The dark side of regulation

People’s life expectancy is increasing, with a corresponding increase in spending on medical and health-related services. This makes the provision for retirement important. People’s pension funds are often the largest portion of their financial provision for retirement and it is therefore paramount that retirement funds grow at a consistent rate in order to ensure that individuals have sufficient savings at retirement.

The South African paradox

It was recently highlighted that individuals in South Africa do not save adequately for their retirement with only around 6% of South Africans being able to maintain their current lifestyles at retirement.

Legislation currently allows investors the option to receive the full amount of savings of their provident fund upon resignation or upon retirement. However, to encourage retirement savings, government attempted to impose a compulsory partial annuitisation retirement savings of a pension or provident fund upon individuals who resign or change employment. Capital invested in preservation provident funds is limited to the initial amount, after which only the investment returns may be reinvested.

Regulation 28 of the South African Pension Funds Act prescribes the maximum allowed investments in different asset classes. In various publications, authors present additional information on the amendments to Regulation 28, informing investors that Regulation 28 does not only prescribe a maximum foreign asset exposure of 25%, but also that the look-through principle was applied, removing the possibility of circumventing Regulation 28.

Maximum benefits

Other authors found that pension funds in South Africa would only enjoy an absolute benefit in their returns if the funds invested the maximum of their allowance in foreign assets.

It can be argued that, due to drifting, it is possible that funds breach the 25% foreign asset investment limit due to different rates of return of the foreign and domestic portfolios.

An unintended consequence of Regulation 28 might be that portfolios have to be restructured if a component in a preservation provident fund significantly outperforms the rest of the components and the asset class limit set by Regulation 28 is breached.

The change in the value of a component, such as the portfolio’s foreign component, could be due to an exogenous factor, such as a weakening in the exchange rate in the local currency and, due to the translation effect, the 25% foreign investment limit might be breached.

The scenario

This study investigated to which extent the optimisation of investment returns may be hampered by the limits set by Regulation 28 in the case of preservation provident funds where the investor follows a passive investment strategy.

As a result of drifting, Regulation 28 limits could potentially reduce the growth of an investment portfolio as the regulation requires divestment from foreign equities within a year after the limits had been breached.

Important providers

For a large number of people, retirement savings are the most important source of income in their old age, and for this reason, regulation aims to protect the funds of individuals but limits the potential for adverse returns due to poor investment decisions.

The regulations may therefore have unintended consequences. Regulators often prescribe limits when dealing with pension funds that would be used by individuals upon retirement.

The effect of this type of regulation is however different amongst developed and emerging economies. From the perspective of an emerging market economy, the two motivations for regulatory maximums in pension fund asset allocation are:

- Ensuring a diversified portfolio, limiting exposure to risky assets; and

- Ensuring that retirees do not become dependent on government grants as a result of poorly managed retirement investment funds.

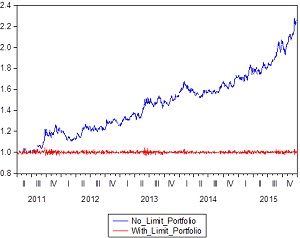

A fictitious R1 portfolio was used to illustrate the unintended consequences that the regulation could have on pension fund returns when an investor makes use of a preservation provident fund. These fictitious portfolios were mutually exclusive and fluctuated as the translation effect of the dollar affected the portfolio.

One portfolio did not have any regulatory restrictions – no limit portfolio – while the other was subject to the current 25% maximum exposure to foreign asset investments (with limit portfolio).

To describe the unintended consequences, the data is presented graphically with a line chart. Descriptive statistics were calculated, and a Granger causality test was conducted.

Figure 1: Performance comparison of the no limit portfolio with the with limit portfolio

Interesting results

The results showed that, due to exchange rate fluctuations, a preservation provident fund could breach the allowed foreign asset allocation, requiring rebalancing and ending up in lower returns due to the downward adjustment that had to be made due to a deteriorating exchange rate.

When the exchange rate became beneficial again for the fund, a rebalanced portfolio already reduced the funds available for growth.

Descriptive statistics were used to illustrate the difference in returns if it had been that there were no regulatory constraints on a portfolio. This pertains to investment in foreign dollar-denominated assets compared to a portfolio that had to maintain the current 25% maximum limits as prescribed in the South African regulations.

Over a four-year period, the growth of the R1 due to exchange rate fluctuations, keeping all other factors unchanged, would have been approximately 130%.

This article emphasised the importance of achieving adequate returns on the investment of a pension fund. In order to protect the funds of investors, regulators engage in prescribing maximum asset allocations in different asset classes in order to ensure a properly diversified portfolio.

This article indicated that regulators could consider relaxing the maximum exposure emerging market economies may invest in developed economies as this might result in increased pension fund returns. Future research should evaluate up to what percentage an investors should be able to invest in foreign developed economies.