101 on structured products

Structured products have soared in popularity globally over the past decade. Where it used to be the exclusive domain of wealthy investors and institutions, it is now available to everyday retail investors through financial advisers, thanks to some new product innovations.

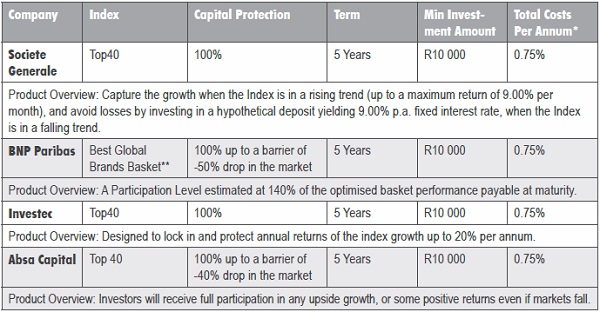

Much like the exchange traded fund (ETF) market it takes a while for a revolutionary idea to go main stream. Here are some key learnings for financial advisers derived from currently available structured products from banks such as Investec, Absa Capital, Societe Generale and BNP Paribas who are all best of breed and highly experienced structured product providers.

Explaining the mechanics

The products supplied by the aforementioned banks are listed the JSE. This fact should provide investors with the necessary regulatory comfort and other advantages such as daily liquidity, transparency and accessibility. In fact, structured products have dual regulation since they are also governed by the FSB, making them one of the most well regulated product types in South Africa. Structured products typically provide a defined return based on a formula which tracks the return of an index, such as the Top 40 index. In addition, structured products contain derivatives that provide potential enhanced returns, (gearing) underpinned by varying levels of capital protection depending on the product type. Investors typically give up the dividend stream of the listed security in return for these benefits.

One cannot be blamed for sitting upright when hearing the word “derivative”, but the truth is that we are all exposed to derivatives on a daily basis. A simple example is your personal bank account where derivatives such as swaps, are employed by the bank on a daily basis to derive the interest rates applicable to your account.

*Based on current available products. Includes platform administration fees, endowment wrapper fee and VAT. Excludes financial advice fees.

** Apple, Google, IBM, Walt Disney and sixteen other well-known global brands. Source: Itransact 2015

Investment term, fees and amounts

Typically the investment term is five years, in some cases the can be less, The 0.75% fee described in the table above is made up of;

• Platform administration fees 0.35% per annum, and can be lower for large amounts.

• Endowment wrapper fees -0.40% per annum

Investment minimums start at as low as R10 000 making structured products highly accessible and cost effective to retail investors. In many cases, platforms will also offer an endowment policy wrapper for special investor needs and estate planning requirements.

Who should own a structured product?

Some uses for structured products include:

• Investors who require exposure to the market, but want their capital protected.

• Investors who have already made good gains on the markets and wish to protect those gains while still continuing to be exposed to the market.

• Investors who are retiring and want to protect their gains.

• Investors who have medium term investment goals such as saving for children’s university education, overseas holiday or paying off their bond.