The racehorse and the falcon

The insurance community is currently grappling with a particular challenge when it tries to solve problems, which is that different people are using different words for the same things and the same words for different things. This can be encapsulated in the parable of the racehorse and the falcon.

Assume you are the chairman of the prestigious, well-established horseracing club. The whose-who of society attends the annual race.

One day, after another successful race, a rather strange fellow tells your stewards that his horse won the race. You meet with the strange fellow and you notice he has a falcon on his arm. He advises you that his horse won the race and points to the falcon. You point out that that is not a horse but a falcon. He then assures you that he belongs to a very learned society, and according to that society’s definition, the animal on his arm is a horse.

You in turn point out that his “horse” did not run the race. He says that that is merely a matter of semantics, since everyone knows that his “horse” is faster than any horse on the field. Therefore, without actually running, it won.

What must the chairman do with this strange fellow? The logical answer is to tell the stewards to escort him off the course and not to let him back again. He should talk to like-minded people and not be allowed into the world of real horse racing.

Oddly the above happens every day. This is one of the great impediments to solving today’s problems and can be illustrated in the current Solvency Assessment and Management (SAM) proposals.

Translating the parable into SAM

Assume you run a smallish insurance company with a premium income of R200 million per annum. The company has shareholders and you have a fiduciary duty to report accurately on the financial position of the company. So you employ and train staff, including claims staff. You instruct them that if a claim is reported, they must immediately capture the claim. Failure to do so means that your financials do not accurately reflect the financial position of the company. This is also the most efficient way to run the company.

The phone rings. The claim is the theft of a motor car, a total loss. The claims staff punch in make, model, type of loss, and like magic, the market value of the vehicle appears on the screen. The claims staff enter into the computer R150 000, the estimated value of the loss, and pass the file on for processing to finalisation. More accounting entries follow as more information is received.

Now your clever computer programmers have programmed the computer to process the accounting at the same time. Your computer debits the income statement with a provision of R150 000 and credits liabilities on the balance sheet with the same amount, as prescribed by International Financial Reporting Standards (IFRS) in Insurance Contracts.

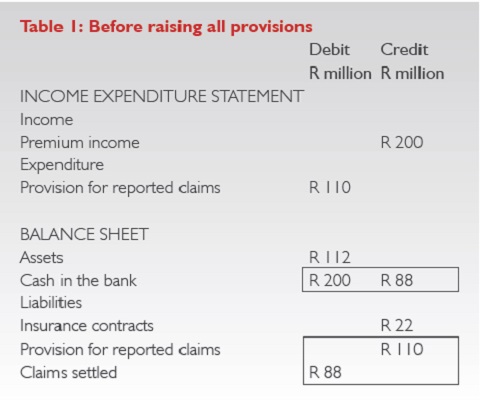

At the end of the year you know exactly the estimated value of all reported claims. Assume this is R110 million. Your claims staff have settled R88 million of the claims, giving an outstanding balance of R22 million. See Table 1.

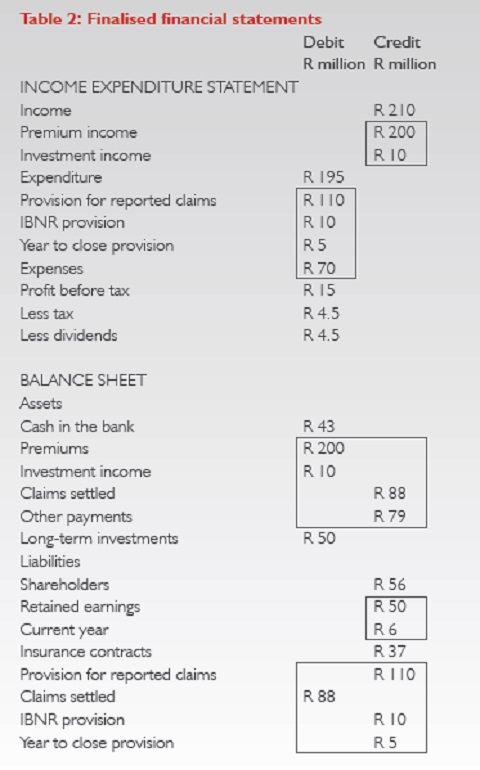

Since you have been operating insurance companies for a long time, you know, at the end of the year, at least, there are a few things you account for. Firstly, you know there are claims in the pipeline that have been incurred but not reported. From experience you know it is less than a month’s value of claims, but to be safe you work on a month’s worth of claims. This is R10 million. So you raise an Incurred But Not Reported (IBNR) provision of R10 million.

You know that your book runs at a claims ratio of 60 percent and thus expect the final claims figures to be R120 million, while reported claims are R110 million. The R10 million is in line with what you think it will be. You also know that you have settled only R88 million out of what you estimate will be R120 million in claims for the year. Additionally, you are not sure if the provision of R120 m is altogether accurate.

Normally you do not worry about this, but since you want to accurately represent the company’s position, you raise a Year To Close provision of R5 million. Once you have paid the expenses,

taxes, dividends, and accounted for investment income, you have cash in the bank sufficient to cover all known claims. Your company had a reserve of R50 million at the beginning of the year. It is more than solvent. The final position after raising the provisions is shown in Table 2.

The falcon is a horse

One day a strange man arrives, introducing himself as the regulator, informing you that you do not know what you are doing. You now have to do things according to SAM.

Firstly, the strange man says you do not know how to calculate the IBNR. It must be calculated using the actuaries Bornhuetter-Ferguson method. You do not want to sound as if you are ignorant, so you offer him a cup of coffee and go Google “Bornhueter-Ferguson method”.

You find and download the 1972 paper and quickly read the introduction. You then come across this amazing statement: “Most [insurance] companies take the narrow view that the IBNR reserve is intended to provide only for [claims that] have not yet been reported.”

You think: “My goodness but that is exactly what I think.” Indeed, this is what insurance companies have understood the IBNR to mean for the past 150 years or so.

However, the paper explains that insurance companies are irrational to believe that the IBNR is the IBNR. The authors of the paper know much better. IBNR, according to them, includes the possible error in the original claims estimates and includes your Year To Close provision. You also have no idea why they call the IBNR a reserve when it is an above-the-line current expense. You have always called this a provision.

The industry’s racehorse is not the same as the regulator’s racehorse. The regulator has a falcon and calls it a a racehorse. Both are using the same word but they describe two different things.

Abuse of words

You do not want to offend your guest. So you join him for coffee and he continues to explain SAM to you. He says that you need have a “technical reserve”. You look at your latest finalised Annual Financial Statements (Table 2), which have stood the industry in such good stead for hundreds of years, but you cannot find anything called a “technical reserve”.

You wonder whether this is the same as IFRS’s Insurance Contracts. Perhaps the regulator is confusing provisions and reserves, or he simply does not know the difference.

If Insurance Contracts is the same as the regulator’s Technical Reserves, then why has it got a different name? If it is different, is this another falcon the regulator is confusing with a racehorse?

This all becomes too much for you and you bid your guest farewell. You find yourself thinking that perhaps John Locke’s book “On the abuse of words” (1686) should become prescribed reading. Locke explained the importance of everyone using the same words to describe the same things. As Locke pointed out, most disputes would be avoided if this was done.