Small and steady wins to the savings game

2020 marked a year where many South Africans suffered financial difficulties, affecting both their lifestyle and spending habits, with approximately 60% of South Africans dipping into their savings during the hard lockdown period to cover financial shortfalls.

Not only does this highlight the importance of saving for a rainy day, but also points to the fact that - despite statistics indicating that the nation is one of the worst savers in the world – South Africans are saving, even if at low levels.

Within the PPS membership base on our platform, 16% withdrew from their discretionary savings during this period, drawing down on average more than 20% of the investment’s value.

Notably, the majority of PPS members’ monthly savings commitments remained in place and they continued to strive towards their savings goals with only 16% having paused their monthly contributions since March 2020, and 6% opting to reduce annual debit order escalations rather than stopping altogether.

Historically, the South African household savings ratio (the income saved by households during a certain period of time), has largely remained in negative territory since the Global Financial Crisis. The low savings culture is further exacerbated by the tendency of consumers to spend more than they earn – known as ‘dissaving’. Over the past five years, spending levels of South Africans have increased gradually, at the expense of savings.

So, where have South Africans been spending? According to Stats SA, the biggest expenses are housing and utilities, followed by transport. Interestingly, households spend more on recreation and culture than on education.

However, spending trends tapered off during the 2020 hard lockdown period, with research from Visual Capitalist showing that SA consumers cut back on spending in most categories, except for groceries and home entertainment.

How to start saving

As the path to economic recovery remains unclear, we encourage you to start saving in practical ways without affecting your disposable income.

1. Set goals

Whether saving for a vacation, a house or for retirement, set attainable goals and milestones along the way. Celebrate achievements along the way, which can motivate you to remain committed and continue to pursue your investment goals.

2. Start today

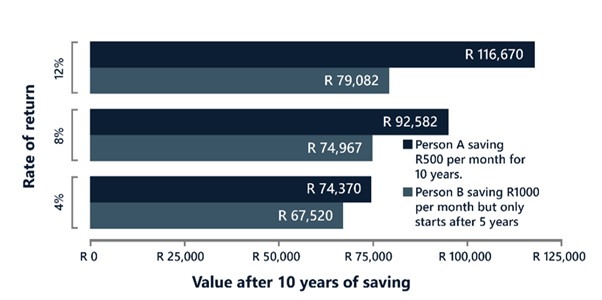

The below illustrates the benefit of starting to save earlier. Compound interest, and the ability of assets to generate earnings, which are reinvested to generate their own earnings, is a key factor in saving earlier.

Source: PPS Investments

In practical terms, a 25-year-old investing R500 per month accumulates more assets within 10 years than a 30-year-old investing R1 000 per month. Illustrating the benefit of compounding, investing a smaller amount over a longer time horizon can have a greater impact on investment results than investing a larger amount for a shorter period of time.

3. Save more

Figuring out where you are spending your money is the first step to identifying which expenses make the most significant impact. Examining and creating a budget is a simple way to see where you could cut back on a few unnecessary expenses to free up some cash to boost your investment contribution. A practical application is the savings you can make on, for example, a takeaway morning cup of coffee. With prices ranging from R20 to R30 for a cup (thanks Starbucks!), investing an additional R500 is the equivalent of around 20 standard takeaway cups of coffee in a month.

4. Start small

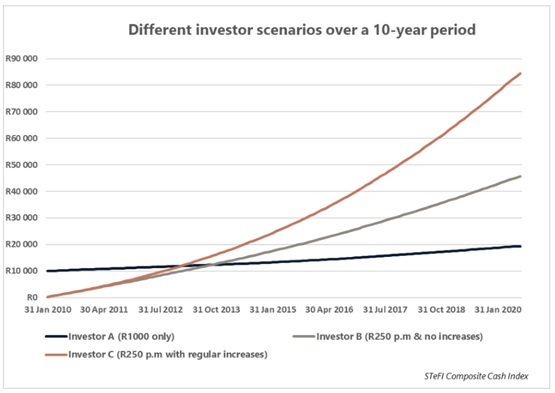

Setting up a debit order allows you to start small and make regular contributions. You will avoid the temptation to access money allocated to savings and will be building up your savings over time. Making regular incremental increases to your monthly contributions can have a positive effect on your investment over time versus investing R1 000 as a once-off investment with no further top ups. Similar, if you were to invest R250 with no increases over 10 years, you would have had about R39 000 less than if you had increased it regularly over time.

Source: PPS Investments

Diversification is key

Another important aspect is a diversified portfolio that provides an opportunity to create a smoother return profile over the long run, as it is better able to withstand fluctuating market conditions. A blend of asset managers is best suited to take advantage of opportunities, both locally and abroad, at different times in the cycle, offering optimal diversification to augment your portfolio that can be achieved through our multi-managed solutions which are positioned to take advantage of any potential changes.

Partner with a trusted financial adviser

Despite the headwinds during 2020, only 2.1% of PPS members reduced their risk profile, which indicates that members remained focused on their financial plan and stayed invested rather than responding to market events and short-term volatility - an approach that could help to ensure achieving financial goals over time. A solid financial plan with a long-term view crafted by a financial adviser allows you to make informed decisions on your holistic portfolio.