Combining the best of two worlds to mitigate longevity risks

When facing the decision of which retirement income vehicle to choose, a retiree is faced with acknowledging the risks inherent in each option.

The primary risks are investment, longevity, inflation and behavioural risk. In the context of a risk spectrum, a guaranteed annuity insures a retiree against each of these risks while the living, linked annuity option allows the retiree to retain these risks for his/her own account. This all or nothing approach to risk transfer is flawed and needs to be rectified to allow the partial transfer of each of the four risks.

Budget categories

Within their budget the typical retiree will have “must-have” expenses as well as luxuries. Budget expenses for a retiree can be divided into four main categories:

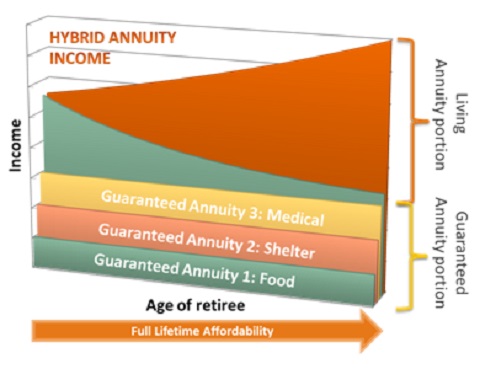

- Food

- Shelter

- Medical

- Other

Introducing hybrid annuities

The income generated by retirement funding vehicles needs to ensure first and foremost that the “must-have” expenses are covered. This translates to a risk free solution being required to cover this portion of the retiree’s budget.

If a retiree were to purchase guaranteed annuities to cover each “must-have” portion of each expense category, the retiree would be protected on a monthly and annual basis against not meeting the minimum income requirement.

The key risks will therefore be transferred. This sustainability is crucial to ensure that financial protection is provided in the short, medium and long term.

This does not mean that a retiree should be purely locked into a guaranteed annuity to cover “must-have” expenses, but should have the option, via a guaranteed annuity, to protect any per expense means that retirees can select escalations in line with varying inflation rates for different expense categories.

The remaining capital not invested in guaranteed annuities can thereafter be invested more actively within a living annuity structure, to seek outperformance via selected investment funds. If the investment outperforms, then the retiree is able to afford a greater number of luxuries. If the investment underperforms, then the retiree will need to cut down on luxuries. The living annuity portion is therefore designed to allow a retiree to invest for greater returns without worrying about the short and long term investment volatility effect on “must-have” expense affordability.

The hybrid annuity therefore allows a retiree to move along the aforementioned income risk spectrum ensuring that each risk is protected to the degree required or selected by the retiree.

At the moment, the only way a retiree can split compulsory capital between a living and guaranteed annuity is if one of the products produces an income in excess of R150 000 per annum. This places split solution out of reach of retirees.

Moving forward

The solution available is to allow each guaranteed annuity to be purchased as a portfolio within a living annuity. Each guaranteed annuity therefore becomes an income generating asset with a nominal value. Retirees are additionally able to continuously add assets allocated to the guaranteed annuity portfolios.

The debate in South Africa regarding the use of a living annuity or a guaranteed annuity needs to be refined to rather ask what the balance should be between the two products.

Each has a specific role to play in the provision of sustainable income provision for retirees. The key is to acknowledge these roles and ensure the selected products tie in with the expectations and requirements of retirees.