Fifty shades of grey: the truth behind life claims

While insurers have always strived to act in the best interest of policyholders, it is important to bear in mind that Treating Customers Fairly (TCF) will result in the Financial Services Board (FSB) looking at the activities of insurers, as they have a responsibility to act with the best interest of the customer at heart.

There are many aspects within life policies which are clear cut. However, there are other aspects which are open to interpretation and present some grey areas. It is important to note that these may need to be clarified with clients in the spirit of openness and fairness.

The policy wording hurdle

Policy wording threatens to become a major issue in the South African insurance industry, particularly in the life sector. While there are currently no definitive calls for companies to change their policy wording, there has been some talk among insurers that they may be looking at this during 2015.

Critical llness benefit wording has not been tested against actual claims to the same extent as more established risk benefits such as life cover and occupational disability. This is mainly because these benefits have not been available for as long.

In addition, critical illness policy wording is generally more complex given the required link to objective medical assessment criteria and the interpretation of policy wording also evolves as legal practices and principles change over time. All of these imply that policy wording in older style contracts are, in some instances, ambiguous and open to interpretation.

When faced with a situation of ambiguous policy wording, insurers aim to interpret the wording in a way that would benefit the claimant most. As part of this decision making process, it is also critical to evaluate the details of the claim against the intention of the critical illness product.

Where it is clear that the product had intended to cover a particular condition - based on the severity of the condition, the insurability of the condition and the cost or impact of the required lifestyle adjustments that the condition could have - claims would generally be paid, even if they fall outside of the letter of the policy wording.

Navigating medical tests

The interpretation of medical test results is generally more complicated as insurers have a duty towards policyholders to ensure the long-term sustainability of their cover. From a pricing perspective, a product might become unsustainable if any item of experience significantly deviates from the pricing assumptions made initially.

Focusing specifically on claims experience, a product would become unsustainable if the amount paid in claims significantly exceeds the amount of assumed claims payments. This could be due to an increase in the underlying incidence of a particular claim cause, as well as more accurate diagnostic procedures which lead to an artificial increase in the incidence of a particular claims cause. Claims which are submitted but which do not qualify for payment in terms of the product specification adds to the conundrum.

In general, insurers do not have any influence on the first two aspects, although they can use sophisticated modelling techniques to estimate likely future incidence rates in conjunction with medical professionals. Insurers do however have influence over the sustainability of their products by admitting only those claims they had intended to pay as per their pricing assumptions.

Additional concerns

The large number of declined claims due to not meeting the stated medical definitions is of concern as it may indicate that customers simply do not understand the intention of the contracts they are purchasing or what they are covered for.

Critical Illness benefits in South Africa are generally complicated due to the large number of definitions it covers and the complicated medical definitions that accompany each of these definitions. Using declined claims statistics as a measure of customer understanding, may imply that there is a case to be made for simplified wording and a reduction in the number of conditions covered.

At the same time, there is a growing concern that customers may not fully understand the need that critical illness benefits intend to fulfil which are the funding of lifestyle adjustment expenses after diagnosis with a critical illness rather than funding the expenses associated with the diagnosis and treatment of the illness. In the years to come, it is likely that the number of complaints regarding the issue mentioned above will increase and continuous education around the intention of the benefit remains a key priority.

The increase in the number of cancer claims at an early stage remains of concern. When these benefits were first developed, being diagnosed with cancer typically meant significant lifestyle adjustments, a high likelihood of passing away shortly after diagnosis, and significant non-medical costs associated with the diagnosis.

As medicine has improved and the diagnosis of cancers typically occurs at an earlier stage, the relative impact of suffering a cancer - medically, from a lifestyle perspective and financially - has also changed. As an industry there may be a need to determine whether the needs that critical illness products are intended to cover are still relevant today and whether the sums insured available are in fact justified in that context.

Clarifying the picture

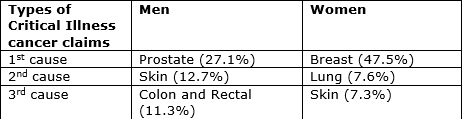

According to Liberty’s stats, cancer has become the biggest reason for claims. According to Liberty’s 2013 claims statistics cancer claims made up 48.2% of all critical illness claims. The majority of these claims (79.7%) were in respect of people older than 45. The main types of cancer also differ significantly between men and women.

The second most prevalent cause of claims is cardiac and cardiovascular conditions (28.1%) and the third is the central nervous system and stroke (11.9%).

The core purpose of life or risk insurance is for clients to provide for their families after they die, become disabled or critically ill. Fully understanding what you are covered for will ensure that there are no nasty surprises when it comes to claims stage.