Just how much risk is Mary's little lamb?

01 February 2013 | Magazine Archives FAnews & FAnuus | Risk Management | John Stebbing, Camargue

Most small to medium-sized businesses believe that risk management is the domain of large companies. Probable responses to risk management queries are often met by, “We’ll cross that bridge when we get to it”, or “we are too busy trying to survive to worry about that…” says John Stebbing, Underwriter at Camargue’s Liability Academy for Brokers (LAB).

The irony, however, is that most business failure can be attributed to not recognising and addressing risks. SMEs can and should use risk management as a means to improve their profits and odds of survival, and it need not break the bottom line: knowledge is power.

Evaluate it honestly

In an economy that desperately needs entrepreneurs to generate employment, it’s shocking to see how many businesses fail in their first few years.

So, why is it that we, like financial lemmings, charge helter-skelter to our doom? The answer lies in the fact that entrepreneurs and most of their managers are optimists.

If they weren’t, they would not risk their money in the first place. Although optimism is mandatory for success, it can also hide a serious flaw that often leads to disaster, since most optimists find it hard to be completely honest about recognising and evaluating the risks their businesses face.

The basic calculation technique

Although risk management can quickly become very complex, even its simplest techniques can tilt the odds in the entrepreneur’s favour.

A practical process that can be useful in risk assessment includes a basic calculation technique:

1. Make a list of the top 20 things that can go wrong,

2. Give each risk a frequency score from one to five depending on how likely it is to occur. A score of five would mean a loss is very likely,

3. Score each risk according to loss severity. Award a score between one and 10, where a 10 represents disaster,

4. Now multiply each risk’s frequency score by its severity score and arrange the list with the highest combined scores at the top.

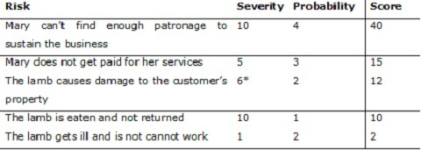

For example: Mary has a little lamb, which she hires out to children’s parties. Table 1.1 illustrates how this technique is applied to a sample of Mary’s business risks.

*In some cases the severity of the loss can vary dramatically. Use the most likely scenario, but with a pessimistic bias.

When performing this analysis, a useful tip to remember is that people tend to underestimate well-known events and overestimate rare events. For example, employers would tend to underestimate the risk of employees taking them to the CCMA, but overestimate the risk of employee injury in the work place.

Don’t ignore the risks

During this risk analysis process there are going to be items that are easier swept under the carpet than confronted. There will also be questions that have not been satisfactorily answered. There is a temptation to ignore these risks in the hope that they will somehow "sort themselves out”. My experience has been that they will indeed sort themselves out – but not in an acceptable way that serves the business agenda.

Solutions needed

In conclusion, what SMEs really need is a comprehensive and robust risk management solution that preferably doesn’t cost anything. There are solutions out there and brokers need to grab opportunities with both hands.