Smart ways to get more out of your savings

Tracy Jensen, Investment Analyst at Nedgroup

2020 has been a tough year. Economies across the globe have been hit hard and, in an attempt to stimulate growth, interest rates have been cut to the lowest levels in history. Unfortunately however, the subsequent reduction in yields has left many people stranded with a big cut in income at the same time as investments have taken a knock.

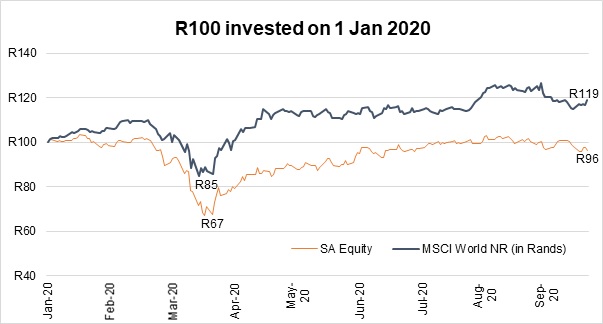

To set the scene, many people lost a significant amount of money on their investments with local and international markets falling by more than 30% in the first quarter. However, those who stayed the course were rewarded as markets bounced back remarkably quickly recovering these loses, as depicted in the chart. This is very unusual and was driven by the COVID-19 pandemic.

In such uncertain times, where volatility and uncertainty seem to be the only constants, it’s important to get the most out of the savings and investments that you do have. Although there is no silver bullet, there are some tips and tricks to make sure that you are optimising your savings during this time.

Tracy Jensen, Investment Analyst at Nedgroup Investments has the following helpful advice:

Tip 1: Optimise your tax

The government wants South Africans to save more to reduce the burden on the state. To encourage this, they are supporting some great tax incentives. Here are a few tax incentives you should take advantage of.

a.) Savings made to a retirement fund reduce your taxable income (up to 27.5% of taxable income subject to a R350 000 annual cap). This means that effectively, SARS is funding your retirement contributions. The money grows tax free and you only pay tax on this in retirement when you draw an income.

b.) Money invested in a tax-free savings account will grow tax-free i.e. you won’t pay dividends tax, interest tax or capital gains tax. You can contribute up to R36 000 a year to a tax-free savings account with a lifetime contribution maximum of R500 000. This is a no-brainer for any investor.

c.) The final incentive is on interest earned. If you are younger than 65 years, the first R23 800 in interest earned is tax free and this is increased to R34 500 for those 65 years and older. At current yields, this allows you to invest about R500,000 (under age 65) and R750,000 (65 years and older) without paying any tax on the interest.

Many people, especially the elderly who receive special dispensation, are not aware of the generous tax exemptions available to investors when it comes to earning interest. Some people invest their money in tax efficient vehicles at lower yields, before they have utilised their allowances, which is a mistake. As we do not receive much from SARS it is worth making use of the few concessions that are available. With falling yields, it’s now even more important that any surplus cash is invested as optimally as possible.

For example, assume a couple over age 75 only earn an income from the interest on their investments. At current interest rates, they would be able to invest approximately R8m in interest earning investments and pay no tax on the interest earned. This tax benefit is a combination of the interest exemption noted above and the annual income tax threshold.

Tip 2: Maximize your returns by matching your time horizon

Short term investments (under 3 years)

In order to get the most out of your savings and investments, you should invest in something that matches the time horizon of when you need the money. For example, if you only need the money in a few years, investing it in a short term (3,6, 9 or 12 months) fixed deposit would mean that you lose out on interest and don’t get the most out of your investment. Currently the call rate is around 3.2%, a 12-month fixed deposit would give you about 3.7% in interest a year, but a 3-year fixed deposit would give you about 4.5% in interest per year.

However, there is an even smarter way to earn a higher interest rate without being locked in for a long period. This is via something called a money market fund or enhanced money market type fund, where the money is accessible within a day. These popular income bearing funds offer yields similar to fixed deposits, but without having to “lock up” the funds for the term of a fixed deposit. To give you an example, the Nedgroup Money Market Fund currently yields about 4.3% and the Nedgroup Core Income Fund (an enhanced money market type fund) yields about 4.6%. The yield on the latter is similar to what you would earn if you locked your money into a 3-year fixed deposit.

Longer term investments (3 years or longer)

On the other hand, if you only need to access the money after a number of years (3 years or more), then a more suitable investment is a fund that has exposure to some growth investments like shares. The longer your time horizon the greater the percentage you should have in growth investments. This generally provides the best long-term returns and you have the time to ride out some of the ups and downs of the market.

Tip 3: Consider the fees you are paying

The higher the fees you pay, the greater the drag on your investments and the more difficult it is to earn higher returns over the long-term. It’s important to find out the fees you are paying, determine whether they are reasonable, and if not, consider similar investments with more reasonable fees. A rough guideline is to try keep your fees under 1% of your investment value a year.

One way of reducing your fees, is to consider investing your money in an equivalent “rules-based” (passive) fund. The Nedgroup Investments Core Funds are an example of this with fees of only 0.35% ex VAT per annum.

Although there is no magic trick to getting more bang for your buck, by implementing all the tips above you can stretch your money and earn better growth on your investments.