Living longer...

Clients battle to get their heads around the future capital amount they need to provide income from, especially when provision for inflation after retirement is included in the calculations.

With advances in technology and medicine, as well as a shift towards a healthier lifestyle, people are living longer. Although the benefits are obvious, the other question that arises is whether your clients will have enough provision for their retirement years?

A critical component to consider when estimating the required retirement provision is the cost of healthcare. We cannot escape the fact that more people will live beyond the age of 90, and will need access to quality healthcare throughout their lives.

This picture is alarming if you consider a client who retires early at the age of 55. Assuming your client started working at the age of 25, it means that he would have worked and saved for only 30 years to support the last 35 years of his life.

Retirement costs

The scenario for someone who saves for 30 years to support about 35 years in retirement gets even more bleak when one considers the high cost of living in the retirement phase.

As people age, their health status deteriorates. In South Africa, medical schemes remain the most utilised funding of private healthcare (in the absence of national health insurance). However, this funding comes at a cost, with the average medical scheme contribution being around R1 900 per month for an individual in 2012/13, regardless of the age.

The cost of healthcare is also expected to increase by at least 3% above inflation. Over time the cost of healthcare will take up a significant portion of the retirement income, given that pension increase in line with inflation (at most).

Have you considered how much capital is required to cover the costs of healthcare? If your client retires this year, and he is in retirement for the next 35 years, the present value of the total healthcare cost is about R1.2 million. This is the cost your client has to bear in mind going into retirement, taking into consideration that longevity can increase this figure.

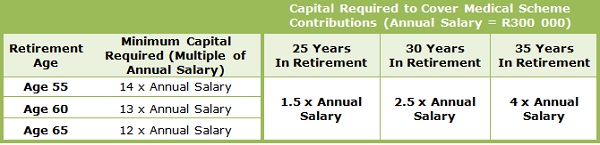

Capital required for retirement

The table below shows the minimum amount (expressed as multiples of annual salary) needed for a male who wants a retirement income that increases by 5% a year. This table also illustrates the capital he requires to cover healthcare costs (depending on how long he might be in retirement).

The high cost of healthcare increases the minimum capital required for retirement by between 5% and 15%, depending on how long you will be in retirement phase.

Other factors to take out are:

• Early retirement is costly.

- The younger your retirement age, the higher the capital you will need

- The longer you will be in retirement, the higher the capital you will require to cover healthcare costs.

• The cost of quality healthcare is independent of your income.

• The average contribution to medical schemes is used as an indicator for the cost of healthcare. This could be the minimum healthcare costs, as pensioners may expect to pay for some costs out-of-pocket.

• We assumed a pensionable salary of R25 000 a month just before retirement, and a replacement ratio of 75% of the income.