Don’t go it alone – make sure you have Temporary Income Protection!

01 August 2012 | Magazine Archives FAnews & FAnuus | Life | Brad Toerien, FMI

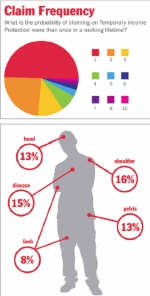

A recent study conducted by FMI revealed that three out of 10 people are likely to face a temporary disability event before the age of 60. The research also confirmed that people invest in permanent rather than in temporary disability cover, with the latter accounting for only 6% of all new disability premiums sold in 2010.

The risk to financial advisers and their self-employed clients lies in the greater chance of suffering frequent temporary interruptions rather than a single long-term disabling event. Financial advisers should, therefore, pay more attention to temporary income protection when addressing their clients’ disability cover needs.

The ‘long wait’ for settlement

Insurers can take months to assess a permanent disability claim. In addition, standard disability benefits do not cover temporary or illness-related claims and tend to carry a three to six month waiting period. Considering the frequency and duration of temporary disabilities, this leaves an obvious gap in the financial planning process.

The long waiting periods prior to permanent disability claims settlement require that financial advisers acknowledge and plan for the risk to income generation posed by frequent temporary interruptions.

Cash flow versus stability

Small business owners are particularly at risk in the case of a temporary disability. Clients who are self-employed or own small businesses are not only concerned with the immediate disruption to cash flow, but with the long-term impact on their business stability. Any temporary interruption – although perhaps not as serious as a permanent disability event – can have serious consequences for an individual’s business, lifestyle, and financial portfolio.

FMI has dozens of examples where temporary disability cover has proved its worth, if not as a life-saver then, at the very least, as a lifestyle saver. Such cover has helped to support a commission-earning salesman suffering from depression, a fitter and turner who could not work due to a broken finger, a car mechanic who needed eight months to recover after falling victim to gun crime, and people from various industries struggling with debilitating back ailments, to name but a few.

Long-term consequences

The consequences of temporary disability can also reach far beyond the disability period, having a permanent impact on business stability. For the small business owner, temporary disability might mean an interruption in cash flow that results in sacrificed expenditure on insurance, investment, and medical aid cover, all of which can contribute to business failure or future insurability problems.

FMI believes that the industry approach to disability is flawed because most FNA tools simply calculate a client’s disability needs with an emphasis on permanent cover. No attempt is made to understand the impact of a temporary interruption in income.

Temporary disability cover continues to be misunderstood and undersold, as evidenced by reports that the average South African income earner is under-insured by 60%.

Cover all the bases

The obvious solution for income earners is to be covered by both temporary and permanent disability insurance. Permanent disability cover can be paid out as a lump sum which can be utilised for once-off events such as settling outstanding debts, for business assurance purposes, to contribute towards an investment, or to prepare for major lifestyle changes.

The risk in this kind of benefit lies in the fact that the client can outlive the pay-out. This makes income replacement benefits an attractive solution Income replacement benefits are designed to cover both permanent and long-duration temporary disabilities and are paid out on a monthly basis to match the client’s income over time. This cover is suitable for maintaining a client’s lifestyle and meeting cash flow requirements. Depending on a client’s disability needs, FMI recommends a holistic approach to disability cover, including essential temporary income protection and a combination of lump sum and income replacement benefits.

Holistic disability cover

To ensure holistic disability cover, financial advisers should take steps to protect their clients against both long-term disability and more frequent short-term disabilities. Ensuring that their clients are protected over both the short term and the longer term is beneficial to financial advisers as well. Clients with immediate income replacement are less likely to lapse other insurance and investment policies.