The probability of picking the right fund

Diversification is derived from the Latin word Diversificare meaning “make dissimilar.” If you have diversified something, you have made its parts different from each other. For example, if your investments are diversified, it means you have put money in more than one place - equity, property, bonds and so on.

Picking the correct fund, and/or fund manager for your client for instance, remains one of the most difficult diversification tasks for a financial adviser. In fact, it is the biggest reason why your client either retains your services or fires you. Substantial research has shown that the probability of picking the correct fund is low. S&P Dow Jones presents a regular report called SPIVA, (Standard & Poors Indices Versus Active Funds) that shows how difficult it is to pick the correct fund.

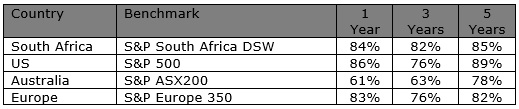

Percentage of active funds outperformed by benchmarks

Source: Standard & Poors 2015

Single funds (especially equities) have been very attractive during the current bull run because of investor preference (sentiment) for equities at a time when other asset classes may seemingly be less attractive. However, what happens when this view is reversed? Will your client fire you?

Another factor about picking funds is persistency – will they still be there after a couple of years? Regulation dictates that funds must be certain sizes for certain periods or else they must close. Poor performance is the main culprit for funds closing since investors chase performance and will quickly flow out of funds they perceive as poor performers.

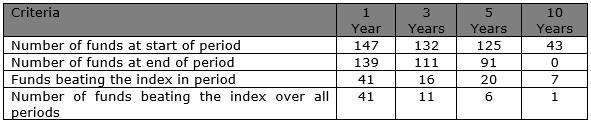

Persistency of performance against the Swix Index

Source: Standard & Poors 2014

The table above suggests that only six funds could boast superior performance over one, three, and five years to the end of December 2014. Only one fund did it over all periods, thus a slim chance of picking the winners.

The asset-allocation strategy

Perhaps the biggest attraction of suggesting an asset allocation strategy to your clients is that if they notice less volatility on their statements, they will be less inclined to react to market sentiment and buy high or sell low.

A big advantage for financial advisers is that they do not have to worry about which asset class is the best or worst at a given time. Nor do they have to worry about the effects of tax and transaction costs that can arise with rebalancing – the asset allocation fund/portfolio mandate or model takes care of all of that.

Fees and costs also play a role. Active asset allocation funds may cost more than index based asset allocation funds because active funds need to constantly make decisions on the stocks within the asset allocation and this costs more. Index asset allocation strategies do not do this but merely use an index that best represents the asset class which costs less.

Costs of being diversified (Active versus Passive)

Source: FE Analytics/Profile Media 2015

As with any investment, costs will affect returns. In the example above, one of the cost categories to consider is the fund Total Expense Ratio (TER) which for the active fund, as a percentage of its return was 39% in contrast to 18% for the passive fund.