Ensuring sustainability through flawless claims management

01 August 2012 | Magazine Archives FAnews & FAnuus | Short Term | Servaas du Plessis, Censeo

The short term insurance landscape has changed significantly over the past 15 years. Improved scientific and risk-specific underwriting models, evolving distribution channels, new entrants with innovative products and loyalty programs have revolutionised the way we conduct business. What will the next decade bring?

There is no doubt the short term insurance landscape will continue to evolve as strict capital, regulatory and reporting requirements are introduced and legislated.

In a recent survey published by PwC it is evident that insurers will have to adapt to change by reconsidering both their product offering and the way in which they interact with clients. Every process from underwriting stage to claims processing stage will have to be put under the microscope. To stay ahead of the game insurers will have to embrace actuarial modelling, predictive analytics and segmentation of client risk. They will also have to pay close attention to client retention modelling and claims management.

Why claims management?

I have been involved in the industry over the past 15 years and have worked in both direct and broker distribution environments. I helped to establish the South African Insurance Crime Bureau and was involved, on an industry level, with the pro-active detection and prevention of both syndicated and opportunistic fraud perpetrated against short term underwriters. I believe that claims management, like client loyalty and retention, are among the most neglected areas in our industry.

Defining great insurance service

Most short term stakeholders believe that great service requires settling claims in full, as quickly as possible. The reality is that insurance would soon become unaffordable if all underwriters paid out for all eventualities. It is also fact – not unique to South Africa – that there are individuals, fortune hunters and organised criminal syndicates that submit fraudulent and dishonest claims. Underwriters have an obligation to protect the interests of their clients, shareholders and other interested stakeholders against such criminal attacks.

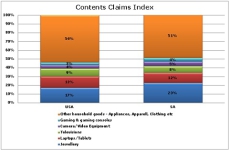

A better picture of the underwriting and claims management environment emerges when we compare the annual US CCI (Contents Claims Index) survey with claims processed for more than 40 underwriters and UMAs in South Africa. Other household items tops the CCI list in both the US and South Africa, though our rate is 3% lower than theirs. The second largest category – jewellery – accounts for 17% of householders claims spend in the US and 23% in South Africa.

Examining fraud trends

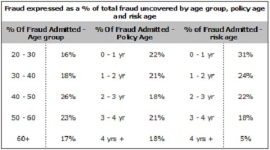

What can we learn by considering fraudulent and dishonest claims’ trends? Of the total number of admitted fraudulent claims (in the householders claims space) the majority of fraud was committed by individuals in the 40 to 50 age group, two to four years after policy inception and less than one year in risk age.

The trends are very similar in vehicle theft and hijacking claims processed over the period. Although the percentage of fraud committed on vehicle claims is lower, the average cost of such claims is substantially higher.

The value in claims management

Placing an emphasis on claims management goes beyond considering the risk of unnecessary claims leakage due to fraud. Provider costs, exchange rates and a handful of other factors also impact on pricing and profitability. Client retention is of critical importance – and seamless, fast and effective claims settlement is perhaps the most important consideration in client retention strategies.

Client interaction primarily takes place during sales and claims stages and there are several channels for this communication to take place. Most companies are centralising their claims processing through call centres, online reporting and/or claims management agencies. It is essential that insurers approach distribution, retention and claims as a fully integrated solution rather than in the segmented manner currently applied.

Working together

Internal/external specialisation, forensic services, expert analysts and custom-made solutions remain the most sensible approach to claims management. A closer collaboration between the different business units will enable client-specific solutions. Proper claims management is crucial to the sustainability of underwriters and re-insurance companies. Aseamless claims processing solution will have a definite and direct impact on an insurers’ ability to retain clients going forward.