designs is also assumed to mean that all risks present are sufficiently reduced.

However, in reality, these are chiefly life safety risks and have little to do with material losses. Another common costly mistake is relying on compliance only to the National Building Regulations which does not adequately address asset and property protection.

Inadequate risk assessments will be the order of the day until insurance risk assessment teams cease to carry out audits against only the criteria of the National Building Regulations. Obviously, this means asset and property risk mitigation will not be equal to the potential loss risk levels present.

Individuality a must

Every insurance company must rely upon their own expertise and criteria to assess and quantify loss scenarios evident within the premises they insure. The recommended risk based approach allows each and every risk to be individually assessed against real asset and property loss scenarios. For example, even two apparently identical plastic operations may be different risk-wise.

The road onward and upward

Let us all commit to using only appropriately qualified risk assessors. Invest in training them so they keep pace with changing technology as well as the risk landscape. Also make sure that they are capable of expertly reviewing fire designs (rational designs).Use and refer to Best Practise for asset and property protection. (Examples include: Best’s Underwriting Guidelines, FM Global Standards and NFPA Standards.) Adapt these to local conditions and remember the word ‘yet’ whilst steering clear of accepting lack of claims as a basis for quantifying risk. A poorly protected risk remains inadequately protected, whether it has endured a loss, ‘yet’ or not.