The warring factions that govern investing

Let’s face it, quite a few financial planners are giving bad advice because they are scared. They are scared that a drop in the value of their client’s investment will lead to a phone call from the Financial Advisory and Intermediary Services Ombudsman’s (FAIS Ombud) office.

So rather than risk explaining themselves, they place clients in inappropriate low risk investments. It is the same as not taking medicine because we do not like its taste.

Just not getting the point

I recently attended a presentation from a company that has developed a risk profiler for clients that is so good, it comes close to walking on water. However, half way through the presentation I realised that the company presenting might understand exactly how to quantify the risk profile of clients, but just like many financial planners, they do not understand the actual risks involved in investing or how to quantify it. They also believe that the only aspect to consider when doing an investment is the client’s risk profile.

In actual fact, the General Code of Conduct under the FAIS Act states that the financial planner must: “identify the financial product or products that will be appropriate to the client’s risk profile and financial needs,”

Digging deep to unearth this need

If a client, age 40, is investing funds for retirement, his financial needs are to survive off this investment for the rest of his life, a financial need that implies an investment term equal to his life expectancy of 40 years.

When planning for retirement, we cannot rely on mortality tables as these tables ask what the risk is that a person will die early. Longevity tables, which insurers hold much closer to their chest, determine what the risk is that a person will survive to old age, which provides a totally different picture. It is clear that this must be taken into consideration when considering which financial product would be suitable. Not only does this represent the client’s financial needs, but it also represents a risk that needs to be taken into account in the risk profile.

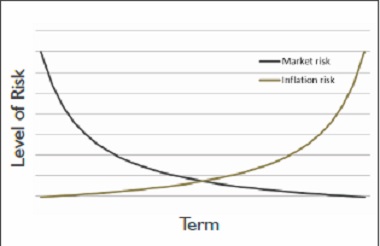

In my opinion, this is the biggest mistake made when considering a client’s risk profile: the risks a client is exposed to changes with time. Inflation risk is negligible over a one year period; but over a 40 year term, 6% inflation reduces the value of money tenfold. Over a 20 year period it loses 69% of its value.

Over a one year period, the worst performance of the JSE since 1960 was -47.60%, over a 20 year the worst was 14.75% and over 40 years the worst performing cycle was 15.98%. The change in risk is illustrated the best with the following graph when only considering inflation and market risk.

The world of a conservative investor

This means that a conservative investor with a 20 year investment term would be in a lower risk investment if he is invested 100% into equities. This is the reason why financial planners add value and is entitled to the remuneration they get. As planners, we need to ascertain what the needs and financial term is of the client. We can then determine the risk profile of the client. And based on all these factors, determine the asset allocation of the financial product.

So next time when asked why a financial planner is needed, remember that it is our job to not only determine the risk profile of the client, but to also determine the risks specific to the investment term and to identify the suitable products for that investment term.