South Africans are not saving enough – what now?

We often hear that South Africans are not saving enough, and that only 6% of South Africans will be able to maintain their standard of living after retirement. But how do you practically become a better saver?

How much are South Africans saving?

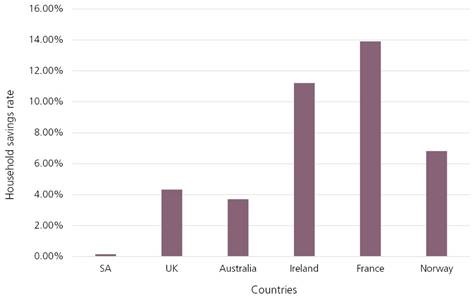

Research by Trading Economics shows that, among the G20 countries, South Africa ranks the lowest in household savings rate. At the beginning of 2019, the ratio of household savings to disposable income was at 0.15%. Among working urban households in South Arica, 40% of people have no formal retirement savings.

GRAPH: Household savings as a percentage of disposable income over previous two years

What is the savings benchmark (or rule of thumb) of saving?

The amount you should be saving will always depend on your goals, the time you have at your disposal and of course your ability to save. But while each person’s saving decision is unique, a simple rule of thumb provides a handy starting point to at least get you thinking along the right lines.

The rule of thumb is to allocate at least 15% of your pre-tax income to retirement savings. After you have done this, you can then consider the following spending guidelines for your after-tax income:

• 60% for necessities (housing, food, utilities)

• 30% discretionary (entertainment and luxuries)

• 10% into discretionary savings (e.g. for education, emergency fund, holidays)

The right answer will be different for everyone, and a financial adviser can help to find the right savings plan for you.

Practical tips to help you save more

It can be challenging to make the necessary lifestyle adjustments if you are currently saving below the recommended levels. The first step is setting up and sticking to your budget; delaying saving until you have ‘enough’ money is sure to end in failure. You are far more likely to succeed if you prioritise investment, and commit your money to your long-term goals before you are tempted to spend it elsewhere.

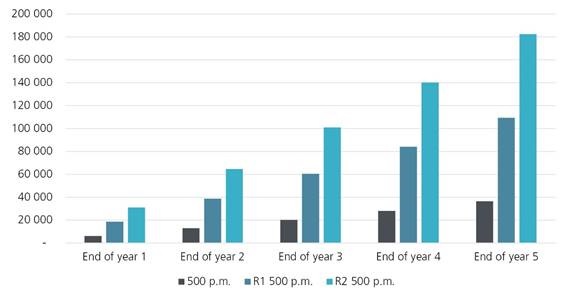

Start by making incremental changes to your lifestyle and continue increasing your commitment until you attain your ideal savings level. Over time, these small adjustments are unlikely to be noticed, but the ‘sacrifices’ you are making gradually and consistently add up, helping you grow your nest egg. Saving soon becomes a part of your personal discipline and will no longer seem like a sacrifice at all! The graph below shows how quickly your savings could add up for different amounts.

Graph: Accumulated savings at the end of each year

The key is to make a start as soon as possible, and to continue to build on that once you have a firm foundation in place. Here are few more guidelines to get you started:

• Start saving small and gradually increase what you save each year.

• Always adjust the amounts you save annually in line with inflation increases.

• Keep a record of all the money you spend and compare it to your budget each month. This will help to point out where you need to make some adjustments to your spending.

• Don’t try and keep up with the Joneses. For example, keep that old cell phone for a few more years, drive your car for a few more years, and you don’t always need the fanciest branded clothing.

• Always preserve your retirement savings when you change jobs.