Bringing passive aggressive into investing

Over the past seven years, pure value asset managers have struggled to outperform market indices, and even asset managers who do not use a strict value investment style have begun struggling to keep up with those indices in the latter part of this period.

Put differently, passive exposure to market capital weighted indices, assuming low cost and tracking error, would have outperformed many active portfolios over this period.

Cash is king

Investment markets in general have been driven by non-fundamental factors to a large extent since the global financial crisis. This is due to vast amounts of liquidity – cash - having been pumped into the global economy by governments wanting to stimulate economic growth. This has not been the only driver of returns in the market, but the impact should not be underestimated.

With more money doing the rounds and chasing the same finite universe of global investible assets, it would make sense for prices to be bid up to higher and higher levels. This notion is supported by the fact that all domestic and global asset classes have provided not only positive returns over the recent number of years, but also those of a large magnitude.

The allocation question

This phenomenon has led to the questioning of the viability of allocating assets to active asset managers in South Africa given the global drive toward passive investment. This drive has been dampened in South Africa due to the performance of a handful of highly successful and prominent asset managers.

The question therefore begs: are we on the verge of entering a new paradigm where active asset management can no longer add value?

Popping the investment bubble

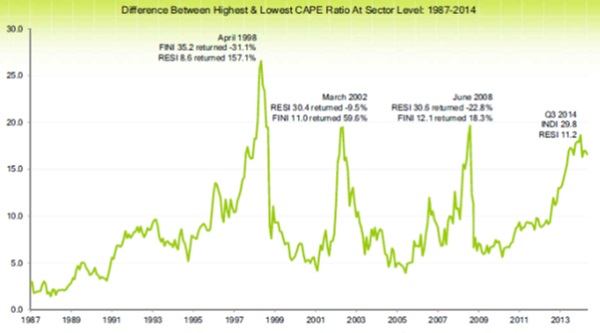

Cannon Asset Managers did an interesting study of previous times that the market has rallied with strong momentum, concentrated to a sector or group of shares that become more and more popular, often referred to as a bubble.

Each time this has occurred, the market has returned back to normal thereafter, rewarding the value investment philosophy. This is called mean reversion, where things return back to “normal”.

The chart shows the last four spikes of the expensiveness of one sector relative to another. It is clear that at the end of the third quarter of 2014, the South African share market was once again in such an extreme position, with resources shares broadly trading at a price earnings ratio of 11.2 times, compared to the 29.8 times of industrials. This emphasises how expensive industrial shares have become, and this phenomenon has not reversed meaningfully yet.

Blood on the streets

Baron Rothschild was credited with saying “The time to buy is when there’s blood in the streets”. Per definition, the market is at its most irrational just before the trend begins to reverse.

One should therefore be careful to kick out the active managers - and probably most notably the value managers - at the time they are best positioned to outperform, given recent underperformance.

Investing for retirement and in retirement implies using the longest time horizon. An investment made at the time of blood in the streets does not usually rocket straight away and requires patience, making this investment philosophy ideally suited to long term investing and specifically for retirement.

Beware the unchecked rush towards passive

Conversely, passive investment, along with the resulting lower cost, also has strong advantages as the cost saving compounds in the long term to be meaningful.

Advisers would need to place more emphasis on an appropriate long term positioning of an investment strategy than timing the market. In the light of the above argument, it may not be advisable to shift exposure from active, particularly value-style, portfolios to passive in the current market context due to the potential unwinding of the irrational scenario at play.