Service Level Agreements key to client satisfaction

01 August 2013 | Magazine Archives FAnews & FAnuus | Features / Profiles | Hennie Reynders, Iemas Financial Services

In the intensely competitive short-term insurance environment, excellent service is the key differentiator. Bad service by service providers impact intermediaries who deal with the client. What can brokers and advisors do?

Brokers that fill the role of a non-mandated intermediary play an important role in looking after the needs of the client. The guidelines set out for Treating Customers Fairly (TCF), aimed to be implemented during 2014, focus on ensuring that clients receive proper information and advice, are treated fairly and that companies deliver on promises made.

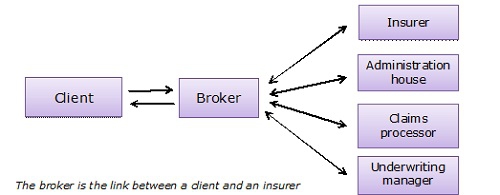

The broker is the link between a client and an insurer - the client will turn to the broker when they need to make a claim, make amendments to a policy or if things go wrong. Intermediaries therefore have to ensure that the role players on who they depend, deliver the service expected by clients.

Manage your Service Level Agreements

For every business process, a broker will need a Service Level Agreement (SLA) with the relevant role player to set out agreed upon services, response times, priorities, responsibilities and guarantees.

The question is whether this will be enough from a TCF perspective? When one looks at how the TCF is drafted, it is in fact a culture that needs to be established across a business. Will a SLA put the broker in a comfortable position and will it be accepted by the regulator if there is a complaint and the broker argues that the SLA was not met by the third parties?

I believe the regulator will place the responsibility on the broker to properly manage these SLA’s and still hold the broker accountable.

Influence on complaints

It is one thing to manage and respond to a client complaint internally, but to depend on a third party’s response is another thing. It becomes more difficult to ensure the complaint is resolved within a suitable timeframe, as the broker is not in charge of the process the third party has to go through. The broker will have to continuously keep track of the feedback process, and keep the client informed.

Smaller brokers will have to face even more challenges, especially in instances where the broker does not have a binder agreement with the insurer, and the administration does not reside with the broker. When the administration is done by the insurer it is another SLA to be managed.

Consumer education will reduce complaints

Earlier this year the Insurance Ombud gave the following advice to insurers and intermediaries in its annual feedback: Consumer education.

Brokers and insurers have to make sure that consumers understand what they are buying, what is covered and what is excluded as this will assist to decrease the number of complaints. However, keep in mind that many of the claims that do not go in the client’s favor are speculative claims. The claimant has nothing to lose coming to the broker’s office and will try to get a declined claim overturned. The broker will depend on the insurer greatly when it comes to claims management.

It all comes back to Service Level Agreements

Whether big or small, the broker has to make sure that the service levels that are offered by insurers and underwriting managers are of a high quality. Clients will turn to you, the broker when they are unhappy with service delivered, not to the third party.

Smaller brokers do not always have the same influence as bigger brokers, and it could happen that insurers use these smaller brokers simply on a ‘Call operator’ methodology, resulting in the level of service delivered not being up to standard.