Gap Cover - the long and winding road

Your clients have a constitutional right to insure themselves against any financial risk, but they are often unaware of the subtle differences between health insurance products and medical schemes. There is a belief with some clients that a health insurance policy offers the same protection as a medical scheme for major medical events, when in fact the protection is only partial and conditional.

There is also no regulation in South Africa which governs the tariffs charged to patients by health professionals, so private practitioners can determine their own fees. This practice results in a significant gap, reaching as much as 450% to 500% between what is charged by private specialist doctors and what is reimbursed by medical schemes.

It is this uncertainty about what medical bills may arise in the future for a medical scheme member that has resulted in strong public support for health insurance cover, specifically for Hospital Cash Plans and Gap Cover products.

Clarifying a confusing topic

A health insurance policy is a contract sold by an insurer to an individual in terms of the Long-term or Short-term Insurance Act. It is subject to regulatory oversight by the Financial Services Board (FSB). The policy promises to pay for certain stated or fixed benefits when the individual is ill or injured. The individual pays a certain premium which is directly related to his or her age, health status or income. Specific types of exclusions may also be built into a policy, such as the maximum age at entry which can have the effect of excluding older people, in particular retirees.

Gap Cover is a specific type of short-term health insurance that covers the shortfall between the actual fees charged by health professionals and the medical scheme tariff, for procedures done in-hospital only.

Demarcation regulations

The demarcation regulations specify the types of health insurance policies that are accepted under the Short-term and Long-term Insurance Acts. The intention of the regulations is to create a clearer demarcation between health insurance and medical scheme business by ensuring that the design, marketing and sale of health insurance policies supports the principals of community rating, open enrolment and cross subsidisation (social solidarity) enshrined in the Medical Schemes Act, while at the same time serving the needs of individuals who require additional financial protection against high medical expenses.

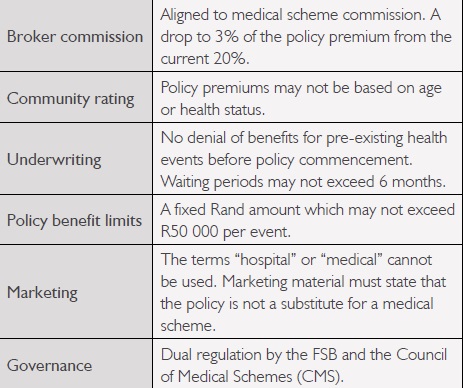

Proposed conditions for Gap Cover

The second draft demarcation regulations issued last year in April by National Treasury, propose the following conditions on health insurance policies, and in particular on Gap Cover products.

Public concerns and current position

National Treasury received over 400 submissions during the consultation process on demarcation, a number of which were from individual members of the public urging government to keep Gap Cover.

Some of the concerns raised in the submissions include:

• The constitutionality for the proposals and the grounds for placing restrictions on health insurance in the absence of low cost medical scheme alternatives.

• Proposed underwriting terms and conditions are inadequate to protect against anti-selective behaviour and will undermine the affordability and sustainability of these products.

The numerous and extensive public comments received have resulted in National Treasury and the Department of Health postponing the publication of the final Demarcation Regulations until the second quarter of 2015.