Retirement fund contributions a tax changing picture

Government confirmed its intent to improve retirement savings in South Africa with one of these being tax incentives for contributions towards retirement.

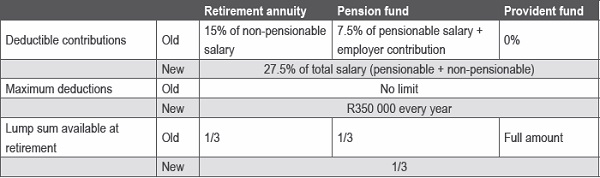

There are currently three ways of making use of tax incentives for employees, namely provident funds, pension funds and retirement annuities. Tax regulations applied to each method are, at present, significantly different. As a result, government has recognised the need to simplify and align incentive structures as well as limit excessive use of tax breaks.

There are currently three ways of making use of tax incentives for employees, namely provident funds, pension funds and retirement annuities. Tax regulations applied to each method are, at present, significantly different. As a result, government has recognised the need to simplify and align incentive structures as well as limit excessive use of tax breaks. The table below shows some of the key changes:

Provident and pension funds and retirement annuities will effectively have the same rules in future. Funds built up in provident funds up to March 2015 will fall under the old rules.

Those contributing to retirement annuities, will have to claim back deductions from the South African Revenue Service (SARS) at the end of each tax year, while deductions to provident and pension funds will be included in the calculation of take-home pay every month.

Offering further incentives

Government announced that the lump sum amount that could be withdrawn tax free at retirement, increased to R500 000 from 1 March. This offers further incentive for individuals to save through retirement vehicles.

High level calculations show that a person who used the maximum deductions in the past through retirement annuities, combined with employer pension funds, would enjoy similar deductions under the new structures. However, higher earners might enjoy lower deductions due to the R350 000 maximum deductions per annum.

The maximum will only apply to people earning more than R1.27 million per annum where the contribution is 27.5% of their total earnings. Typically, total contributions from the employee and the employer are currently below 20% of pensionable salary in employer schemes. Where the contribution is 20%, the annual maximum of R350 000 will only apply to those earning more than R1.9 million, assuming 90% of the salary is pensionable.

Incentives for high income earners

Where high earners do contribute more than the yearly maximum, there are still reasons to invest in retirement savings vehicles. The amounts contributed above the maximum will not be taxed after retirement, whether taken as a lump sum or income. In addition, returns will still be tax free, which is a major benefit compared to other avenues of saving.

On the other hand, lower income earners will be able to contribute more than 27.5% as long as the amount contributed is less than R20 000. This will encourage lower income earners to contribute more towards retirement.

Deduction amounts that are not used in a given year will be recorded separately and this will, most likely, fall in the ambit of SARS. This amount could be used for deductions in future years.

Employer sponsored schemes, such as umbrella funds, typically benefit from group structures

and could therefore offer more cost efficient products than many retail products.

Currently, contributions towards income protection type benefits are tax deductible, while income received once claimed, is taxed. From March 2015, contributions will not be tax deductible anymore, but income received through claims will be tax free. This means that employers will have to reconsider the cover levels to ensure the income in the event of a claim, which is now tax free, is appropriate compared to the income levels before claiming, which was previously taxed.