The end of filing annual tax returns

Every year, millions of taxpayers are compelled to file tax returns. This article suggests a way to dispense with this unnecessary practice. In the vast majority of cases, the reason for this practice is no longer clear.

Take, for example, an employee whose only source of income is his salary. His tax details are: income, leave pay, bonus, travel expenses, medical aid, pension contributions, and whatever else the company offers. Everything is worked out by the employer, and the employee receives his IRP5 form.

The employer subtracts the so-called pay-as-you-earn (PAYE) and pays this over to the South African Revenue Service (SARS) simultaneously when the salary payment is made to the employee. PAYE is in reality an employee’s withholding tax and should be renamed as such. At the end of the year, the employer gives a copy of the IRP5 form to the employee who used to pass it on to SARS.

At the same time, SARS is sent a copy and has an elaborate process of reconciling employee-employer transactions. So by the time the employee sends the information to SARS, SARS has long since had all the information. There is no point whatsoever in the employee sending information to SARS which SARS already has. SARS works out the tax liability of the taxpayer from the information sent to it. It can do so without the taxpayer filing a return, giving information already received.

Income tax unacceptably complex

Not only is it unnecessary to send the information to SARS, the average employee does not, and cannot, work out his own tax liability. A taxpayer was recently of the opinion that he was not liable to pay tax on income he earned. He consulted three professional tax consultants, with many years’ experience and all three advised him that he had to pay tax on the income. The taxpayer disagreed and spent considerable time working his way through the Income Tax Act and found that there was, as he suspected, an exemption in the tax Act covering his case. He returned to the consultants who then agreed that he was not liable for tax.

Tax legislation is virtually unknowable, let alone subject to compliance. One of the world’s greatest judges said that when he reads tax legislation, the words simply swam meaninglessly before his eyes.

This is a far cry from the standard laid down centuries ago by Montesquieu in 1748 who said, “Tax ought to be easy to collect, and so clearly settled, as to leave no opportunity for the collectors to increase or diminish these.” Adam Smith, the father of modern economics, agreed when he articulated his famous canons of taxation in 1776.

We need to design an income tax system which, for the vast majority of taxpayers, meets Montesquieu’s standard, and this is what I am suggesting.

Place a sales tax on goods

A sales tax on goods is a good illustration of what Montesquieu had in mind. The taxpayer pays 14% of the purchase price of the goods. As far as the public is concerned, there are no forms to fill in, no reconciliation, no returns, no filings… nothing.

When the goods are purchased, the tax matter is at that point clearly settled. SARS cannot increase or decrease the tax liability of the purchaser of the goods.

Withholding taxes

We need a system whereby every time the taxpayer receives income, a percentage of the income goes to SARS and the balance is paid over to the taxpayer. The so-called PAYE system should be extended to other common forms of income and the system simplified to make that, as far as possible, the end of the matter. The tax matter is clearly settled at that point.

All that is needed to achieve this, is that any other form of income have to be treated the same as salaries. Income is disclosed to SARS and a deduction, at a pre-determined percentage is paid to SARS by the person making the payment.

In fact, some other forms of income have been taxed at the source, in this manner, for decades. The so-called company tax was, until recently, the shareholder’s withholding tax. Until recently, when a company made a profit, which actually belongs to the shareholder, the profit was taxed at the source and that was the end of the matter. To correctly deal with the matter, that profit due to the shareholder, should have been included by the taxpayer as part of his taxable income and from this, subtracted the withholding tax already paid to SARS, the so-called company tax.

The taxpayer should have been liable for the difference, if any, or be entitled to a refund if there was one. Instead, the withholding tax was paid directly by the company to SARS and treated as the final tax. In Montesquieu’s terminology, the tax matter was clearly settled at that point. The company tax, like the sales tax, was in full and final settlement of the shareholders’ tax liability for this source of income. No forms or notification by the taxpayer was required. This clear position has of course been confused with the recent re-introduction of dividend tax, the double taxation eliminated by the Margo Commission. So all that is needed to do away with the annual tax filing, is that tax should be subtracted at the source, at a pre-determined percentage and paid over to SARS. SARS, and the taxpayer, will be advised accordingly. The system of withholding tax should be extended to other common sources of income.

The proposed system

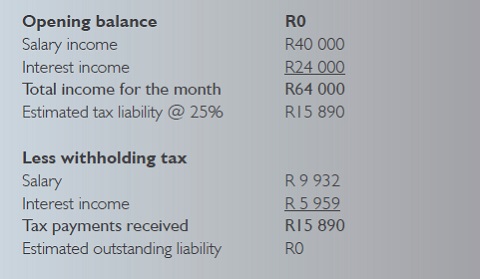

My proposed system can be illustrated by a simple example. Assume a taxpayer, over the age of 65, earns a salary of R480 000 per annum or R40 000 per month and earns interest income of R48 000 a year, paid twice a year, R24 000 each time. For simplicity’s sake he has no other transactions of tax concern. No medical expenses, no retirement funding and no company transport. The details are shown in the table below. Each time the taxpayer receives a payment, tax is subtracted, paid to SARS and the taxpayer is advised. On a monthly basis SARS, as in the case with any other business, sends out a monthly statement to the taxpayer. Assuming there are no outstanding taxes, in other words the opening balance is zero, the January statement will look as follows:

In this system, there is, of course, no longer anything like provisional tax.

At the end of the year, SARS sends a preliminary tax reconciliation statement to the taxpayer in which his tax liability is worked out. The taxpayer can check the preliminary statement after which the final assessment is sent to the taxpayer. It is in this statement that the taxpayer’s rate of taxation is worked out, the 25% used above, which is the figure used for the next 12 months. There is no need at all for the 12 month period to end at the same point of time, presently the end of February. It could be spread across the year. For simplicity sake, it could be the taxpayer’s month of birth. There is no need for the taxpayer to submit any returns. SARS has all the information it needs to do the preliminary reconciliation statement. With some forms of income the taxpayer may have some additional items of expenditure. For example, if the taxpayer owns property he has leased out, he can submit these expense details at the end of the tax cycle. If there is an outstanding balance, because when finally worked out the 25% was slightly out, the taxpayer can pay in the difference or get a refund. Even this is unnecessary. The taxpayer pays tax his entire working life. The tax rate can be increased slightly in the next tax period to recover the slight deficit.

Abolish the current system

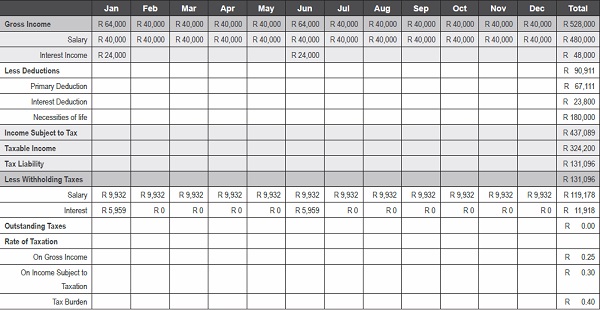

The tax calculation should be simplified to follow the correct theory of taxation which means abolishing the current system of rebates and replacing it with deductions reflecting actual expenditure values. Income subject to taxation equals gross income minus deductions and exemptions.

Once this is determined, tax liability is then determined from the tax rate tables. Once the tax liability is known, the rates of taxation on gross income can be determined. In the table below, the taxpayer’s rate of taxation on the gross income is 0.25% and 0.30% on income subject to taxation. It is the use of this rate, in the above system, which enables income tax to emulate sales tax.

Necessities of life

The tax burden, which is not currently calculated, can also be determined. This requires determining the taxpayer’s taxable income, which is gross income minus necessities of life (or non-discretionary expenditure). It will be seen that, currently, the primary deduction is R67 111. This represents the amount needed to cover the necessities of life.

Some years ago, in a paper published in the South African Journal of Economics, I estimated the figure to be R120 000 for a person living by himself. Today, allowing for inflation, it is likely to be in the order of R180 000 a year. A separate independent body should determine that figure annually. For the taxpayer in the table, the tax burden is 40%, which is vastly different from the 25% used to determine the tax liability. The taxpayer who does not have time, knowledge of interest in tax matters, accepts the preliminary statement as the final assessment. He then gets on with his life. If he so chooses, he can go through life without ever being involved with SARS. For him, as in the case of sales tax on goods, the matter is always clearly and finally settled when the percentage of his income is paid over to SARS.