Differentiation between asset and income protection is important

01 August 2013 | Magazine Archives FAnews & FAnuus | Life | Schalk Malan, BrightRock

An online search for the dictionary definition of income and assets delivers pretty consistent and concise results: Income: (noun) Money received regularly in return for work, capital or land; Asset: (noun) An item that has value and is owned by an individual or entity.

A search for the dictionary definition of life insurance, by contrast, returns varied and long-winded explanations. Many sources focus on the promise of a pay-out to a beneficiary on a person’s death. Some emphasise the tax benefits delivered by life insurance. Others hold forth on the intrinsic value of human life. No wonder consumers aren’t that clear about its purpose either. In a 2012 survey conducted by LIMRA , 70% of Americans failed a basic US life insurance IQ test – and almost a third of respondents didn’t understand the fundamental concept or idea behind it.

What does life insurance boil down to?

But life insurance boils down to two very clear issues: income and assets.

Its purpose is to provide protection against economic loss, of either income or assets, when a person becomes ill, injured or die. For many years, the industry’s focus in packaging cover for consumers has been on the insurable event that leads to the economic loss (highlighting the 3Ds of death, disability and dread disease) without highlighting the nature of the loss itself. Is there any practical value in making a more obvious distinction between income and asset protection needs?

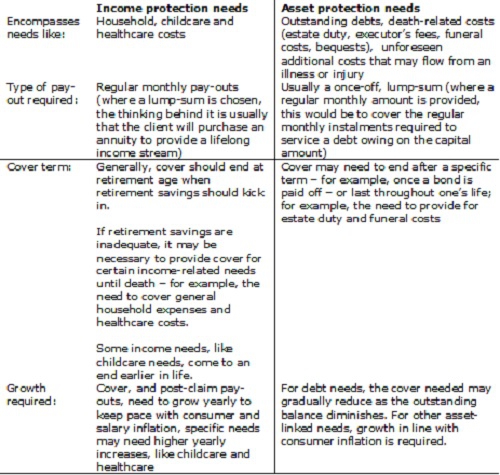

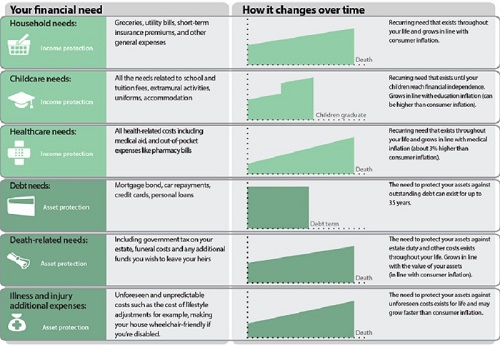

Asset protection vs Income protection

While income and assets share the characteristic of having economic value, the definitions above provide a clue to the fundamental differences between them. Asset protection needs have very different traits, tendencies and trajectory than their income-based counterparts; and that means they should be covered differently.

For you as a financial adviser, clearly differentiating between the two in how you approach your client’s risk protection can significantly enhance the quality of the advice you provide, and result in significant immediate savings for you client .

By structurally differentiating between these two categories of financial need, it is possible for product providers to build in significant differentiation between how the two categories are covered. The distinctions below should be catered for automatically and dynamically over time.

Dangers of no distinction

Conversely, by not making a greater structural distinction between income and asset needs, traditional product offerings may complicate the adviser’s task. They require shoe-horning of the client’s asset and income needs into a single block, for a single period, with growth at a single rate to fit available cover solutions, plus more regular reviews and more complicated calculations. And the inefficiency of these structures costs your clients more.

Some have argued that reducing premium wastage through more efficient structures that are more closely aligned to the differences in income and asset protection needs will reduce the financial adviser’s commission earnings. But in fact, given the massive insurance gap faced by South African consumers, more cost-efficient cover frees up savings that can be put towards buying up more cover, upping the average policy size and thereby increasing rather than reducing the adviser’s commission earnings.