Rising education costs demand an “A+” for arithmetic

01 June 2012 | Magazine Archives FAnews & FAnuus | Investments | Nico Coetzee, PPS Investments

Assisting your clients in planning to finance their children’s education often extends beyond a good high school placement or successful matriculation. To make their children’s dreams a reality, your client may have to fund a tertiary education too...

The annual spike in school fees and university tuition costs has significant financial implications for your clients. A clear understanding of their long-term education funding requirements should inform your financial planning advice.

Soaring education costs

A realistic estimate of 2012 tuition fees at a South African university is between R30 000 and R40 000 per year. Factor in living expenses, transport costs and learning material and the "conservative” bill quickly inflates to around R60 000 per year. In fact, the University of Cape Town estimates incidental expenses for a self-sufficient student could top R120 000 per year, excluding tuition!

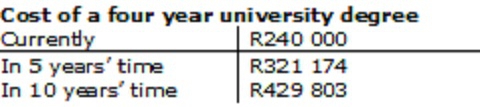

University tuition and related expenses will escalate substantially by the time your clients’ children matriculate. Assuming 6% inflation, the total cost of a four-year degree (at R60 000 per annum today) will swell by almost 80% in 2022.

The magic of compounding

You have to start saving early to accumulate such significant capital amounts. And the sooner your clients begin investing for their children’s tertiary education, the better. Remember – their invested capital appreciates thanks to both the investment return generated from it and the time-honoured concept of compounding.

Your clients can choose between a structured investment vehicle, such as an endowment plan, or a discretionary investment product that offers more flexibility. In both instances, the low minimum investment values and cost savings associated with unit trust-based solutions offer significant advantages when compared to traditional education policies.

A disciplined strategy

An endowment plan supports disciplined investing by allowing your clients to set up a regular debit order, or set aside a lump sum for a fixed investment period. This ensures that they stand to benefit from capital appreciation and compounding over five or more years.

The growth in endowment policies is taxed at 30% while dividends (15%) and capital gains (10%) are taxed within the policy. Any investment proceeds are tax free in your clients’ hands. Investors with a marginal tax exceeding 30% may therefore be presented with a tax advantage.

A discretionary unit trust investment allows you to structure a personalised investment portfolio tailored to your clients’ needs. You can invest directly into a client’s preferred unit trusts and customise the portfolio on an ongoing basis.

Expensive alternative

A third alternative is for your client to finance the costs of a tertiary education by means of a loan. But interest charges will mean that your client pays a great deal more than the amount borrowed.

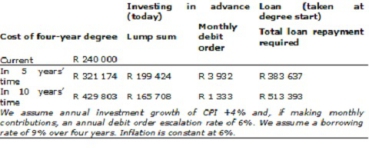

The impact of the three options is illustrated below.

Your client saves money by investing in advance! The following graph illustrates the extent of the saving achieved by planning for a child’s education:

Month-on-month management

If your clients have enough capital available they can potentially save a huge sum on their children’s tertiary tuition by investing an appropriate lump sum as early as possible. By breaking the required capital into a manageable monthly debit order investment, your clients still stand to make significant savings on their education funding obligations.

You should advise your clients to consider their university savings ahead of time, and well ahead of time if possible!