Customer centricity is changing the face of insurance

02 April 2012 | Magazine Archives FAnews & FAnuus | Features / Profiles | Michael Blain, Centriq Insurance

Corporate institutions, small businesses and individuals derive a sense of financial security from insurance. It is a tool to predict, plan and adapt to an ever-changing world filled with dynamic needs and risks. How can the industry balance growth against the global transformation trends currently exhibiting?

The insurance industry is experiencing increasing levels of transformation on both an internal and external level, locally and globally. While this transformation creates massive opportunities for growth, it also creates challenges.

Raising the bar

One of the biggest tests the industry faces is to keep abreast of rapid and often extreme change. To do so, insurance stakeholders are stepping up their games, raising the bar ever higher. This is particularly true in the manner in which we exercise risk management and control and how we treat our clients.

Recent surveys by PwC: Top Insurance Industry Issues for 2012 and KPMG: The South African Insurance Industry Survey 2011, demonstrate the risks, challenges and transformation issues facing the industry.

A balancing act

The trick is to balance the pursuit of growth against the requirement to protect capital and profits, while meeting clients’ individual needs. Insurers can achieve this by:

• Finding and exploring innovative ways in which to increase market penetration and market share within our borders, or into foreign markets.

• Containing costs through operational efficiency by the aggressive management of expense ratios and underwriting performance, innovatively structured business models and overall product and service offerings.

A shrinking market

Cost saving measures will result in fallout, market consolidation (through acquisitions and mergers) and the complete transformation of certain business models… Other factors, such as regulatory changes, innovative technology-based solutions, the war on skills and talent, and drive to achieve and maintain profitability without sacrificing customer loyalty will impact the industry too.

Key industry stakeholders are shifting from passively identifying and pricing risk (and reactively paying claims once an event has occurred) to proactively avoiding and reducing losses. The competitive "edge” is in better structuring and managing of risks before a claims event occurs!

Extreme makeover SA

This shift demands an extreme makeover of our historically inward-looking and conservative industry. In some instances we need an overall mind shift, in others a change in business model.

Examples include:

• The phasing out and re-examination of manually intensive operating models by using real-time data from sensors and devices to assess the risk of customers based on actual behaviours. This enables policyholder specific pricing, customised, flexible product and other value-added service offerings.

• Improved efficiency and effectiveness of overall marketing campaigns as detailed customer information enables insurers to precisely target customer groups at the lowest possible cost, further enabling them to exercise accurate underwriting and risk management.

• Making use of telematics to price usage-based insurance and proactively control losses and manage risk, which in turn enhances operational profitability and enables the consumption, storage and analysis of vast amounts of data. Insurers can leverage unstructured data to detect fraud and improve claims performance.

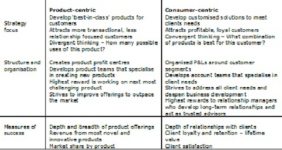

• Shifting from a strong product-focused to a customer-centric operating model, as illustrated in the following table, released by PwC:

We are moving away from product-focused models – in which the core performance driver is to increase market share by means of product or lines of business – to a customer-centric model, where client retention and lifetime value, client satisfaction and insurer/client relationship depth are key.

A key driver of the industry is our recognition of customer power and our realisation that we have to cater for each customer’s needs rather than presenting them with generic options. Over the next paragraphs we’ll expand on this idea under various product categories.

Life, annuities and retirement

Diversified financial services firms are trying to address the full range of customers’ concerns about health, wealth and life uncertainties rather than financial stability only.

Personal lines

We have seen a tremendous increase in the number of self-directed customers… The so-called GenXers (born between 1965 and 1980) and most of the Millennials (born after 1980) like to conduct their own research and make their own insurance decisions, while requiring limited customer service support.

As a result we have experienced an increase in the demand (amongst personal lines customers and agents) for transparency and control over pricing, service and claims. Mobile and interactive technologies for multimedia and multi-channel content dissemination, dialogue, and transactional capabilities via multiple digital platforms are also in demand to drive and meet customers’ immediate needs.

Managing product and risk

Overall, we are seeing a greater commitment from insurers to reconfigure their product offerings and better manage their risk appetite. This focus enables them to cater to clients’ total account needs.

The shift to total solutions entails the redesign of core product platforms, pricing and loss assessment approaches, all of which need to operate at an account rather than line-of-business level. We could also see insurers losing key parts of their book as customers look to simplify their growing operational complexities.