Developed market equities in 2014

When widely-followed global equity indices, like the S&P 500 or the Dow Jones Industrial Index, reach all-time highs, should serious investors really care about the absolute levels of aggregate share markets or individual share prices? Herman van Papendorp, head of Macro Research and Asset Allocation and Co-manager* of balanced funds at Momentum Asset Management, thinks not.

“Fundamentally, company share prices should rise over time in line with the profits and dividends generated by their underlying operations and, as such, the share prices of profit-generating companies should indeed be expected to regularly make new highs. What should be of more interest to the astute investor is whether the level of share prices realistically reflect the underlying earnings-generating fundamentals of the companies.”

S&P 500 not cheap

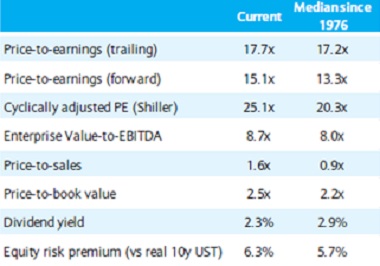

In terms of the US equity market, a wide range of valuation metrics currently point to an S&P 500 that is not cheap, but rather moderately expensive relative to history (see table 1). “This does not, however, mean that a stock market crash is imminent. History shows that a change in underlying fundamentals, like the interest rate cycle, is typically needed for a major stock market correction to ensue and rising US policy rates are more likely from around mid-2015 onwards. Nevertheless, heady valuation levels do indicate likely constrained absolute returns from US equities going forward,” says Van Papendorp.

Table 1: S&P 500 valuation measures

Source: Compustat, Barclays Research. Data as of 10/8/2014

So, what was (and is) an investor to do against the backdrop of an apparently expensive US equity market and a likely tightening US monetary policy cycle next year?

Van Papendorp recommends that, “as always, a balanced asset portfolio that is appropriately diversified across asset classes and regions should limit downside risk, while allowing the investor to participate in potential upside. As a starting point, investors should recognise that US equities are still likely to outperform US fixed-income assets in the coming years, while interest rates rise and with US equities less expensive than US bonds. Asset allocation should therefore be heavily skewed in favour of equities.”

Better value in non-US global equity market

Furthermore, the overall global equity market and other developed equity markets currently show better value than the US equity market and do not have the threat of tighter domestic monetary policy hanging over them. Japanese equities, for instance, are trading at an attractive valuation discount to the world, while relative return on equity (RoE) is improving. Also, the likelihood of additional liquidity support from Japanese policy makers should provide an underpin for equity prices.

Similarly, European equities are also currently trading at attractive valuation levels, while the threat of deflation could spur the European Central Bank to embark on quantitative easing measures that would provide equity market support.

In summary, even though US equity markets are currently trading at historical highs, US equities are still more attractively priced than fixed-income assets, while other developed equity markets, like Japan and Europe, have better valuation metrics than US equities and are likely to receive much more liquidity support in coming years than the US. Investors would therefore likely benefit from, firstly, overweighting equities within a global balanced portfolio and, secondly, giving preference within developed markets to European and Japanese equity exposure.

Asset allocation crucial

Going forward, in addition to US Federal Reserve tapering and rate hike worries, increasing geopolitical tensions around the world are likely to increase the volatilities of asset markets. A recent Merrill Lynch survey found that geopolitical concerns were seen as the largest tail risk by 45% of asset managers.

“There seems to be a disconnect between potential market risks and the low volatility currently experienced by asset classes. Markets are not properly discounting the risk environment, which will have negative implications for returns should these scenarios play out. This needs to be factored into both asset allocation and stock selection decisions,” concludes Van Papendorp.