Retail Structured Products

Recent research suggests that, on average, only one out of five actively managed funds that invest in equities managed to beat their benchmarks. This is a clear indication that investors should be considering other ways to attain wealth.

South African investors are also “programmed” that investing is a “long term game”, but we should not forget about medium term investment objectives such as:

• children going to University in five years’ time;

• investors who have attained good growth in the markets over the last few years, but believe that the markets may be overheated and want to protect capital and growth, but still want to be exposed to any further potential market growth; and

• retirees who are forced to be exposed to the market because they need the growth, but do not want to risk their nest egg.

Retail Structured Products (RSP), are listed investment products with a medium term investment goal, that can further diversify your client’s existing wealth accumulation strategy and offer important capital protection mechanisms at the same time. Think of it as investing on the stock market with capital protection.

In their purest form, listed RSPs offer investors key benefits:

• are regulated products on the Johannesburg Stock Exchange;

• typically have fixed terms between three to five years;

• have varying levels of capital protection - some even offer 100%, protecting investors from any downside risk. Investors typically give up dividends in the listed RSP in return for the capital protection;

• deliver a payoff based on a pre-determined mathematical formula;

• use underlying well known and understood indices such as the Top40;

• have the ability to provide returns in most market conditions with limited or no downside risk at very competitive fees;

• do not attract fees over the term of the product. Fees are paid once off and upfront; and

• can be wrapped in a five year term endowment policy offered by a life assurer for financial planning reasons.

How do RSPs work?

Simply put a RSP consists out of three main parts.

• A zero coupon bond: a portion of the investment is used to ensure that the initial capital is returned to the investor at maturity;

• Option (Payoff Strategy): the remaining portion of the investment is used to purchase the option, which is the underlying index that delivers the payoff at maturity.

• Capital Protection: varying levels of capital protection may be selected. More protection means less money goes into the option, less protection means more money goes into the option.

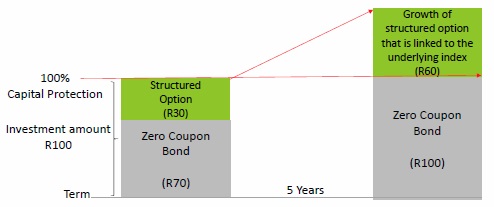

Mechanic of a simple structured products

Assumptions for diagram above (For illustrative purposes only)

• 70% of the initial investment amount after fees and costs is used for the zero coupon bond that will return the investors capital at maturity.

• 30% of the initial investment amount after fees and costs is used to purchase the option on the index (the listed share).

• 100% Capital protection at maturity.

• 100% Return on the structured option at maturity.

Source: Itransact

What are the fees?

Because RSPs are listed on the JSE, it has a share price that is determined by the issuing bank. Other fees such as advice and platform administration fees may also be applicable.

What are the risks?

Because RSPs are provided by banks, the investor takes on the credit risk of the issuing bank. If the RSP is wrapped in an endowment policy, the investor takes on the capital adequacy risk of the chosen life assurer.

When talking investments it is important to establish if your client has other investment time horizons other than long term only. Medium term investment objectives should not be over looked.