Genetic testing : the industry benefits

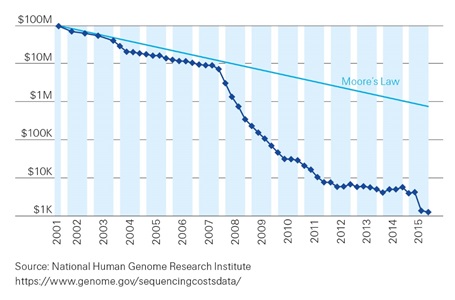

Since the Human Genome Project was completed in 2003, genome-sequencing costs have fallen dramatically and the number of available genetic tests has grown substantially.

From an underwriter's perspective, this unprecedented access to genetic information has the potential to become a crucial piece of information for risk classification. However, there is the possibility for substantial adverse selection, particularly for critical illness products.

Understanding the interplay

As a result, the legal frameworks that support the symmetry of information between insurer and insured through the sharing of an individual's full medical risk profile will become key to a sustainable life insurance industry.

Up to now, our understanding of the human genetic code has been incredibly difficult. However, we are getting better at understanding the interplay between genes and disease.

This means we are also getting a lot better at predicting disease onset and progression. This is the Holy Grail and it has the potential to drive innovation on product design and underwriting.

Direct marketing

While there is still a lot of work to be done before predictive risk assessment becomes reality, genetic testing has already started to become advertised by direct to consumer genetic testing companies as a new health management tool to consumers.

The provision of personalised adverse drug reaction and nutritional advice, backed by genetic profiles, has great potential to improve drug treatment outcomes and provide a strong incentive for lifestyle adjustments.

Direct-to-consumer (DTC) testing

Many private genetic testing companies are attempting to capitalize on the fast evolution in testing technology by bringing testing kits directly to consumers that estimate the risk of developing a disease, gives advice on nutrition, lifestyle changes and medication, or informs about possible medical care and prevention for a customer, given their genotype. So far, insurers are mostly providing DTC test kits to their customers as part of wellness or lifestyle based loyalty programs.

Most DTC tests focus on common and complex diseases like heart disease, cancer or diabetes. Although robust and accurate, most of these genetic variations only account for a small fraction of risk for a specific disease.

In their current state, the predictive value from DTC genetic tests for risk of a disease in the future is often poor and any medical benefit or clinical utility gained through a DTC service is modest at best.

Current challenges

Genetic testing is being used in many fields of medicine with great success such as diagnosis of diseases, pre-natal screening, screening of new-borns, predicting risk for developing a disease and pharmacogenetics.

However, it is important to remember there are some points to remember that a specific genetic variant may:

- confirm that you will likely develop a disease but not necessarily when (if at all) or how severe the disease will be;

- show that you are at increased risk of a disease which in some instances may be only slightly increased compared to an average person; and

- only be one of many factors, e.g. lifestyle or environmental factors, that affect increased risk of developing a disease.

This has attracted lots of regulatory scrutiny around, amongst others, the role of health professionals, interpretation of tests and pre-/post- test counselling.

Regulation

Worldwide, there is great variety of regulation and industry agreements on how underwriters may or may not use genetic information for life and health insurance purposes.

In South Africa, the Association of Savings and Investments South Africa (ASISA), has published standards for its members to the effect that insurers may not require an applicant to undergo genetic testing but can expect an applicant to fully disclose all results and may accordingly adjust premiums and policy terms and conditions, provided there is sufficient justification to do so.