Underwriting ‘the Big C’

01 October 2012 | Magazine Archives FAnews & FAnuus | Life | Nicholas van der Nest, Liberty

Cancer is a dread disease that nobody wants to face. It imposes severe financial and emotional hardships on both the sufferer and their family, especially if contingency plans for such eventualities are not in place. Advances in underwriting practices mean that you can offer your clients risk covers based on their specific needs.

Cancer is regarded as a dread disease by both the insurance industry and the medical community. It accounted for some 23.7% of the more than R2 billion in life claims paid by Liberty through 2011, the second highest cause. The group reveals that 14% of all claims paid within the first three years of inception of the policy were cancer-related too.

Early detection is critical

Cancers tend to be asymptomatic prior to diagnosis. What this means is that most cancers have been growing for an average of three to six years by the time they are diagnosed.

An article in the Lancet Medical Journal reports that the global incidence of cancer could increase by up to 200% in developing countries and by 75% in developed countries from 2008 to 2030. This is mainly due to lifestyle changes in the former and aging populations in the latter.

Cancer can be described as the uncontrolled growth of abnormal cells that expand and invade surrounding tissue and which can then spread to other parts of the body. It can occur in any cell in the body. The risk of mortality and morbidity relates to the cancer’s interference with the normal functions of the cells or organs invaded.

Cancer risk factors

Many factors affect an individual’s risk of developing cancer. Some of these factors have been clearly identified by scientists as smoking, excessive exposure to sunlight and an inherited predisposition to cancer.

Mounting evidence shows that a previous cancer is also a risk factor for developing multiple cancers. Cancer patients have a 20% higher risk, on average, of developing a new primary cancer, compared to the general population. This is particularly true for survivors of childhood cancers.

There is a definite need among cancer survivors to access insurance cover. In such cases the underwriter requires detailed information in order to assess the risk of providing the required cover at equitable rates.

Essential underwriting information

Factors that affect the prognosis of the cancer sufferer include the stage at which the cancer was diagnosed, the type of cancer, the age of the patient at diagnosis, co-morbid conditions at the time of diagnosis, response to treatment and recurrence or metastasis of the cancer.

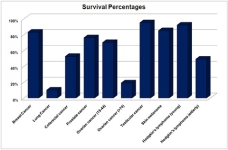

Why is this information important? Table 1 shows the 10 and 20 year survival of cancers by type of cancer. It suggests that oesophageal cancer has a much poorer prognosis than either colon or thyroid cancer. And it shows that survival rates for breast cancer and Hodgkin’s lymphoma are different 10 and 20 years after completion of treatment. Increased mortality risk exhibits many years after remission.

Table 1: Relative survival rates by type of cancer

The stage at which the cancer is diagnosed also affects survival (as indicated in Table 2). Survival rates measured over a five year period from the time of diagnosis confirm higher mortality for more severe cancer stages. A person diagnosed at Stage IV has a 15% five-year survival rate!

Measuring survival rates

Certain types of cancer also show different survival rates depending on the age at diagnosis. Ovarian cancer and Hodgkin’s lymphoma have a higher survival rate when diagnosed in a younger age group (per Tabel 3 above).

Another factor that must be considered is the period after treatment completion, when the risk of recurrence or metastasis remains high. The risk is higher in Stages III and IV than for cancers diagnosed in stage I and II in general – again depending on the type of cancer.

Unavoidable side-effects

Cancer treatments can increase the patient’s risk of developing other cancers too. Radiation therapy to the chest (for breast cancer) increases the risk of lung cancer. And the hormone suppression therapy used to treat certain breast cancers increases the patient’s cardiovascular risk.

Your client may have to provide the underwriter with histology reports, full treatment details and information about follow-ups to complete an accurate risk assessment. Liberty underwriters have developed a thorough understanding of these factors and try in all instances to offer risk cover based on your client’s specific needs.