The younger healthier generation and medical scheme risk pools

The state of health of citizens in a county is a priority; as it reflects the quality of life enjoyed by its people and impacts on economic development.

South Africa has a strong private healthcare infrastructure, but due to high costs, growth in the private healthcare sector is hampered. This state of affairs points to a major handicap for South Africa where the quality of human capital of the nation determines the economic development and quality of life.

Discussing the numbers game

The 2013/14 Annual Report of the Council for Medical Schemes (CMS) shows that the average age of male medical scheme beneficiaries is generally lower than that of females. The pensioner ratio, beneficiaries aged 65 and older, remains constant at 7.1% for the industry.

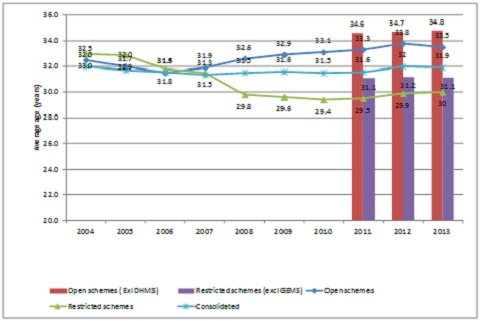

Figure 1 depicts the trend in the average age of beneficiaries from 2004 to 2013. It illustrates that restricted medical scheme members were older than those of open schemes until 2006.

This changed in 2007, primarily due to the introduction of Government Employees Medical Scheme (GEMS). The average age of open scheme beneficiaries in 2013 was 33.5 years and for restricted schemes 30 years.

Figure 1: Age of beneficiaries 2004-2013

Source: Council for Medical Schemes, Annual Report 2013/14

A source of frustration

Although the proportion of pensioners and industry average age remained fairly consistent over the last decade, and is not yet a concern, some individual schemes, especially restricted schemes, have different experiences. Ageing in these schemes and no influx of younger members are partly causing the continuous scheme mergers due to a negative effect on the schemes’ risk pools.

Ageing of beneficiaries has wide implications for any medical scheme. Older age groups generate enhanced demand for primary and tertiary healthcare. This is a concern since the prevalence rate of morbidity is higher within this population segment, which is disproportionately also susceptible to multiple causes of chronic ailments, longer hospitalisation stays, more expensive diagnostic investigations, curative care and rehabilitation procedures.

At the same time, due to good health, many younger people do not see the need to join a medical scheme. Those not studying are low income earners and affordability is an issue. Therefore, students or beneficiaries in the age band of 18 to 25 years should not be treated as adult dependents, but somehow they need to remain in the medical scheme system. They are a relatively low risk and will help improve risk pools and the overall growth of medical schemes.

A big risk worry

Unfortunately, the absence of a risk adjustment mechanism within the funding environment will continuously result in a skewed market structure where some schemes continue to benefit from their risk profiles while others experience worsening demographic profiles, hence the consolidation within the industry will increase.

Income cross-subsidies are needed to ensure that medical scheme memberships are affordable for lower-income households. Currently, wealthier households spend a far lower proportion of their income on medical scheme contributions. Restricted schemes use income cross subsidisation effectively to ensure that low income earners can afford the contributions, but open schemes tend to differentiate contributions by income band only for their low cost options.

Mandatory participation in medical schemes membership for young people in formal employment and increasing income cross subsidisation amongst members will further contribute to accessibility of private healthcare. This would prevent anti-selection and reduce contributions. Mandatory membership would also reduce the average age of the lives covered by medical schemes.

In addition, young people should be encouraged to enter the private healthcare sector as early as they can to improve distribution of risk within medical schemes and to build up sufficient reserves to be viable in the long-term. The absolute number of individuals covered by medical schemes must increase to sustain viability and growth in the private healthcare sector.