Don’t roll the dice when it comes to savings

How do you determine if your fixed deposit or money market fund is actually the right choice for you?

Anyone starting to save regularly or wanting to invest a lump sum over the short term is looking for a high interest rate, easy access to their money, capital preservation and low investment risk.

Be wise, scrutinise

It is worth taking a closer look at the various investment choices to see if you are really getting the best for your savings, which is basically referred to as moving up the yield curve. It refers to looking beyond a fixed deposit or money market fund to other yield-earning investments where you can earn more on your savings.

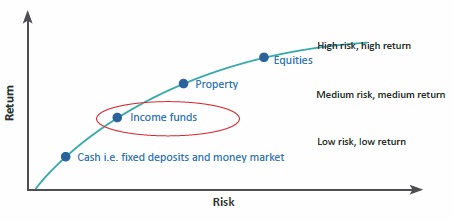

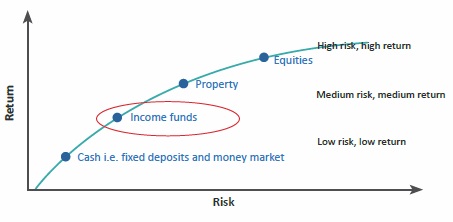

What constitutes the yield curve?

• A fixed deposit is the lowest risk investment, but the returns (interest rates) are also the lowest;

• A money market is still low risk, but offers a better return than a fixed deposit;

• A low-risk income fund has more risk than a money market, but offers better returns;

• A higher-risk income fund offers higher returns but for more risk.

Putting risk into perspective

It may be worth defining risk in terms of how it is used in relation to income funds. The efficient frontier measures different asset classes based on their expected level of risk versus their expected returns.

Income funds, even so-called aggressive income funds, are within the low- to medium-risk category of asset classes. Moving up the yield curve from a bank deposit to an income fund is still classified as lower risk when compared to equity investments.

Time frame matters

Many investors choose a money market fund because they want quick access to their money. However, the actual time frame of investors in money market funds is regularly up to five years and more.

A money market fund is a good option if you are planning to save for between 12 months and two years. If you want access to your money, but plan to invest for up to five years, you may be missing an opportunity by not investing in an income fund where you benefit from higher returns.

A low-risk income fund can give investors 1% to 1.5% more return per year than a money market fund. Over five years, that’s an additional 7.5% on your savings without taking into account compound interest.

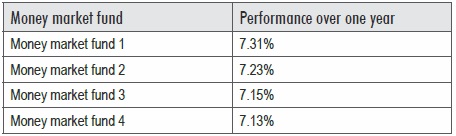

Money market rates

The top-performing money market funds over the past year, provided the following returns:

*Source Morningstar, Money Market category, non-institutional, at 25 June 2016

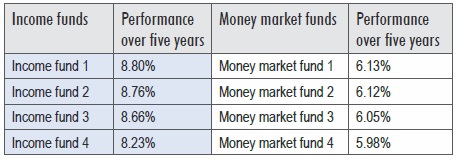

Over a five year period, low-risk income funds provided the following returns vs money market funds:

*Source Morningstar, Bond – Short Term, non-institutional; Money Market, non-institutional, at 25 June 2016

As the world continues to struggle with low investment returns, investors should aim to add extra return where they can while remaining within the low risk band they are comfortable with.