Reducing medical aid costs: curative vs preventative health models

Funders and service providers must engage to ensure progression from a curative health model to a preventative health model, within a regulated regime.

According to the July 2013 edition of the Statistics South Africa Fieldworker Summary Report, the average age a person is expected to live in South Africa is 59.6 years. The grim reality of these findings though is the fact that a huge percentage of the country’s population still does not have access to equal healthcare, either in the public or private sector.

Our constitution enshrines the rights and freedom to quality healthcare for all, where government is actively advocating for a National Health Insurance Plan, which is premised on the same ideology. How is this to be found in an increasingly fragmenting public and private health sectors?

Cost is still a major issue

The reality is that only 16% of South Africans have access to private healthcare via medical schemes. There are still many challenges which include the cost of private health services, the de-regulation of costs and the need for negotiated deals between funders and healthcare service providers. These all result in exorbitantly high medical scheme premiums.

Smaller and lower cost medical schemes are at the mercy of this tug of war where they are expected to provide the same healthcare interventions, regardless of how low their contributions per member may be. Whilst all patients are equal, and their care must be equal, there is a big difference in what they contribute. This is exacerbated by the denial of care for seriously ill chronic patients in state for medical scheme members, where treatment was sought for very expensive prescribed minimum benefit (PMB) conditions by low income schemes as a buffer against the interpretation of PMB legislation.

Working in an unsustainable system

The average cost of care per medical scheme patient is indicative of an unsustainable system, as illustrated where the average hospital cost per beneficiary per annum (pbpa) in South African Municipal Workers Union National Medical Aid (SAMWUMED) increased by approximately 180% between 2007, where it was R514 pbpa, and 2013 where it was R1 411 pbpa. This was at a designated service provider hospital network.

The number is much higher at non-designated providers, where no deals exist. Why is patient care increasing so significantly? The answers can be found in the de-regulation of cost and an increased burden of disease often detected very late.

What can be done to stop this run-away train? The answer rests in tariff regulation and of course creating a progressive, preventative healthcare system.

Don’t ignore an effective strategy

Preventative healthcare solutions are often touted, seldom elaborated and more often than never implemented as a complete strategy. If we can control diseases, we can better manage health costs. Medical schemes play a significant role in the health process and must use their strategic advantage to ensure healthier members by facilitating and rewarding prevention strategies.

Medical schemes do employ intervention strategies to better manage the risk pool, such as co-payments and benefit risk strategies via managed care. We must recognise that the solution does not simply rest with benefit cut-backs and certainly not with co-payments, as this is a double blow to the member. It rests with the progressive realisation of better preventative strategies.

For example, by employing benefits for vaccinations, screenings, healthcare assessments, vitamins, contraception or circumcision, it provides a means to better manage quality health outcomes which would ultimately result in lower medical scheme premiums.

Easily diagnosed and treatable chronic conditions such as hypertension and diabetes are very often left undiagnosed, contributing heavily to the health cost burden. The statistics below extracted from the Hospital Quality Assessment Report (HQA) reveal some frightening facts.

Table 1: % Disease prevalence treated in the medical scheme industry

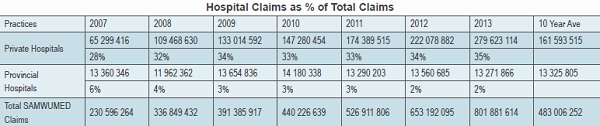

If one considers the care provided for in-hospital costs for these conditions, it would indicate that the rate of prevalence is much higher and remain undetected and thus inappropriately treated, causing considerable downstream costs. The table below is an illustration of the exponentially rising hospital costs at SAMWUMED.

Table 2: SAMWUMED hospital costs as a % of total health spend

No end in sight

What is even more startling, is that we have witnessed an average increase in the cost pbpa of approximately 18% between 2008 and 2013. This is approximately three times the average annual inflation. In the private healthcare sector there are networks. They exist, however, in bilateral vacuums for competitive purposes which far too often limit the potential for economies of scale, which would serve to lower medical scheme premiums. Why can’t SAMWUMED members enjoy the same rates as Government Employees Medical Schemes (GEMS) members, given that there is no competition between these schemes?

According to the 2013 HQA Report, it is the responsibility of the health industry to ensure the right diagnoses, followed by the right treatment in the right setting, at the right time, at the right price, delivering the right outcome, every time.

This is why measuring clinical quality is a corner stone of an effective healthcare system.

The same report further supports the notion that the objective of preventative care and health screening initiatives is to detect illnesses early, prevent future illness, and to minimise the complications and costs that could be associated with such illness, particularly in respect to those who are at higher risk.