What’s the right price point for your practice?

Failing to correctly calculate a price point is one of the biggest mistakes an adviser makes when changing to a fee-based remuneration model.

In the old commission-based world, advisers would simply receive whatever commission was payable by the product provider, irrespective of whether it was sufficient to be profitable. However, in the new fee-based world, instead of selling products, advisers are selling their own expertise, advice and intellectual capital. However, how to cost that accurately can be challenging.

Rule of thumb

The first step in calculating what should be charged, is to work out what it costs to deliver a service. The practice needs to identify how much revenue (before tax) it needs to generate to make a profit, taking into account the cost of sales (advisers), and other business expenses (overheads). The revenue model should be simple. A good rule of thumb is to say that a third of the revenue covers overheads, a third covers advisers and a third covers profit. The business really needs to be making a 20% profit as a minimum.

The next step is to make a decision about the method of charging. Will it be based on an hourly rate, a percentage of assets under management, on a retainer, or a combination of models? The charging model that best suits an adviser firm will depend on the firm’s value proposition. This involves assessing the firm’s area of expertise and the services its clients most value. Propositions can range from holistic, to generalist, or to specialist and the nature of the clients will also be important in the choice of preferred remuneration model(s).

Determining factors

Returning to the calculation of fees, it is important to calculate the total number of hours that will be charged for. If there are eight hours in a day, it might be accurate to say only seven are directly chargeable as the other hour is for administration and marketing tasks. By dividing the gross target revenue figure by the total number of chargeable hours, a benchmark hourly rate can be achieved. This can then be adjusted up or down depending on the service being paid for, and who in the firm is carrying out that service. Even if a staff member has no direct contact with a client, his or her services still need to be costed.

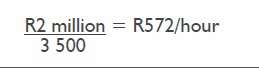

As an example, a practice’s target is to generate approximately R2 million in revenue in the next financial year with three members of staff: a financial planner, a para-planner and an administrator. The firm has worked out that its total chargeable hours are 3 500 a year between the three people.

By dividing the revenue into the total chargeable hours, the firm arrives at a benchmark fee of R572 per hour. This hourly fee can then be scaled upwards or downwards depending on which member of staff is doing the work:

Accurate adjustments

At this point the firm will be able to judge whether the hourly fee for each staff member looks reasonable or not, providing that some research into what competitors are charging has been done. If the rates appear too high, it is advisable to adjust either the revenue target, profit target or the available chargeable hours. Alternatively, improvements can be made to the value proposition to enable and justify charging more.

If the adviser firm does not have the skill and/or the time to accurately work out its revenue and target profits in order to accurately cost the business, a good idea is to engage the services of a practice manager or business transition consultant.