SAM: Knowing the difference between provisions and reserves

01 June 2012 | Magazine Archives FAnews & FAnuus | Prof Robert Vivian | Robert W Vivian, James Britten, University of the Witwatersrand

Solvency Assessment and Management (SAM) is based on Europe’s Solvency II system, which in turn is based on the Basel capital regulatory system for banks. Local insurance companies as required by the FSB have made steady progress towards implementing the methodology.

Before the 2008 financial collapse Basel II was the prevailing banking risk management system. This system was unable to prevent the global banking crisis, and so Basel III was born. It is not clear that Basel III will succeed where its predecessor failed, nor whether a capital management system designed for banks is applicable, at all, to insurance.

Banks versus insurers

Banks are concerned with capital preservation (savings) while insurance companies are concerned with paying claims out of premiums (revenue not capital). It is therefore difficult to draw a conceptual link between a banking capital regulatory system and an insurance revenue management system. Until the 1900s at least regulators were concerned with insurers premiums not capital.

There is no evidence that the existing system, which is costless to implement, has failed. If one takes two aspects of the current system the costless nature becomes clear. The Incurred but Not Reported (IBNR) provision is set at 7% (and the reserve at 25%) of premiums. Financial statements – produced in the course of business – report premium income – with the result these calculations can be done at no cost.

There is a further problem, the subject of this article. If the literature from American actuaries is consulted it becomes clear that actuaries do not know the difference between provisions and reserves. Actuaries have only once concept in mind: Reserves.

Confusing the definitions

It remains unclear whether they are unaware of something called a provision, or whether they assume the word "reserve” to also mean provision! But the distinction is important.

A provision is an amount which is legitimately charged to the current year’s income statement. It is legitimate because it represents income or expenditure which belongs to the financial year under consideration. This provision ensures that income and expenditure is correctly matched, vitally important when it comes to insurance. A reserve does not represent income or expenditure actually incurred during the accounting year.

The distinction is illustrated by an example. It takes some time after an event occurs before the insurer receives notification. After the event has occurred, the insured usually contacts his broker who will send the insured a claim form. It may take time for the insured to get the information needed to complete the form and return the form to the broker. The broker must then notify the insurer.

The liability event

As a rule an insurer becomes liable to indemnify the insured when a loss event occurs, not when the insurer is notified. Because the insurer knows that there are claims which have not been notified it raises a provision for these claims, known as the IBNR provision.

A reserve is different. Consider the amount held by an insurer in reserve for possible earthquakes or other catastrophes, for example. An insurer may reason that it has had a number of good years, years with an absence of severe claims such as hail, flood, earthquakes and so on.

The insurer decides to build-up reserves from the good years to cover the bad. But because no expenditure is actually incurred, the insurer cannot raise such provision during the good years! A reserve therefore represents "expenditure” not incurred, and thus has no place in the conventional income statement of an insurance company.

No record required

It should be noted that whereas items exist on the insurer’s financial statements for provisions, no such items exist for reserves. Reserves can be calculated from the financial statements and indicated as a note to financial statements, but no accounting entries are made for reserves.

So for example when dealing with the IBNR provision the expenditure account is debited, and liabilities (Insurance Contracts) credited with the amount of the provision. The expenditure account is not debited and no liability folio is credited for an earthquake reserve.

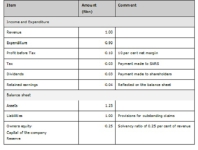

If actuaries are unclear on the difference between provisions and reserves, there is a danger the correct accounting procedures will not be followed when SAM is implemented. This is illustrated by way of an example (in Table 1) which shows the current financial financial position of an insurer. Assume after a SAM assessment has been done that a decision is taken to "strengthen” the reserves.

Clearly the company is solvent. It has an income of R1 billion and makes a profit before tax at a margin of 10%. And it has more than enough assets to cover its liabilities – if it settled all of its claims it would be left with R250 million!

The solvent / insolvent riddle

The SAM calculation is carried out and it is decided to "strengthen” the reserves by R0.4 billion. On the face of it there is no rational reason for this decision since the company is profitable and solvent… And it is nonsense that mere calculations can move a company from being a solvent company to being an insolvent one.

The important question now becomes, what accounting entries are required to deal with the R0.4 billion? The answer to this is none whatsoever. The increase is a reserve and no accounting entries are needed for reserves. But there are questions the board of directors will have to answer. The most important being where the additional R0.4 billion will come from?

The most obvious answer is from shareholders. The company could raise the additional capital from a rights issue. It is difficult to see why shareholders will want to inject more capital into the company since the additional capital will not increase the return to shareholders.

Withholding dividends

A second option is to retain earnings by paying no dividends for a number of years. Shareholders may not like that solution either, but at least the value of their shares increase.

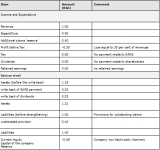

Now what would happen if it is not understood that no accounting entries are required and the actuary decides that to meet the requirement of SAM that the claims reserves (meaning provisions) need to be "strengthened”. Strengthening claims reserves is an oxymoron! In this case an unallocated provision of R0.4 billion will be raised by debiting the income statement and crediting liabilities. The outcome is indicated in Table 2.

Destroying a vibrant company

The position is now completely different from before. Owners’ equity is negative and the company is technically insolvent. Techical insolvency is not sufficient to liquidate the company but it does not have the required capital reserve, with the result the regulator can cause a solvent company to be wound up.

Shareholders will not inject new capital into the company because it reflects a loss of R900 million and is shown to be technically insolvent. The SARS payment should not have been reversed either, since the strengthening reserves provision does not represent expenditure actually incurred in the production of income.

It is near impossible to tell if the increase in the provision is a genuine provision or not. One clue is the unallocated nature of the provision – it is not associated with existing claims! With the arrival of SAM it is important to distinguish between provisions and reserves.

Foot note:

‘This is an extract from a paper entitled Managing the "solvency” (SCR regulatory) risk presented at a workshop held on the 3rd April 2012, arranged by Asyst Intelligence, a company specializing inter alia in SAM’.