Why your Medical Aid client cannot do without Gap Cover

01 February 2013 | Magazine Archives FAnews & FAnuus | Healthcare | Michael Settas, Xelus

Out-of-pocket medical expenses not covered by medical schemes are rapidly becoming an unaffordable expense. But, there’s a very effective solution to ensuring that hospital and cancer treatments are properly covered, and your client is not left holding the short end of the stick.

In brief, medical schemes have contracts with medical providers determining the price of services. Payment is direct, does not involve the member and is mainly for services such as hospitalisation, medication, radiology, pathology and sometimes dentistry, optometry, and primary care depending on the design of the medical scheme option.

Mind the Gap

"Where a medical scheme does not have a contract with a provider, it refunds the member according to its set of tariffs. If this is lower than the provider’s fee, then a "gap” is created, which the member covers on an out-of-pocket basis. This is commonly known as a "tariff shortfall’,” explains Michael Settas, managing director of Xelus, a leading gap product provider.

"Consumers are at risk when it comes to surgery or other serious treatment such as oncology, where out-of-pocket costs can be significant. It is now commonplace for us to cover shortfalls of R20-30 000, whereas a few years ago these were exceptions.

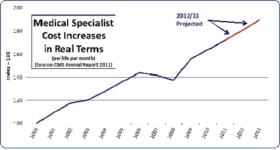

"In real terms, medical specialists’ fees are almost double what they were in 2000. Medical scheme tariffs have simply not been able to keep up, illustrating why tariff shortfalls on high cost treatments are a growing problem. High demand for specialist services, emigration and insufficient graduates are exacerbating factors,” says Settas.

PMB… But!

Although, the Council for Medical Schemes (CMS) acknowledged this problem of high specialists costs (Circular 54/2011), it has been complicated by contradictory claims that comprehensive protection for scheme members is available via the statutory Prescribed Minimum Benefits (PMB). According to a CMS ruling in 2010, PMB must be paid for at actual cost and not at scheme tariff.

This sounds plausible, but is unfortunately an overly simplistic view. The main concerns on the PMB "payment-at-cost” ruling are:

• It applies to contracted specialists, but since specialists are in high demand, they have little incentive to negotiate with medical schemes and are better off charging private rates.

• Relying on PMB for protection removes a consumer’s freedom to consult their specialist of choice.

• Where a scheme does not have contracted specialists, the payment-at-cost ruling automatically applies to PMB procedures. However, according to the CMS’ 2010 Annual Report, only 51% of in-hospital procedures were a PMB. There’s no protection for the remaining 49% of procedures.

Only viable solution

It’s impossible for anyone to determine what ailments are going to afflict them in future, so the PMB present a fragmented solution for members. Gap cover products, however, remain the only viable solution.

"Your client may also face other types of shortfalls arising from the benefit design of schemes, imposing co-payments and deductibles on hospital admissions, or sub-limits on certain in-patient services.”

Viewed against high medical inflation, these are a cost shifting mechanism that increases the out-of-pocket burden for members, so that annual medical scheme contribution increases remain within the CMS’ pre-defined maximum of CPI + 3%.

Simple and reliable

So, what encompasses an effective solution for consumers when choosing a gap cover product? Two main factors should be considered: firstly a "one-product-covers-all-solution”, and secondly, simplicity. There are solutions available and clients needs those options.