Unlocking the door to the world

When global stock markets run, and you want to expose your client to the best opportunities across the globe, the 25% international exposure limit for Regulation 28 compliant funds can feel frustratingly low.

However, we would like to argue that most retirement funds’ real exposure to international markets is much higher than 25%.

Looking at Africa

Although Regulation 28 of the Pension Funds Act allows international exposure of only 25% of a retirement portfolio, additional geographic diversification is allowed through African exposure of up to 5%.

So by incorporating Africa, in addition to the 25% exposure to international assets, total foreign exposure can reach 30%.

The growth potential for Africa has huge potential. Johan van der Merwe, Sanlam Investments CEO says that he thinks Africa is an awakening giant. He adds that the kind of growth the world has seen up to now is only a taste of a steep growth trajectory still to come.

This sentiment is echoed by several high profile people in other industries. Jannie Durand from Remgro calls Africa a way to diversify out of Remgro’s risk in South Africa. He added that the company is de-risking the Remgro portfolio by going into Africa, opening new revenue streams.

A widening reach

Because of the changing nature of the larger shares listed on the JSE, local equity investors are not as exposed to the South African economy as 20 years ago.

Many South African companies have already globalised, either by dual listing on a foreign stock exchange, by acquiring foreign subsidiaries or by simply extending their distribution footprint outside the borders of South Africa. Think of Naspers, British American Tobacco, BHP Billiton, Woolworths and Steinhoff.

Therefore, the bulk of the earnings and dividends of these companies now originate in foreign countries. According to some analysts, the percentage of the JSE’s earnings that now come from outside of South Africa could be as high as 75%. Yes, Regulation 28 limits the exposure to foreign-listed assets to 25% (30% if you include the rest of Africa), but it cannot limit the foreign earnings of South African-listed companies.

The globalisation trend is likely to persist as local companies continue to search for a higher return on investment offshore than the beleaguered local consumer can offer them. Locally listed companies may still be influenced by the tough economic climate in this country, but their growth - and therefore investors’ return on local equity - is not necessarily stunted.

Careful of anchoring on the past

Just because foreign equity has outperformed South African equity during 2013 and 2014, it does not mean the trend will continue.

Already for the year to 31 August 2015, the local stock exchange has delivered a positive 2.4% in Rand terms, while the MSCI World Index and the MSCI Emerging Market Index have lost 2.1% and 12.6% respectively in US Dollars terms.

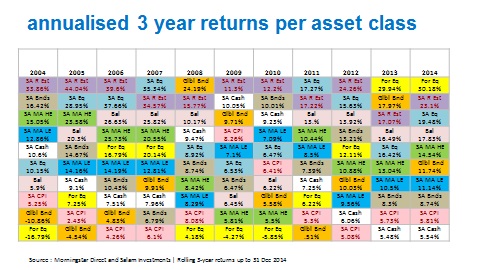

As showed in the accompanying rolling three-year performance table, sometimes real estate comes out top, sometimes South African equity and sometimes foreign equity.

Reason for staying

As much as we sometimes need to persuade investors to take on more offshore exposure to reap the benefits of diversification, we also need to steer them away from placing their entire portfolios offshore, for the same reason.

We also warn against the currency risk of a portfolio that is 100% exposed to foreign assets, but will eventually be used to settle an investor’s bills in rand.

South Africa is a resource-dependent emerging market, and emerging markets can often be volatile, while established markets offer the prospect of steadier growth. A balance of both types of market exposure can give you the growth you need without excessive risk.