Longevity and the risks that it poses from a retirement planning perspective

01 April 2013 | Magazine Archives FAnews & FAnuus | Employee Benefits | Nico-Louis Minnie, Liberty

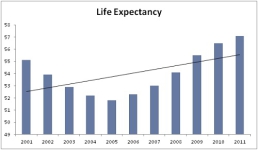

It is no secret that life expectancy has increased over past decades. This is even more relevant in emerging markets due to increased access to medical care and better standards of living. The chart below shows the combined (male and female) life expectancy in South Africa since 2001.

Longevity in South Africa

Source: Statistics South Africa

The initial decline was due to the high prevalence of HIV and relatively poor access to ARVs in the early 2000s. Although the chart is based on average life expectancy the shape for insured lives (since 2005) is similar, with even higher life expectancies. This then creates a couple of issues when it comes to retirement planning, since any unknown or volatile parameter has to be treated with caution.

The cost of longevity

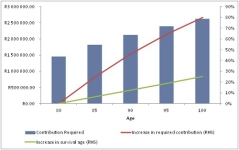

Intuitively, we expect a person living longer to require more resources, but what does that mean quantitatively? We have modelled some retirement scenarios to compare them. The assumptions are quite simple: we assume that the retiree is aged 65 and that he will live to exactly 80, 85, 90, 95 or 100 with a monthly income requirement of R10 000 in real terms, based on a real return of 3% a year. Because we are assuming fixed survival ages we don’t have to consider gender explicitly. The output of this analysis is depicted in the chart below.

Source: Liberty Investments

In this example, 80 is the reference point for someone who retires at 65. The graph shows that if that individual survives to 90 he will have to increase his contribution by 46% in order to be able to still earn a monthly real income of R10 000, up to and including age 90.

A 46% increase in the contribution for a 12.5% increase in age (80 to 90) proves that the increase in the contribution outstrips the increase in age. In other words, if the retiree lives x% longer than expected, he will have to increase his contribution by a percentage far greater than the x%.

What options exist that address this issue?

The easiest way to solve this is to transfer this risk to an insurer that will manage it on its balance sheet. Purchasing an inflation-linked life annuity will ensure that the retiree receives an income that keeps up with inflation for his lifetime. The drawback is that investment freedom is lost and the cost of these annuities is often out of reach of most customers.

Ideally, you want the retiree to be able to have some investment freedom with the option to transfer some or all of the longevity risk to an insurer. One way of achieving this is to combine a living and a life annuity, although this comes with its own challenges around minimum contribution limits. A new development on this front has been to dynamically switch the customer into a life annuity when the income drawdown required on a living annuity becomes unsustainable (above 17.5%).

Another, more flexible, way is to enhance the customer’s investment value as he ages. A recent development in the SA market saw a company adding this feature to a standard living annuity. Customers are rewarded annually if they survive – the product makes use of the pooling of longevity risk and instead of retaining this risk on its balance sheet the insurer uses it to enhance the investment values of participating policyholders. The customer retains full investment freedom on the entire investment value while still being protected against living longer than expected.

The way forward

We have seen some innovations around retirement income provision in the last year and these are expected to gain momentum in the years to come. It is therefore critical to stay abreast of new offerings in the market as well as changes in legislation in order to provide customers with the best possible retirement income vehicle based on their unique needs.